Stock Analysis

- Norway

- /

- Semiconductors

- /

- OB:NOD

Be Wary Of Nordic Semiconductor (OB:NOD) And Its Returns On Capital

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Although, when we looked at Nordic Semiconductor (OB:NOD), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Nordic Semiconductor:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.0063 = US$4.7m ÷ (US$862m - US$114m) (Based on the trailing twelve months to December 2023).

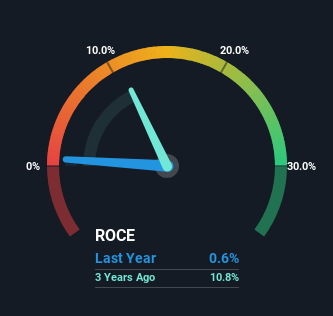

So, Nordic Semiconductor has an ROCE of 0.6%. Ultimately, that's a low return and it under-performs the Semiconductor industry average of 13%.

View our latest analysis for Nordic Semiconductor

In the above chart we have measured Nordic Semiconductor's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Nordic Semiconductor .

What Can We Tell From Nordic Semiconductor's ROCE Trend?

In terms of Nordic Semiconductor's historical ROCE movements, the trend isn't fantastic. Around five years ago the returns on capital were 6.3%, but since then they've fallen to 0.6%. Given the business is employing more capital while revenue has slipped, this is a bit concerning. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

The Bottom Line

From the above analysis, we find it rather worrisome that returns on capital and sales for Nordic Semiconductor have fallen, meanwhile the business is employing more capital than it was five years ago. Since the stock has skyrocketed 141% over the last five years, it looks like investors have high expectations of the stock. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

One final note, you should learn about the 3 warning signs we've spotted with Nordic Semiconductor (including 1 which is a bit concerning) .

While Nordic Semiconductor may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're helping make it simple.

Find out whether Nordic Semiconductor is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About OB:NOD

Nordic Semiconductor

Nordic Semiconductor ASA, a fabless semiconductor company, designs, sells, and delivers integrated circuits (ICs) and related products and services for use in short- and long- range wireless applications in Europe, the Americas, and the Asia Pacific.

Reasonable growth potential with mediocre balance sheet.