Stock Analysis

- New Zealand

- /

- Hospitality

- /

- NZSE:MCK

Millennium & Copthorne Hotels New Zealand Limited (NZSE:MCK) Looks Inexpensive But Perhaps Not Attractive Enough

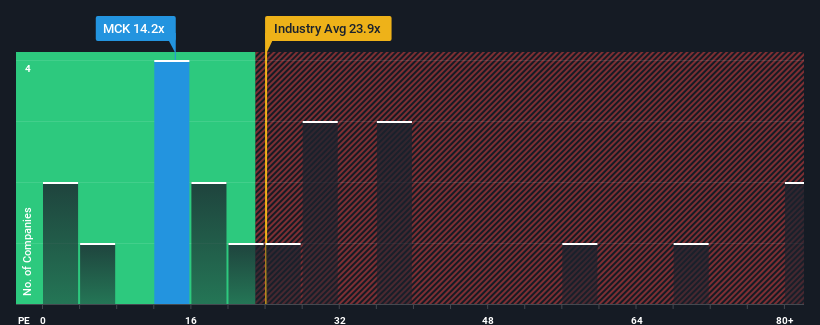

Millennium & Copthorne Hotels New Zealand Limited's (NZSE:MCK) price-to-earnings (or "P/E") ratio of 14.2x might make it look like a buy right now compared to the market in New Zealand, where around half of the companies have P/E ratios above 18x and even P/E's above 32x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

For example, consider that Millennium & Copthorne Hotels New Zealand's financial performance has been pretty ordinary lately as earnings growth is non-existent. It might be that many expect the uninspiring earnings performance to worsen, which has repressed the P/E. If not, then existing shareholders may be feeling optimistic about the future direction of the share price.

Check out our latest analysis for Millennium & Copthorne Hotels New Zealand

What Are Growth Metrics Telling Us About The Low P/E?

Millennium & Copthorne Hotels New Zealand's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Taking a look back first, we see that there was hardly any earnings per share growth to speak of for the company over the past year. The lack of growth did nothing to help the company's aggregate three-year performance, which is an unsavory 55% drop in EPS. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

In contrast to the company, the rest of the market is expected to grow by 21% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

In light of this, it's understandable that Millennium & Copthorne Hotels New Zealand's P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Bottom Line On Millennium & Copthorne Hotels New Zealand's P/E

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Millennium & Copthorne Hotels New Zealand maintains its low P/E on the weakness of its sliding earnings over the medium-term, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Having said that, be aware Millennium & Copthorne Hotels New Zealand is showing 1 warning sign in our investment analysis, you should know about.

Of course, you might also be able to find a better stock than Millennium & Copthorne Hotels New Zealand. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're helping make it simple.

Find out whether Millennium & Copthorne Hotels New Zealand is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:MCK

Millennium & Copthorne Hotels New Zealand

Millennium & Copthorne Hotels New Zealand Limited owns, operates, manages, leases, and franchises hotels in New Zealand and Australia.

Flawless balance sheet and slightly overvalued.