Last Update 13 Jun 26

ORX: Overdose Reversal Pipeline Progress Will Support Future Upside

Orexo's SEK price target remains unchanged at SEK 29. Analysts have kept the fair value steady and point to relatively stable assumptions for the discount rate, revenue growth, profit margin and future P/E in their updated work.

What's in the News

- Orexo reported positive pre clinical in vivo data on nasal absorption of atipamezole using its AmorphOX drug delivery technology, supporting development of OX390 as an emergency treatment for overdoses involving xylazine and medetomidine. Source: Company key developments

- The study indicated rapid and substantial intranasal absorption of atipamezole across multiple formulations, with a single nasal dose of OX390 reported to reach the targeted therapeutic exposure range and to establish proof of concept. Source: Company key developments

- The next planned milestone for OX390 is a type C meeting with the FDA to agree on the non clinical development plan that would enable human clinical trials. Source: Company key developments

- OX390 is being developed as a rapidly acting intranasal powder for community use by first responders and laypersons. This development is supported in whole or in part by US federal funds from BARDA under contract number 75A50125C00010. Source: Company key developments

- Orexo held an Analyst/Investor Day, providing a forum for management to update the market and investors on the business and pipeline. Source: Company key developments

Valuation Changes

- Fair Value: SEK 29.0 per share, unchanged from SEK 29.

- Discount Rate: steady at 5.344%.

- Revenue Growth: assumption broadly unchanged at 22.47%.

- Net Profit Margin: trimmed slightly from 20.05% to 19.84%.

- Future P/E: assumption has risen slightly from 186.18x to 188.15x.

Key Takeaways

- Legal settlements and strategic changes stabilize revenue streams, enhancing future planning and financial clarity for Orexo.

- Advancements in product development and strategic partnerships signal potential growth in revenue and net margins.

- Supply chain issues, legal uncertainties, and regulatory challenges threaten to delay product launches, increase costs, and impact profitability and revenue streams.

Catalysts

About Orexo- A specialty pharmaceutical company, develops and commercializes pharmaceuticals and digital therapies in the United States, European Union, and internationally.

- The settlement of the Sun Pharmaceuticals litigation provides Orexo with more certainty in maintaining Zubsolv's revenue stream, eliminating the risk of revenue loss from exclusivity issues. This stabilizes future revenue and allows strategic planning for growth.

- Stabilizing Zubsolv revenue despite challenges in inventory levels with wholesalers suggests a stable or potentially growing revenue stream, underpinning future revenue stability and earnings.

- Progress in clinical trials and favorable data for OX640 suggests potential future growth in revenue from successful product development and market entry, improving future earnings prospects.

- Strategic organizational changes, such as transferring Zubsolv IP and manufacturing rights to a wholly-owned subsidiary, could enhance operational efficiency and financial clarity, potentially improving net margins.

- The resolution with GAIA on digital assets and the focus on other potential partnerships (e.g., Abera) for the AmorphOX technology indicates a strategic pivot towards high-potential growth areas, potentially increasing future revenues and net margins.

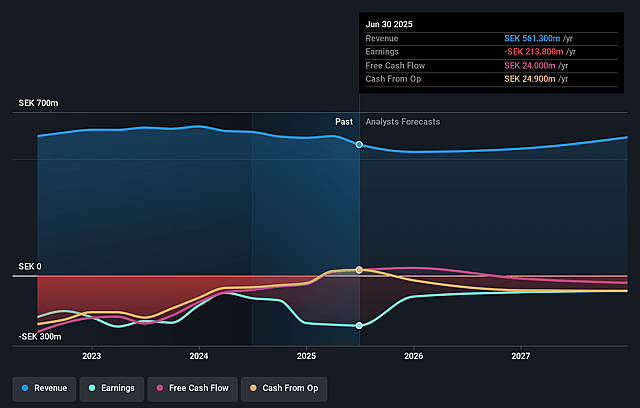

Orexo Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Orexo's revenue will grow by 22.5% annually over the next 3 years.

- Analysts are not forecasting that Orexo will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Orexo's profit margin will increase from -2347.8% to the average GB Pharmaceuticals industry of 19.8% in 3 years.

- If Orexo's profit margin were to converge on the industry average, you could expect earnings to reach SEK 6.5 million (and earnings per share of SEK 0.18) by about June 2029, up from -SEK 417.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 190.4x on those 2029 earnings, up from -1.7x today. This future PE is greater than the current PE for the GB Pharmaceuticals industry at 68.5x.

- Analysts expect the number of shares outstanding to grow by 1.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.34%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Supply chain issues with a critical component supplier for OX124 may delay product launch and approval by the FDA, which could postpone potential revenue streams and negatively impact earnings.

- Legal uncertainties, such as ongoing negotiations with the Department of Justice, may result in settlements or adverse outcomes, potentially affecting financial stability and increasing operating expenses.

- The digital health programs face challenges due to new CMS guidelines requiring FDA registration, needing further investment for clinical evidence. This could impede revenue growth from these assets and require higher expenditures, affecting net margins.

- The dependency on Zubsolv as a major revenue contributor, combined with potential pressures from Medicare changes favoring generics, could introduce variability in revenues and affect profit margins if patients shift to alternatives.

- Impairments and write-downs of digital assets like Deprexis and Vorvida reflect challenges in obtaining reimbursement and market penetration, potentially limiting expected revenue and forcing restructuring costs, affecting overall profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK29.0 for Orexo based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK32.7 million, earnings will come to SEK6.5 million, and it would be trading on a PE ratio of 190.4x, assuming you use a discount rate of 5.3%.

- Given the current share price of SEK20.7, the analyst price target of SEK29.0 is 28.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Orexo?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.