Stock Analysis

- Sweden

- /

- Capital Markets

- /

- OM:EQT

EQT's (STO:EQT) Dividend Will Be Increased To €1.80

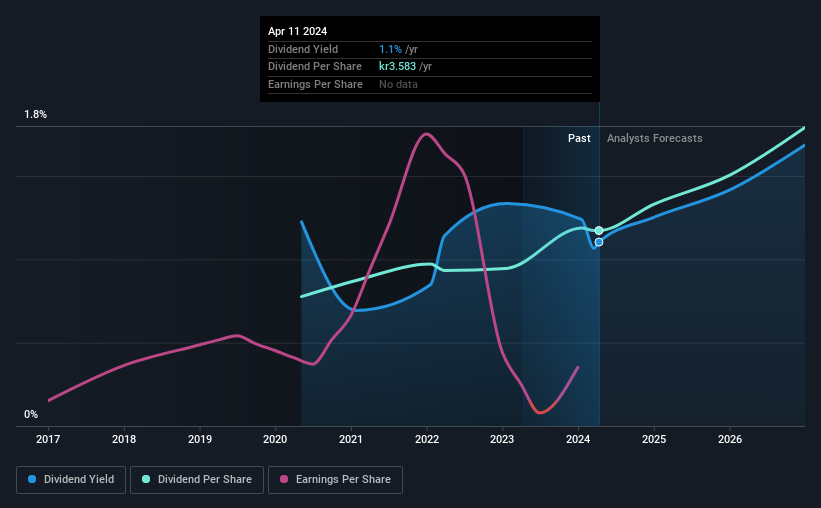

EQT AB (publ) (STO:EQT) will increase its dividend from last year's comparable payment on the 3rd of June to €1.80. Although the dividend is now higher, the yield is only 1.1%, which is below the industry average.

See our latest analysis for EQT

EQT Is Paying Out More Than It Is Earning

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. Prior to this announcement, the company was paying out 276% of what it was earning, however the dividend was quite comfortably covered by free cash flows at a cash payout ratio of only 40%. Generally, we think cash is more important than accounting measures of profit, so with the cash flows easily covering the dividend, we don't think there is much reason to worry.

Earnings per share is forecast to rise exponentially over the next year. Assuming the dividend continues along recent trends, we could see the payout ratio reach 246%, which is on the unsustainable side.

EQT Is Still Building Its Track Record

The dividend has been pretty stable looking back, but the company hasn't been paying one for very long. This makes it tough to judge how it would fare through a full economic cycle. The dividend has gone from an annual total of €0.206 in 2020 to the most recent total annual payment of €0.311. This works out to be a compound annual growth rate (CAGR) of approximately 11% a year over that time. The dividend has been growing rapidly, however with such a short payment history we can't know for sure if payment can continue to grow over the long term, so caution may be warranted.

Dividend Growth May Be Hard To Come By

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. However, initial appearances might be deceiving. It's not great to see that EQT's earnings per share has fallen at approximately 9.6% per year over the past five years. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this can turn into a longer term trend.

EQT's Dividend Doesn't Look Sustainable

Overall, we always like to see the dividend being raised, but we don't think EQT will make a great income stock. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For instance, we've picked out 2 warning signs for EQT that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're helping make it simple.

Find out whether EQT is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About OM:EQT

EQT

EQT AB (publ) is a global private equity firm specializing in Private Capital & Real Asset segments.

High growth potential with excellent balance sheet.