Stock Analysis

- Norway

- /

- Marine and Shipping

- /

- OB:SNI

Stolt-Nielsen Limited (OB:SNI) Surges 26% Yet Its Low P/E Is No Reason For Excitement

Despite an already strong run, Stolt-Nielsen Limited (OB:SNI) shares have been powering on, with a gain of 26% in the last thirty days. The last 30 days bring the annual gain to a very sharp 43%.

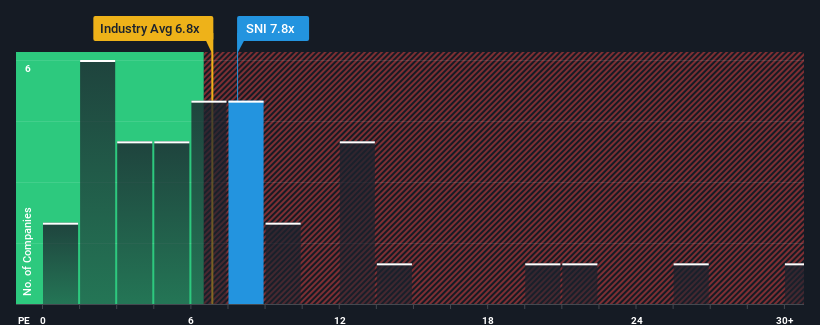

In spite of the firm bounce in price, given about half the companies in Norway have price-to-earnings ratios (or "P/E's") above 12x, you may still consider Stolt-Nielsen as an attractive investment with its 7.8x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

While the market has experienced earnings growth lately, Stolt-Nielsen's earnings have gone into reverse gear, which is not great. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

See our latest analysis for Stolt-Nielsen

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Stolt-Nielsen's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 8.4% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 448% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Turning to the outlook, the next three years should generate growth of 8.1% each year as estimated by the five analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 19% each year, which is noticeably more attractive.

In light of this, it's understandable that Stolt-Nielsen's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Despite Stolt-Nielsen's shares building up a head of steam, its P/E still lags most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Stolt-Nielsen maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Stolt-Nielsen that you need to be mindful of.

If you're unsure about the strength of Stolt-Nielsen's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're helping make it simple.

Find out whether Stolt-Nielsen is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:SNI

Stolt-Nielsen

Stolt-Nielsen Limited, together with its subsidiaries, provides transportation, storage, and distribution solutions for bulk liquid chemicals, edible oils, acids, and other specialty liquids worldwide.

Average dividend payer with mediocre balance sheet.