Stock Analysis

- Hungary

- /

- Renewable Energy

- /

- BUSE:ALTEO

The Market Lifts ALTEO Energy Services Public Limited Company (BUSE:ALTEO) Shares 27% But It Can Do More

The ALTEO Energy Services Public Limited Company (BUSE:ALTEO) share price has done very well over the last month, posting an excellent gain of 27%. Taking a wider view, although not as strong as the last month, the full year gain of 25% is also fairly reasonable.

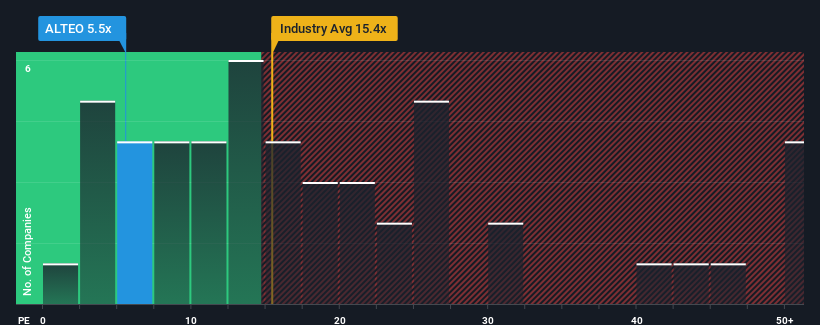

Even after such a large jump in price, given about half the companies in Hungary have price-to-earnings ratios (or "P/E's") above 13x, you may still consider ALTEO Energy Services as a highly attractive investment with its 5.5x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

For instance, ALTEO Energy Services' receding earnings in recent times would have to be some food for thought. It might be that many expect the disappointing earnings performance to continue or accelerate, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for ALTEO Energy Services

How Is ALTEO Energy Services' Growth Trending?

There's an inherent assumption that a company should far underperform the market for P/E ratios like ALTEO Energy Services' to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 1.3%. Even so, admirably EPS has lifted 1,941% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

This is in contrast to the rest of the market, which is expected to grow by 16% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's peculiar that ALTEO Energy Services' P/E sits below the majority of other companies. It looks like most investors are not convinced the company can maintain its recent growth rates.

The Final Word

Shares in ALTEO Energy Services are going to need a lot more upward momentum to get the company's P/E out of its slump. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that ALTEO Energy Services currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. There could be some major unobserved threats to earnings preventing the P/E ratio from matching this positive performance. It appears many are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

Having said that, be aware ALTEO Energy Services is showing 1 warning sign in our investment analysis, you should know about.

You might be able to find a better investment than ALTEO Energy Services. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're helping make it simple.

Find out whether ALTEO Energy Services is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BUSE:ALTEO

ALTEO Energy Services

ALTEO Energy Services Public Limited Company generates and sells electricity and heat in Hungary.

Flawless balance sheet and good value.