Stock Analysis

- Sweden

- /

- Interactive Media and Services

- /

- OM:BUSER

Risks Still Elevated At These Prices As Bambuser AB (publ) (STO:BUSER) Shares Dive 28%

Unfortunately for some shareholders, the Bambuser AB (publ) (STO:BUSER) share price has dived 28% in the last thirty days, prolonging recent pain. For any long-term shareholders, the last month ends a year to forget by locking in a 79% share price decline.

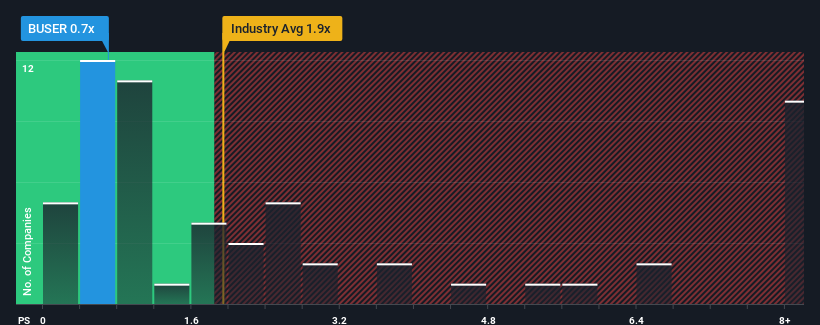

Although its price has dipped substantially, it's still not a stretch to say that Bambuser's price-to-sales (or "P/S") ratio of 0.7x right now seems quite "middle-of-the-road" compared to the Interactive Media and Services industry in Sweden, where the median P/S ratio is around 1.1x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Bambuser

How Bambuser Has Been Performing

While the industry has experienced revenue growth lately, Bambuser's revenue has gone into reverse gear, which is not great. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Bambuser will help you uncover what's on the horizon.How Is Bambuser's Revenue Growth Trending?

In order to justify its P/S ratio, Bambuser would need to produce growth that's similar to the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 14%. In spite of this, the company still managed to deliver immense revenue growth over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company, but investors will want to ask why it is now in decline.

Looking ahead now, revenue is anticipated to climb by 4.7% during the coming year according to the one analyst following the company. With the industry predicted to deliver 27% growth, the company is positioned for a weaker revenue result.

With this information, we find it interesting that Bambuser is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Final Word

Bambuser's plummeting stock price has brought its P/S back to a similar region as the rest of the industry. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look at the analysts forecasts of Bambuser's revenue prospects has shown that its inferior revenue outlook isn't negatively impacting its P/S as much as we would have predicted. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Bambuser that you should be aware of.

If these risks are making you reconsider your opinion on Bambuser, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're helping make it simple.

Find out whether Bambuser is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BUSER

Bambuser

Bambuser AB (publ) develops and provides solutions for live streaming in Sweden.

Flawless balance sheet and slightly overvalued.