Stock Analysis

Optimistic Investors Push Dufu Technology Corp. Berhad (KLSE:DUFU) Shares Up 28% But Growth Is Lacking

Dufu Technology Corp. Berhad (KLSE:DUFU) shareholders would be excited to see that the share price has had a great month, posting a 28% gain and recovering from prior weakness. While recent buyers may be laughing, long-term holders might not be as pleased since the recent gain only brings the stock back to where it started a year ago.

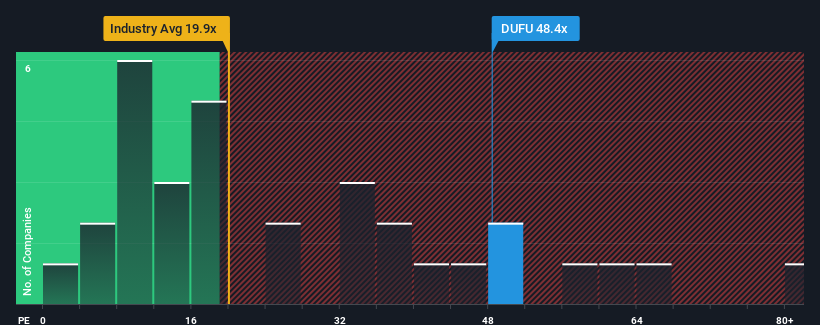

Following the firm bounce in price, Dufu Technology Berhad may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 48.4x, since almost half of all companies in Malaysia have P/E ratios under 16x and even P/E's lower than 10x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

For example, consider that Dufu Technology Berhad's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

View our latest analysis for Dufu Technology Berhad

How Is Dufu Technology Berhad's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as Dufu Technology Berhad's is when the company's growth is on track to outshine the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 64%. As a result, earnings from three years ago have also fallen 54% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 17% shows it's an unpleasant look.

With this information, we find it concerning that Dufu Technology Berhad is trading at a P/E higher than the market. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

What We Can Learn From Dufu Technology Berhad's P/E?

Shares in Dufu Technology Berhad have built up some good momentum lately, which has really inflated its P/E. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Dufu Technology Berhad currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

You should always think about risks. Case in point, we've spotted 2 warning signs for Dufu Technology Berhad you should be aware of, and 1 of them can't be ignored.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're helping make it simple.

Find out whether Dufu Technology Berhad is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:DUFU

Dufu Technology Berhad

Dufu Technology Corp. Berhad, an investment holding company, engages in the manufacture and sale of industrial products.

Excellent balance sheet unattractive dividend payer.