Stock Analysis

- Chile

- /

- Infrastructure

- /

- SNSE:FROWARD

Portuaria Cabo Froward S.A.'s (SNSE:FROWARD) Shares Climb 29% But Its Business Is Yet to Catch Up

Portuaria Cabo Froward S.A. (SNSE:FROWARD) shareholders have had their patience rewarded with a 29% share price jump in the last month. Taking a wider view, although not as strong as the last month, the full year gain of 16% is also fairly reasonable.

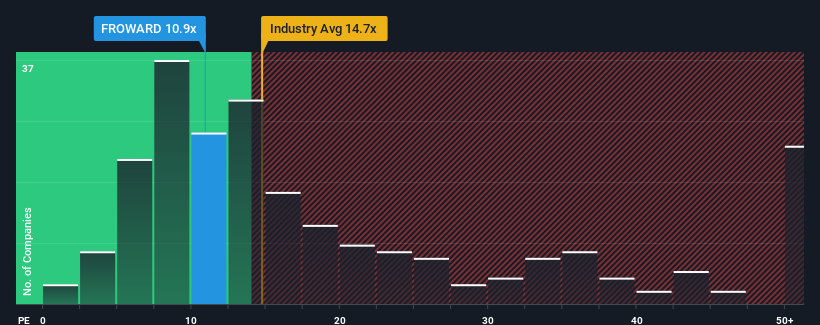

Since its price has surged higher, Portuaria Cabo Froward may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 10.9x, since almost half of all companies in Chile have P/E ratios under 8x and even P/E's lower than 6x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

For example, consider that Portuaria Cabo Froward's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

Check out our latest analysis for Portuaria Cabo Froward

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as high as Portuaria Cabo Froward's is when the company's growth is on track to outshine the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 11%. This means it has also seen a slide in earnings over the longer-term as EPS is down 37% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 13% shows it's an unpleasant look.

In light of this, it's alarming that Portuaria Cabo Froward's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Bottom Line On Portuaria Cabo Froward's P/E

The large bounce in Portuaria Cabo Froward's shares has lifted the company's P/E to a fairly high level. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Portuaria Cabo Froward revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Portuaria Cabo Froward (1 makes us a bit uncomfortable) you should be aware of.

If you're unsure about the strength of Portuaria Cabo Froward's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're helping make it simple.

Find out whether Portuaria Cabo Froward is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SNSE:FROWARD

Portuaria Cabo Froward

Portuaria Cabo Froward S.A. provides port services in Chile.

Flawless balance sheet, good value and pays a dividend.