Stock Analysis

- France

- /

- Hospitality

- /

- ENXTPA:SFCA

Société Française de Casinos Société Anonyme's (EPA:SFCA) Share Price Is Matching Sentiment Around Its Earnings

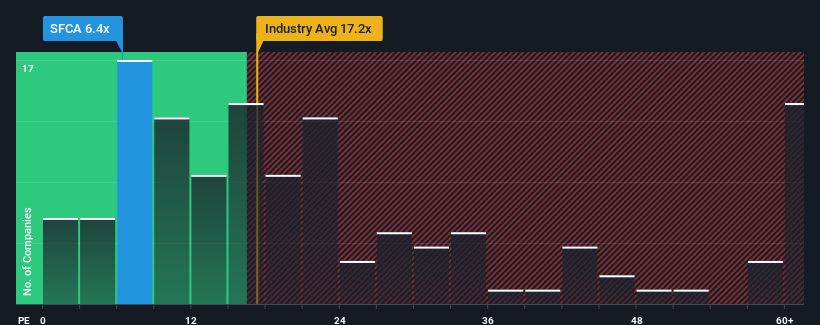

Société Française de Casinos Société Anonyme's (EPA:SFCA) price-to-earnings (or "P/E") ratio of 6.4x might make it look like a strong buy right now compared to the market in France, where around half of the companies have P/E ratios above 16x and even P/E's above 28x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

For example, consider that Société Française de Casinos Société Anonyme's financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

See our latest analysis for Société Française de Casinos Société Anonyme

Is There Any Growth For Société Française de Casinos Société Anonyme?

Société Française de Casinos Société Anonyme's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 22%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 16% shows it's noticeably less attractive on an annualised basis.

In light of this, it's understandable that Société Française de Casinos Société Anonyme's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Key Takeaway

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Société Française de Casinos Société Anonyme revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 2 warning signs for Société Française de Casinos Société Anonyme (1 doesn't sit too well with us!) that you should be aware of.

Of course, you might also be able to find a better stock than Société Française de Casinos Société Anonyme. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're helping make it simple.

Find out whether Société Française de Casinos Société Anonyme is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:SFCA

Société Française de Casinos Société Anonyme

Société Française de Casinos Société Anonyme operates casinos in France.

Flawless balance sheet and good value.