Stock Analysis

- United States

- /

- Media

- /

- NYSE:EVC

There's No Escaping Entravision Communications Corporation's (NYSE:EVC) Muted Revenues Despite A 50% Share Price Rise

Entravision Communications Corporation (NYSE:EVC) shareholders are no doubt pleased to see that the share price has bounced 50% in the last month, although it is still struggling to make up recently lost ground. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 67% share price drop in the last twelve months.

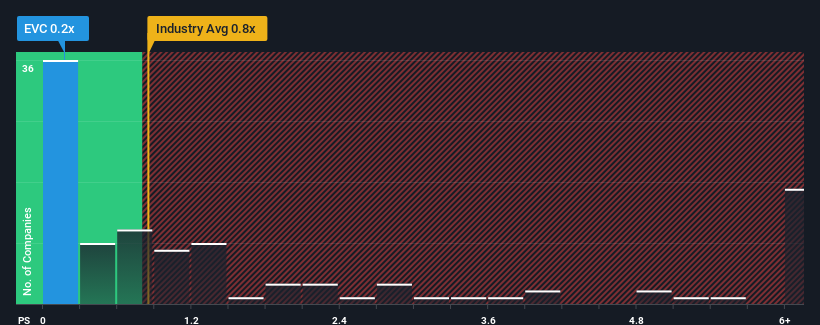

Although its price has surged higher, Entravision Communications may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 0.2x, considering almost half of all companies in the Media industry in the United States have P/S ratios greater than 0.8x and even P/S higher than 3x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for Entravision Communications

How Has Entravision Communications Performed Recently?

Recent times have been advantageous for Entravision Communications as its revenues have been rising faster than most other companies. One possibility is that the P/S ratio is low because investors think this strong revenue performance might be less impressive moving forward. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on Entravision Communications will help you uncover what's on the horizon.How Is Entravision Communications' Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Entravision Communications' to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 16%. The strong recent performance means it was also able to grow revenue by 222% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 18% as estimated by the only analyst watching the company. With the industry predicted to deliver 4.0% growth, that's a disappointing outcome.

In light of this, it's understandable that Entravision Communications' P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Final Word

Entravision Communications' stock price has surged recently, but its but its P/S still remains modest. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

It's clear to see that Entravision Communications maintains its low P/S on the weakness of its forecast for sliding revenue, as expected. As other companies in the industry are forecasting revenue growth, Entravision Communications' poor outlook justifies its low P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Having said that, be aware Entravision Communications is showing 4 warning signs in our investment analysis, and 1 of those is significant.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're helping make it simple.

Find out whether Entravision Communications is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About NYSE:EVC

Entravision Communications

Entravision Communications Corporation operates as an advertising solutions, media, and technology company worldwide.

Good value with adequate balance sheet and pays a dividend.