Stock Analysis

- Australia

- /

- Capital Markets

- /

- ASX:GQG

Fewer Investors Than Expected Jumping On GQG Partners Inc. (ASX:GQG)

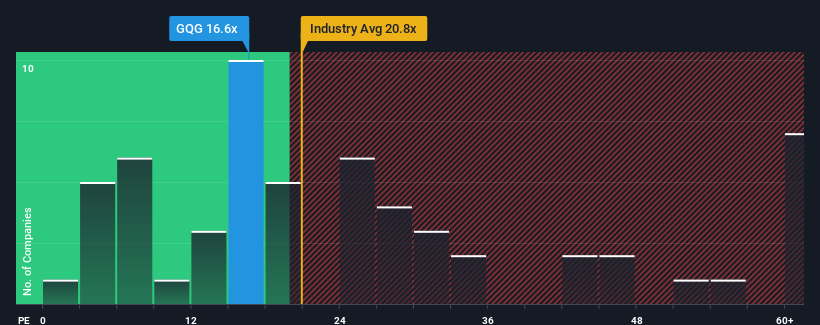

When close to half the companies in Australia have price-to-earnings ratios (or "P/E's") above 21x, you may consider GQG Partners Inc. (ASX:GQG) as an attractive investment with its 16.6x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times have been pleasing for GQG Partners as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for GQG Partners

What Are Growth Metrics Telling Us About The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as GQG Partners' is when the company's growth is on track to lag the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 19% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 97% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 19% per year as estimated by the nine analysts watching the company. That's shaping up to be similar to the 17% each year growth forecast for the broader market.

With this information, we find it odd that GQG Partners is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that GQG Partners currently trades on a lower than expected P/E since its forecast growth is in line with the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

Before you settle on your opinion, we've discovered 1 warning sign for GQG Partners that you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're helping make it simple.

Find out whether GQG Partners is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About ASX:GQG

GQG Partners

GQG Partners Inc. operates as a boutique asset management company worldwide.

Flawless balance sheet and undervalued.