Stock Analysis

- Spain

- /

- Renewable Energy

- /

- BME:SLR

The Market Doesn't Like What It Sees From Solaria Energía y Medio Ambiente, S.A.'s (BME:SLR) Earnings Yet

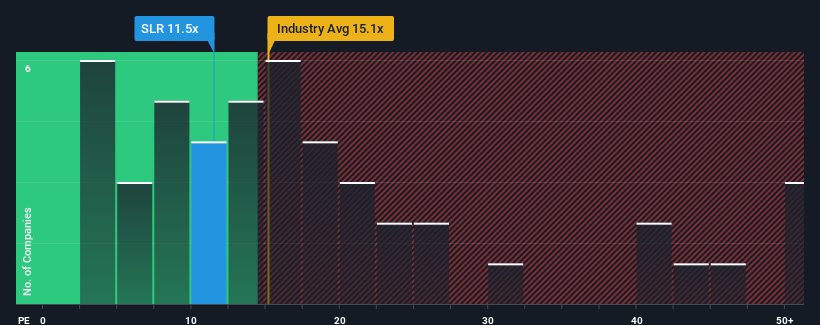

With a price-to-earnings (or "P/E") ratio of 11.5x Solaria Energía y Medio Ambiente, S.A. (BME:SLR) may be sending bullish signals at the moment, given that almost half of all companies in Spain have P/E ratios greater than 16x and even P/E's higher than 31x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With earnings growth that's superior to most other companies of late, Solaria Energía y Medio Ambiente has been doing relatively well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Solaria Energía y Medio Ambiente

What Are Growth Metrics Telling Us About The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Solaria Energía y Medio Ambiente's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered an exceptional 19% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 254% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 7.5% per year during the coming three years according to the analysts following the company. With the market predicted to deliver 12% growth each year, the company is positioned for a weaker earnings result.

With this information, we can see why Solaria Energía y Medio Ambiente is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Solaria Energía y Medio Ambiente's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Solaria Energía y Medio Ambiente (2 are significant) you should be aware of.

Of course, you might also be able to find a better stock than Solaria Energía y Medio Ambiente. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're helping make it simple.

Find out whether Solaria Energía y Medio Ambiente is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:SLR

Solaria Energía y Medio Ambiente

Solaria Energía y Medio Ambiente, S.A., together with its subsidiaries, engages in the generation of solar photovoltaic energy.

Fair value with moderate growth potential.