Stock Analysis

Insiders See AU$1.21m Investment In Flexiroam Jump Last Week

Last week, Flexiroam Limited (ASX:FRX) insiders, who had purchased shares in the previous 12 months were rewarded handsomely. The shares increased by 29% last week, resulting in a AU$4.4m increase in the company's market worth, implying a 15% gain on their initial purchase. As a result, their original purchase of AU$1.21m worth of stock is now worth AU$1.39m.

While insider transactions are not the most important thing when it comes to long-term investing, we would consider it foolish to ignore insider transactions altogether.

Check out our latest analysis for Flexiroam

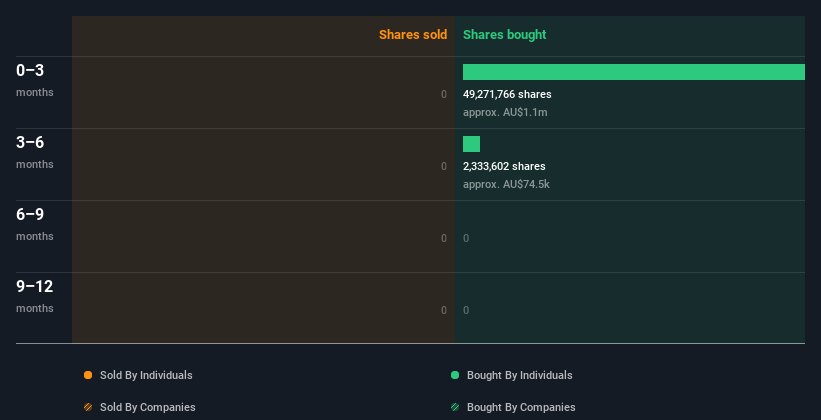

The Last 12 Months Of Insider Transactions At Flexiroam

In the last twelve months, the biggest single purchase by an insider was when Non-Executive Director Stephen Picton bought AU$1m worth of shares at a price of AU$0.023 per share. We do like to see buying, but this purchase was made at well below the current price of AU$0.027. Because it occurred at a lower valuation, it doesn't tell us much about whether insiders might find today's price attractive.

While Flexiroam insiders bought shares during the last year, they didn't sell. The chart below shows insider transactions (by companies and individuals) over the last year. By clicking on the graph below, you can see the precise details of each insider transaction!

Flexiroam is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Insiders At Flexiroam Have Bought Stock Recently

It's good to see that Flexiroam insiders have made notable investments in the company's shares. In total, insiders bought AU$1.1m worth of shares in that time, and we didn't record any sales whatsoever. This is a positive in our book as it implies some confidence.

Insider Ownership

I like to look at how many shares insiders own in a company, to help inform my view of how aligned they are with insiders. I reckon it's a good sign if insiders own a significant number of shares in the company. Flexiroam insiders own 56% of the company, currently worth about AU$11m based on the recent share price. I like to see this level of insider ownership, because it increases the chances that management are thinking about the best interests of shareholders.

So What Does This Data Suggest About Flexiroam Insiders?

It's certainly positive to see the recent insider purchases. And an analysis of the transactions over the last year also gives us confidence. But on the other hand, the company made a loss during the last year, which makes us a little cautious. Along with the high insider ownership, this analysis suggests that insiders are quite bullish about Flexiroam. Nice! While we like knowing what's going on with the insider's ownership and transactions, we make sure to also consider what risks are facing a stock before making any investment decision. For example, Flexiroam has 4 warning signs (and 2 which are significant) we think you should know about.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Valuation is complex, but we're helping make it simple.

Find out whether Flexiroam is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About ASX:FRX

Flexiroam

Flexiroam Limited engages in the telecommunications and Internet of Things (IoT) connectivity business worldwide.

Fair value with moderate growth potential.