Stock Analysis

- United Kingdom

- /

- Medical Equipment

- /

- LSE:SN.

Smith & Nephew plc (LON:SN.) Not Flying Under The Radar

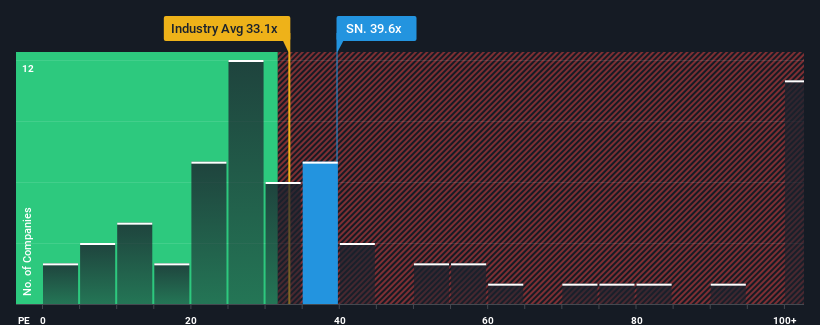

With a price-to-earnings (or "P/E") ratio of 39.6x Smith & Nephew plc (LON:SN.) may be sending very bearish signals at the moment, given that almost half of all companies in the United Kingdom have P/E ratios under 16x and even P/E's lower than 9x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Smith & Nephew certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Smith & Nephew

Is There Enough Growth For Smith & Nephew?

In order to justify its P/E ratio, Smith & Nephew would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered an exceptional 18% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen a very unpleasant 41% drop in EPS in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 45% per annum as estimated by the analysts watching the company. That's shaping up to be materially higher than the 14% per annum growth forecast for the broader market.

In light of this, it's understandable that Smith & Nephew's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Smith & Nephew maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

Plus, you should also learn about these 3 warning signs we've spotted with Smith & Nephew (including 1 which is significant).

You might be able to find a better investment than Smith & Nephew. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're helping make it simple.

Find out whether Smith & Nephew is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About LSE:SN.

Smith & Nephew

Smith & Nephew plc, together with its subsidiaries, develops, manufactures, markets, and sells medical devices and services in the United Kingdom and internationally.

Good value with reasonable growth potential.