Stock Analysis

- Hong Kong

- /

- Marine and Shipping

- /

- SEHK:2490

After Leaping 134% LC Logistics, Inc. (HKG:2490) Shares Are Not Flying Under The Radar

LC Logistics, Inc. (HKG:2490) shareholders have had their patience rewarded with a 134% share price jump in the last month. While recent buyers may be laughing, long-term holders might not be as pleased since the recent gain only brings the stock back to where it started a year ago.

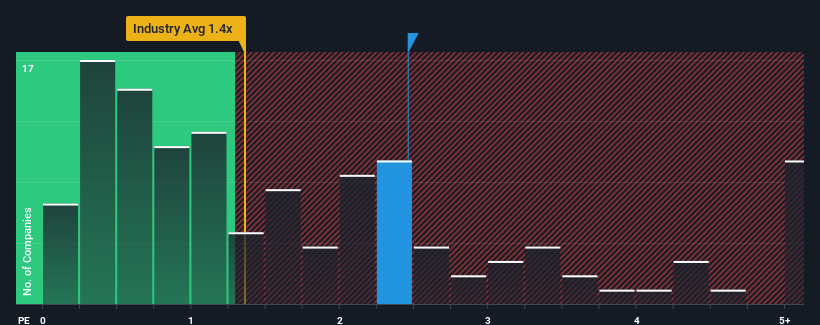

Since its price has surged higher, when almost half of the companies in Hong Kong's Shipping industry have price-to-sales ratios (or "P/S") below 0.9x, you may consider LC Logistics as a stock probably not worth researching with its 2.5x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for LC Logistics

What Does LC Logistics' P/S Mean For Shareholders?

For example, consider that LC Logistics' financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on LC Logistics' earnings, revenue and cash flow.How Is LC Logistics' Revenue Growth Trending?

In order to justify its P/S ratio, LC Logistics would need to produce impressive growth in excess of the industry.

Retrospectively, the last year delivered a frustrating 73% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 58% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

When compared to the industry's one-year growth forecast of 4.9%, the most recent medium-term revenue trajectory is noticeably more alluring

In light of this, it's understandable that LC Logistics' P/S sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Bottom Line On LC Logistics' P/S

LC Logistics shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that LC Logistics maintains its high P/S on the strength of its recent three-year growth being higher than the wider industry forecast, as expected. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. If recent medium-term revenue trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

Plus, you should also learn about this 1 warning sign we've spotted with LC Logistics.

If you're unsure about the strength of LC Logistics' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're helping make it simple.

Find out whether LC Logistics is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About SEHK:2490

LC Logistics

LC Logistics, Inc., a freight forwarding company, provides integrated cross-border seaborne logistics and time charter services worldwide.

Excellent balance sheet with poor track record.