Advertisement

Are Asaleo Care Limited’s (ASX:AHY) Returns Worth Your While?

Today we'll look at Asaleo Care Limited (ASX:AHY) and reflect on its potential as an investment. Specifically, we'll consider its Return On Capital Employed (ROCE), since that will give us an insight into how efficiently the business can generate profits from the capital it requires.

First, we'll go over how we calculate ROCE. Next, we'll compare it to others in its industry. Last but not least, we'll look at what impact its current liabilities have on its ROCE.

What is Return On Capital Employed (ROCE)?

ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. In general, businesses with a higher ROCE are usually better quality. Ultimately, it is a useful but imperfect metric. Renowned investment researcher Michael Mauboussin has suggested that a high ROCE can indicate that 'one dollar invested in the company generates value of more than one dollar'.

How Do You Calculate Return On Capital Employed?

Analysts use this formula to calculate return on capital employed:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for Asaleo Care:

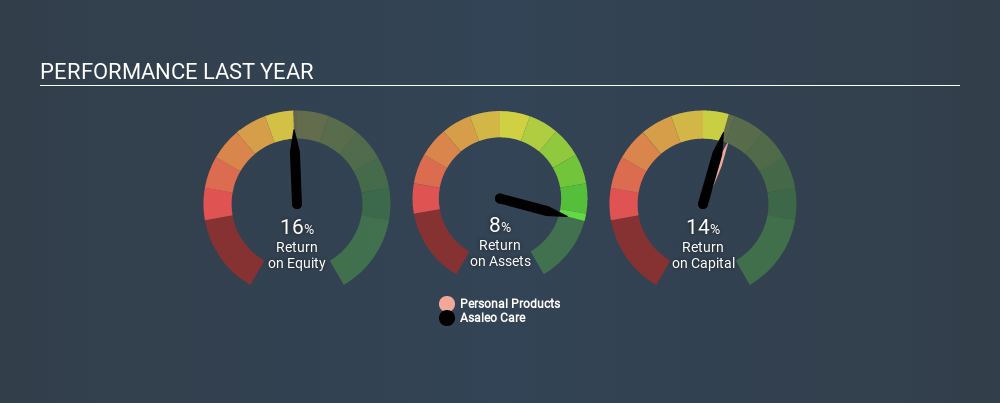

0.14 = AU$54m ÷ (AU$481m - AU$91m) (Based on the trailing twelve months to December 2019.)

Therefore, Asaleo Care has an ROCE of 14%.

Check out our latest analysis for Asaleo Care

Does Asaleo Care Have A Good ROCE?

ROCE can be useful when making comparisons, such as between similar companies. We can see Asaleo Care's ROCE is around the 15% average reported by the Personal Products industry. Separate from Asaleo Care's performance relative to its industry, its ROCE in absolute terms looks satisfactory, and it may be worth researching in more depth.

You can click on the image below to see (in greater detail) how Asaleo Care's past growth compares to other companies.

When considering this metric, keep in mind that it is backwards looking, and not necessarily predictive. ROCE can be misleading for companies in cyclical industries, with returns looking impressive during the boom times, but very weak during the busts. This is because ROCE only looks at one year, instead of considering returns across a whole cycle. What happens in the future is pretty important for investors, so we have prepared a free report on analyst forecasts for Asaleo Care.

Do Asaleo Care's Current Liabilities Skew Its ROCE?

Current liabilities are short term bills and invoices that need to be paid in 12 months or less. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To counter this, investors can check if a company has high current liabilities relative to total assets.

Asaleo Care has current liabilities of AU$91m and total assets of AU$481m. As a result, its current liabilities are equal to approximately 19% of its total assets. A fairly low level of current liabilities is not influencing the ROCE too much.

What We Can Learn From Asaleo Care's ROCE

With that in mind, Asaleo Care's ROCE appears pretty good. Asaleo Care looks strong on this analysis, but there are plenty of other companies that could be a good opportunity . Here is a free list of companies growing earnings rapidly.

I will like Asaleo Care better if I see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5363.1% undervalued

130 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18051.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.323.4% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2451.6% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FA

FA_Trader on SkyWorld Development Berhad ·

SkyWorld Development: RM0.90 target price points to a possible re-rating as earnings recovery begins

Fair Value:RM 0.956.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Janpeo on Amadeus IT Group ·

The "AI Fear" Arbitrage Opportunity

Fair Value:€65.922.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KI

KiwiInvest on NVIDIA ·

NVIDIA's future hinges on $400b revenue and AI software dominance

Fair Value:US$339.935.4% undervalued

188 followersusers have followed this narrative

11 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.6% undervalued

107 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.228.1% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.6% undervalued

1399 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative