Stock Analysis

Does Nordic Fibreboard (TAL:SKN1T) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Nordic Fibreboard AS (TAL:SKN1T) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Nordic Fibreboard

What Is Nordic Fibreboard's Debt?

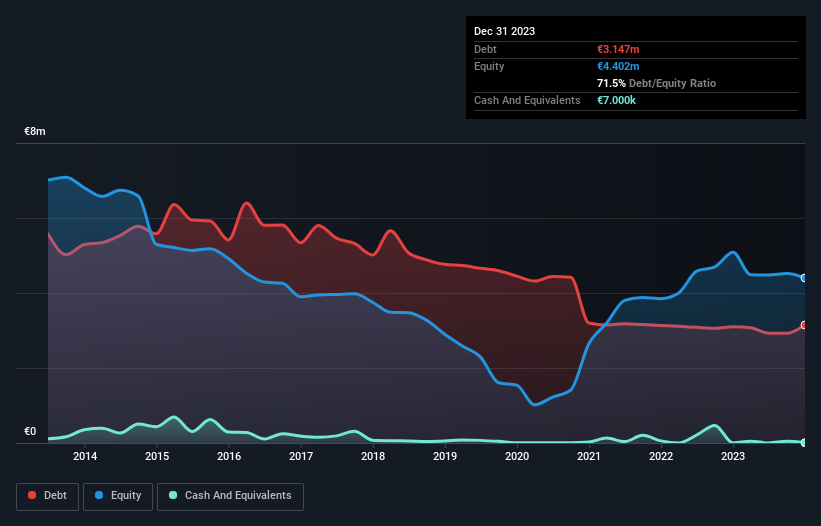

The chart below, which you can click on for greater detail, shows that Nordic Fibreboard had €3.15m in debt in December 2023; about the same as the year before. Net debt is about the same, since the it doesn't have much cash.

How Strong Is Nordic Fibreboard's Balance Sheet?

The latest balance sheet data shows that Nordic Fibreboard had liabilities of €1.53m due within a year, and liabilities of €2.57m falling due after that. On the other hand, it had cash of €7.0k and €450.0k worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by €3.65m.

This deficit is considerable relative to its market capitalization of €3.87m, so it does suggest shareholders should keep an eye on Nordic Fibreboard's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Nordic Fibreboard's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Nordic Fibreboard had a loss before interest and tax, and actually shrunk its revenue by 30%, to €7.7m. That makes us nervous, to say the least.

Caveat Emptor

While Nordic Fibreboard's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping €727k. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. We would feel better if it turned its trailing twelve month loss of €682k into a profit. So we do think this stock is quite risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Nordic Fibreboard you should be aware of, and 1 of them doesn't sit too well with us.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're helping make it simple.

Find out whether Nordic Fibreboard is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TLSE:SKN1T

Nordic Fibreboard

Nordic Fibreboard AS engages in the production and wholesale of building materials.

Mediocre balance sheet and slightly overvalued.