Stock Analysis

- Australia

- /

- Metals and Mining

- /

- ASX:BCB

Bowen Coking Coal Limited's (ASX:BCB) 25% Dip In Price Shows Sentiment Is Matching Revenues

To the annoyance of some shareholders, Bowen Coking Coal Limited (ASX:BCB) shares are down a considerable 25% in the last month, which continues a horrid run for the company. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 82% loss during that time.

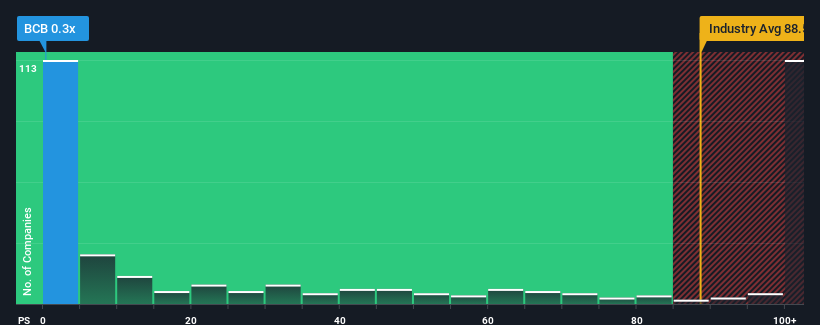

Following the heavy fall in price, Bowen Coking Coal's price-to-sales (or "P/S") ratio of 0.3x might make it look like a strong buy right now compared to the wider Metals and Mining industry in Australia, where around half of the companies have P/S ratios above 88.5x and even P/S above 552x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Check out our latest analysis for Bowen Coking Coal

How Bowen Coking Coal Has Been Performing

With revenue growth that's superior to most other companies of late, Bowen Coking Coal has been doing relatively well. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Keen to find out how analysts think Bowen Coking Coal's future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Bowen Coking Coal would need to produce anemic growth that's substantially trailing the industry.

If we review the last year of revenue growth, we see the company's revenues grew exponentially. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 11% per year as estimated by the dual analysts watching the company. With the industry predicted to deliver 137% growth per annum, the company is positioned for a weaker revenue result.

In light of this, it's understandable that Bowen Coking Coal's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Bowen Coking Coal's P/S?

Bowen Coking Coal's P/S looks about as weak as its stock price lately. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Bowen Coking Coal maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. It's hard to see the share price rising strongly in the near future under these circumstances.

You need to take note of risks, for example - Bowen Coking Coal has 3 warning signs (and 1 which shouldn't be ignored) we think you should know about.

If you're unsure about the strength of Bowen Coking Coal's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're helping make it simple.

Find out whether Bowen Coking Coal is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About ASX:BCB

Bowen Coking Coal

Bowen Coking Coal Limited, together with its subsidiaries, engages in the exploration, development, and production of metallurgical coal in Australia.

Undervalued with high growth potential.