Stock Analysis

The three-year underlying earnings growth at Renishaw (LON:RSW) is promising, but the shareholders are still in the red over that time

While it may not be enough for some shareholders, we think it is good to see the Renishaw plc (LON:RSW) share price up 16% in a single quarter. But that cannot eclipse the less-than-impressive returns over the last three years. In fact, the share price is down 37% in the last three years, falling well short of the market return.

Since Renishaw has shed UK£127m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

See our latest analysis for Renishaw

While markets are a powerful pricing mechanism, share prices reflect investor sentiment, not just underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

During the unfortunate three years of share price decline, Renishaw actually saw its earnings per share (EPS) improve by 29% per year. This is quite a puzzle, and suggests there might be something temporarily buoying the share price. Or else the company was over-hyped in the past, and so its growth has disappointed.

Since the change in EPS doesn't seem to correlate with the change in share price, it's worth taking a look at other metrics.

With a rather small yield of just 1.9% we doubt that the stock's share price is based on its dividend. We note that, in three years, revenue has actually grown at a 9.1% annual rate, so that doesn't seem to be a reason to sell shares. It's probably worth investigating Renishaw further; while we may be missing something on this analysis, there might also be an opportunity.

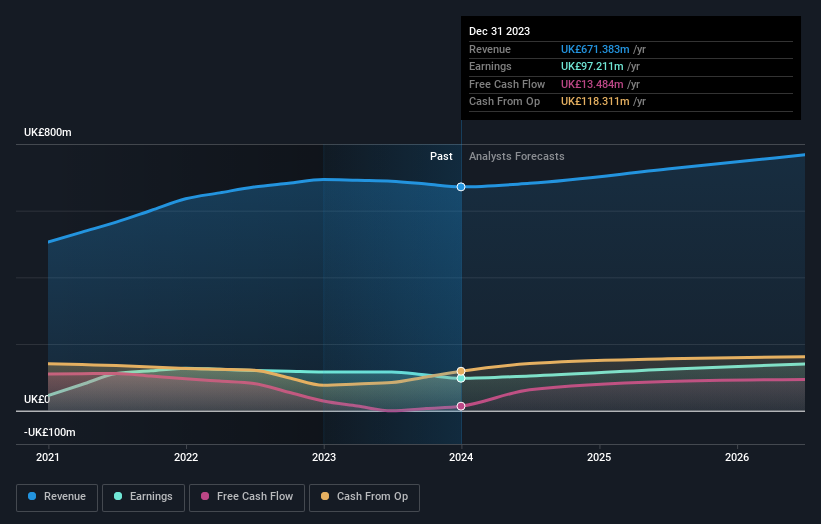

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. It's always worth keeping an eye on CEO pay, but a more important question is whether the company will grow earnings throughout the years. So it makes a lot of sense to check out what analysts think Renishaw will earn in the future (free profit forecasts).

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. As it happens, Renishaw's TSR for the last 3 years was -33%, which exceeds the share price return mentioned earlier. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

It's good to see that Renishaw has rewarded shareholders with a total shareholder return of 11% in the last twelve months. That's including the dividend. That certainly beats the loss of about 1.0% per year over the last half decade. This makes us a little wary, but the business might have turned around its fortunes. Before deciding if you like the current share price, check how Renishaw scores on these 3 valuation metrics.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on British exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether Renishaw is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About LSE:RSW

Renishaw

Renishaw plc, an engineering and scientific technology company, designs, manufactures, distributes, sells, and services technological products and services, and analytical instruments and medical devices worldwide.

Excellent balance sheet with moderate growth potential.