Stock Analysis

- Italy

- /

- Gas Utilities

- /

- BIT:AC5

Acinque's (BIT:AC5) Sluggish Earnings Might Be Just The Beginning Of Its Problems

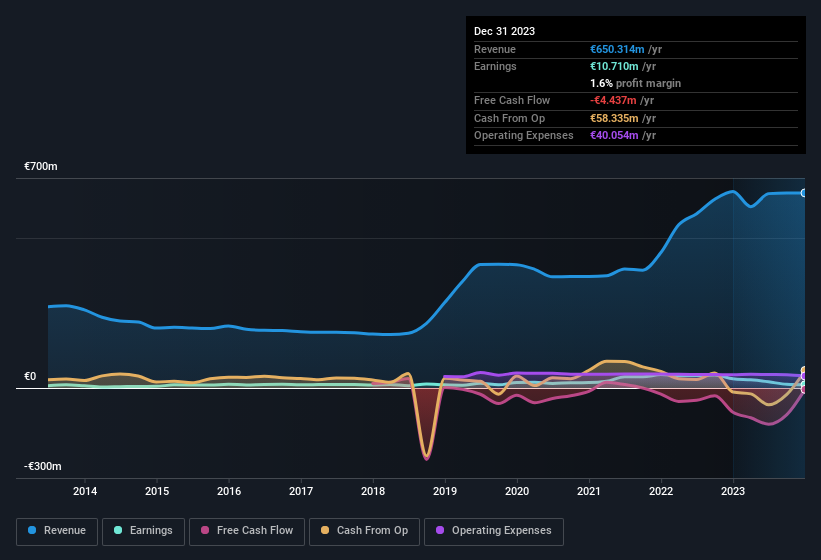

The subdued market reaction suggests that Acinque S.p.A.'s (BIT:AC5) recent earnings didn't contain any surprises. We think that investors are worried about some weaknesses underlying the earnings.

View our latest analysis for Acinque

The Power Of Non-Operating Revenue

Most companies divide classify their revenue as either 'operating revenue', which comes from normal operations, and other revenue, which could include government grants, for example. Oftentimes, non-operating revenue spikes are not repeated, so it makes sense to be cautious where non-operating revenue has made a very large contribution to total profit. Importantly, the non-operating revenue often comes without associated ongoing costs, so it can boost profit by letting it fall straight to the bottom line, making the operating business seem better than it really is. Notably, Acinque had a significant increase in non-operating revenue over the last year. In fact, our data indicates that non-operating revenue increased from €10.9m to €49.9m. If that non-operating revenue fails to manifest in the current year, then there's a real risk the bottom line profit result will be impacted negatively. In order to better understand a company's profit result, it can sometimes help to consider whether the result would be very different without a sudden increase in non-operating revenue.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Acinque.

Our Take On Acinque's Profit Performance

When considering the nature of Acinque's earnings, we'd absolutely keep in mind that it saw an increase in non-operating revenue in the last year, which would in turn have boosted its profit, potentially in an unsustainable manner. Therefore, it seems possible to us that Acinque's true underlying earnings power is actually less than its statutory profit. In further bad news, its earnings per share decreased in the last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Be aware that Acinque is showing 3 warning signs in our investment analysis and 1 of those is concerning...

Today we've zoomed in on a single data point to better understand the nature of Acinque's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're helping make it simple.

Find out whether Acinque is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:AC5

Mediocre balance sheet unattractive dividend payer.