Stock Analysis

- Poland

- /

- Electrical

- /

- WSE:RSP

Remor Solar Polska S.A.'s (WSE:RSP) Earnings Haven't Escaped The Attention Of Investors

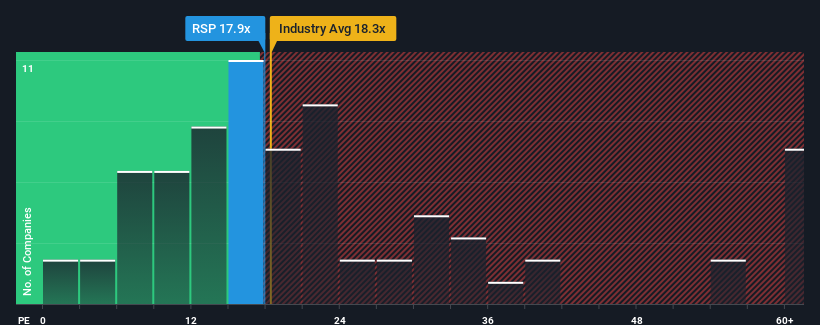

When close to half the companies in Poland have price-to-earnings ratios (or "P/E's") below 12x, you may consider Remor Solar Polska S.A. (WSE:RSP) as a stock to potentially avoid with its 17.9x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

The recent earnings growth at Remor Solar Polska would have to be considered satisfactory if not spectacular. One possibility is that the P/E is high because investors think this good earnings growth will be enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Remor Solar Polska

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Remor Solar Polska would need to produce impressive growth in excess of the market.

If we review the last year of earnings growth, the company posted a worthy increase of 2.8%. Pleasingly, EPS has also lifted 229% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Comparing that to the market, which is only predicted to deliver 5.3% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

In light of this, it's understandable that Remor Solar Polska's P/E sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Key Takeaway

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Remor Solar Polska revealed its three-year earnings trends are contributing to its high P/E, given they look better than current market expectations. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

You always need to take note of risks, for example - Remor Solar Polska has 2 warning signs we think you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're helping make it simple.

Find out whether Remor Solar Polska is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About WSE:RSP

Remor Solar Polska

Remor Solar Polska S.A. engages in design and implementation of projects to install photovoltaic ground and roof structure systems in Poland.

Flawless balance sheet and fair value.