Stock Analysis

- Malaysia

- /

- Semiconductors

- /

- KLSE:UNISEM

Investors Appear Satisfied With Unisem (M) Berhad's (KLSE:UNISEM) Prospects

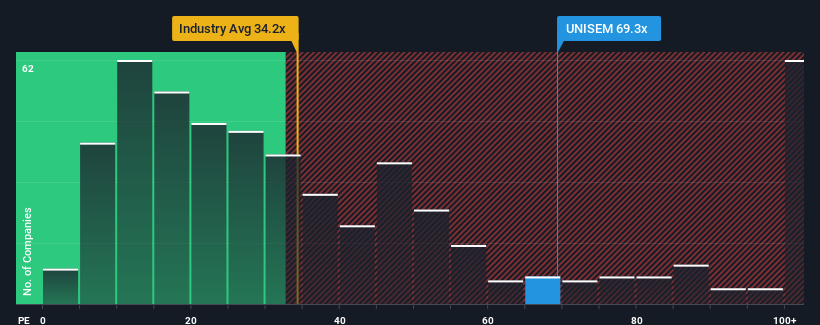

With a price-to-earnings (or "P/E") ratio of 69.3x Unisem (M) Berhad (KLSE:UNISEM) may be sending very bearish signals at the moment, given that almost half of all companies in Malaysia have P/E ratios under 16x and even P/E's lower than 10x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

While the market has experienced earnings growth lately, Unisem (M) Berhad's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Unisem (M) Berhad

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Unisem (M) Berhad would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 66%. The last three years don't look nice either as the company has shrunk EPS by 48% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 44% per annum during the coming three years according to the seven analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 12% per annum, which is noticeably less attractive.

In light of this, it's understandable that Unisem (M) Berhad's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Unisem (M) Berhad's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Unisem (M) Berhad maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Unisem (M) Berhad (1 is a bit unpleasant!) that you need to be mindful of.

If these risks are making you reconsider your opinion on Unisem (M) Berhad, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're helping make it simple.

Find out whether Unisem (M) Berhad is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:UNISEM

Unisem (M) Berhad

Unisem (M) Berhad, together with its subsidiaries, provides semiconductor assembly and test services in Asia, Europe, and the United States.

Excellent balance sheet with reasonable growth potential.