Stock Analysis

- Malta

- /

- Real Estate

- /

- MTSE:MPC

Malta Properties' (MTSE:MPC) Promising Earnings May Rest On Soft Foundations

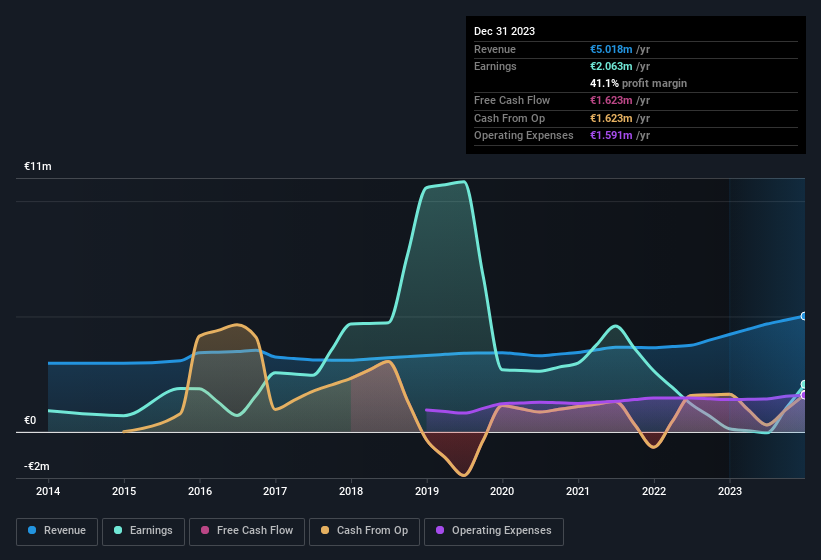

Despite posting some strong earnings, the market for Malta Properties Company p.l.c.'s (MTSE:MPC) stock hasn't moved much. Our analysis suggests that shareholders have noticed something concerning in the numbers.

Check out our latest analysis for Malta Properties

The Impact Of Unusual Items On Profit

To properly understand Malta Properties' profit results, we need to consider the €970k gain attributed to unusual items. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. Which is hardly surprising, given the name. Malta Properties had a rather significant contribution from unusual items relative to its profit to December 2023. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Malta Properties.

Our Take On Malta Properties' Profit Performance

As we discussed above, we think the significant positive unusual item makes Malta Properties' earnings a poor guide to its underlying profitability. For this reason, we think that Malta Properties' statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. The silver lining is that its EPS growth over the last year has been really wonderful, even if it's not a perfect measure. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you want to do dive deeper into Malta Properties, you'd also look into what risks it is currently facing. To that end, you should learn about the 6 warning signs we've spotted with Malta Properties (including 3 which are concerning).

Today we've zoomed in on a single data point to better understand the nature of Malta Properties' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're helping make it simple.

Find out whether Malta Properties is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About MTSE:MPC

Malta Properties

Malta Properties Company p.l.c., together with its subsidiaries, engages in the investment and development of commercial properties in Malta.

Acceptable track record second-rate dividend payer.