Stock Analysis

- Denmark

- /

- Construction

- /

- CPSE:MTHH

MT Højgaard Holding A/S' (CPH:MTHH) Price Is Right But Growth Is Lacking After Shares Rocket 31%

Despite an already strong run, MT Højgaard Holding A/S (CPH:MTHH) shares have been powering on, with a gain of 31% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 30% in the last year.

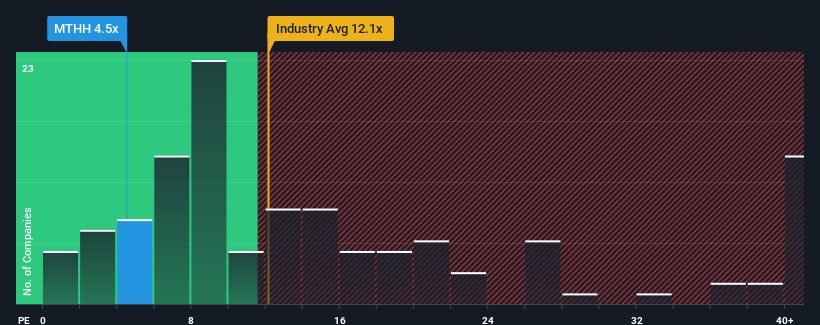

Even after such a large jump in price, MT Højgaard Holding's price-to-earnings (or "P/E") ratio of 4.5x might still make it look like a strong buy right now compared to the market in Denmark, where around half of the companies have P/E ratios above 14x and even P/E's above 31x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Recent times have been advantageous for MT Højgaard Holding as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for MT Højgaard Holding

Is There Any Growth For MT Højgaard Holding?

There's an inherent assumption that a company should far underperform the market for P/E ratios like MT Højgaard Holding's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 32% gain to the company's bottom line. The latest three year period has also seen an excellent 9,235% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should bring diminished returns, with earnings decreasing 2.3% per annum as estimated by the only analyst watching the company. That's not great when the rest of the market is expected to grow by 15% per year.

With this information, we are not surprised that MT Højgaard Holding is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From MT Højgaard Holding's P/E?

MT Højgaard Holding's recent share price jump still sees its P/E sitting firmly flat on the ground. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that MT Højgaard Holding maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

And what about other risks? Every company has them, and we've spotted 2 warning signs for MT Højgaard Holding (of which 1 is potentially serious!) you should know about.

Of course, you might also be able to find a better stock than MT Højgaard Holding. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're helping make it simple.

Find out whether MT Højgaard Holding is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About CPSE:MTHH

MT Højgaard Holding

MT Højgaard Holding A/S engages in the construction, civil engineering, and infrastructure businesses in Denmark and internationally.

Solid track record with excellent balance sheet.