Stock Analysis

- France

- /

- Food and Staples Retail

- /

- ENXTPA:CO

Casino, Guichard-Perrachon S.A. (EPA:CO) Stock's 94% Dive Might Signal An Opportunity But It Requires Some Scrutiny

The Casino, Guichard-Perrachon S.A. (EPA:CO) share price has fared very poorly over the last month, falling by a substantial 94%. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 99% loss during that time.

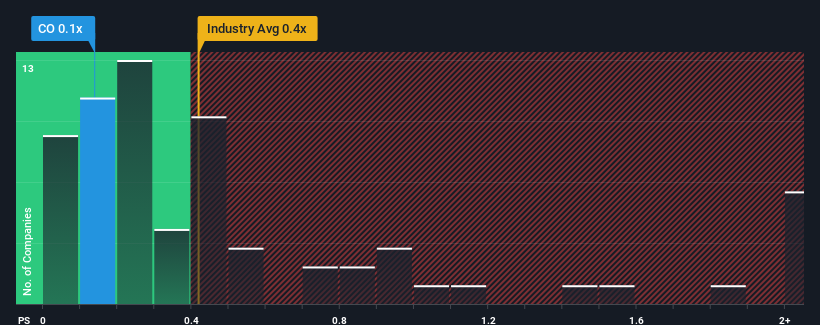

Although its price has dipped substantially, you could still be forgiven for feeling indifferent about Casino Guichard-Perrachon's P/S ratio of 0.1x, since the median price-to-sales (or "P/S") ratio for the Consumer Retailing industry in France is also close to 0.4x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for Casino Guichard-Perrachon

How Casino Guichard-Perrachon Has Been Performing

While the industry has experienced revenue growth lately, Casino Guichard-Perrachon's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

Keen to find out how analysts think Casino Guichard-Perrachon's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Casino Guichard-Perrachon's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 6.2% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 72% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 327% during the coming year according to the three analysts following the company. That's shaping up to be materially higher than the 5.4% growth forecast for the broader industry.

In light of this, it's curious that Casino Guichard-Perrachon's P/S sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

What Does Casino Guichard-Perrachon's P/S Mean For Investors?

Following Casino Guichard-Perrachon's share price tumble, its P/S is just clinging on to the industry median P/S. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Casino Guichard-Perrachon currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

We don't want to rain on the parade too much, but we did also find 4 warning signs for Casino Guichard-Perrachon (2 don't sit too well with us!) that you need to be mindful of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're helping make it simple.

Find out whether Casino Guichard-Perrachon is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:CO

Casino Guichard-Perrachon

Casino, Guichard-Perrachon S.A. operates as a food retailer in France, Latin America, and internationally.

Good value with limited growth.