Stock Analysis

- India

- /

- Capital Markets

- /

- NSEI:BSE

Subdued Growth No Barrier To BSE Limited (NSE:BSE) With Shares Advancing 41%

BSE Limited (NSE:BSE) shareholders would be excited to see that the share price has had a great month, posting a 41% gain and recovering from prior weakness. The last 30 days were the cherry on top of the stock's 516% gain in the last year, which is nothing short of spectacular.

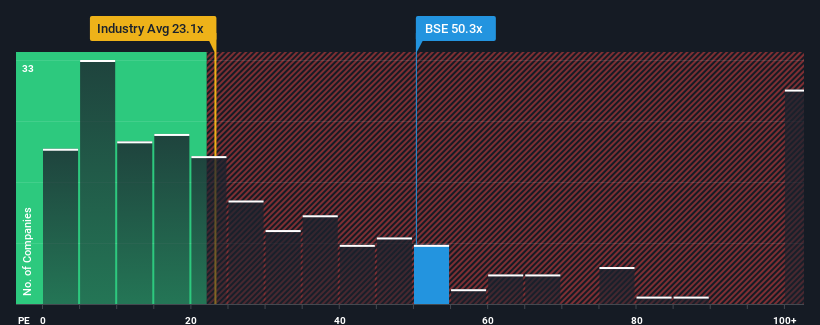

Following the firm bounce in price, BSE's price-to-earnings (or "P/E") ratio of 50.3x might make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 31x and even P/E's below 17x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, BSE has been doing relatively well. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for BSE

Is There Enough Growth For BSE?

There's an inherent assumption that a company should far outperform the market for P/E ratios like BSE's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 274% last year. The latest three year period has also seen an excellent 603% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 6.8% over the next year. That's shaping up to be materially lower than the 24% growth forecast for the broader market.

In light of this, it's alarming that BSE's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Final Word

Shares in BSE have built up some good momentum lately, which has really inflated its P/E. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that BSE currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

You always need to take note of risks, for example - BSE has 2 warning signs we think you should be aware of.

If these risks are making you reconsider your opinion on BSE, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're helping make it simple.

Find out whether BSE is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BSE

BSE

BSE Limited, together with its subsidiaries, provides a platform for trading in equity, debt instruments, derivatives, and mutual funds in India and internationally.

Excellent balance sheet with reasonable growth potential.