Last Update 24 Jun 26

Fair value Decreased 2.31%9697: Horror IP Pipeline And New Console Cycle Will Support Margins

Analysts updated their Capcom view with a slightly lower fair value estimate of ¥4,236 from ¥4,336, aligning this with a revised Street price target of ¥3,600 from ¥3,700, as they highlight improved profit growth prospects despite the recent share selloff.

What’s in the News for Capcom

- Capcom announced Dragon’s Dogma 2: Dark Arisen, a paid expansion for Dragon’s Dogma 2, scheduled for release on October 9, 2026, with a combined package for Nintendo Switch 2 as part of its multi platform rollout. (Source: company announcement)

- Monster Hunter Wilds: Ascendance, a large expansion for Monster Hunter Wilds, is in development for a planned 2027 release, with new quest ranks, locales, monsters and weapon actions, and a version under development for Nintendo Switch 2. (Source: company announcement)

- Resident Evil Veronica, a remake of Resident Evil Code: Veronica and the latest title in the Resident Evil series, is scheduled for release in 2027 with a reimagined story and updated graphics using Capcom’s RE ENGINE. (Source: company announcement)

- Onimusha: Way of the Sword, the first new Onimusha title in over 20 years, is scheduled to launch on September 25, 2026, with a playable demo already available and pre orders open, while the Windows version is planned for a later date. (Source: company announcement)

- Capcom’s board is set to consider disposal of treasury shares as restricted stock remuneration for external directors, alongside previously announced revisions to the director remuneration system. (Source: board meeting disclosures)

Valuation Changes for Capcom

- Fair Value: revised slightly lower to ¥4,236.47 from ¥4,336.47 per share.

- Discount Rate: adjusted marginally lower to 6.65% from 6.77%.

- Revenue Growth: updated to 9.24% from 8.59% in the underlying model assumptions.

- Net Profit Margin: now set at 30.72%, compared with the prior 31.24% assumption.

- Future P/E: valuation multiple in the model reduced modestly to 27.45x from 28.23x.

Key Takeaways

- Expanding globally, especially in emerging markets and digital platforms, is expected to grow Capcom's revenues and international presence.

- Diversified content strategies and investment in talent and technology aim to boost operational efficiency, broaden audiences, and stabilize recurring income.

- Heavy reliance on core franchises, rising talent and development costs, and industry consolidation threaten Capcom's margins, growth prospects, and overall earnings stability.

Catalysts

About Capcom- Plans, develops, manufactures, sells, and distributes home video games, online games, mobile games, and arcade games in Japan and internationally.

- Capcom's strategy to accelerate global expansion-particularly in emerging markets and through increased support for PC platforms-directly positions the company to capitalize on the ongoing growth in the worldwide gaming population, driving long-term revenue and potential international earnings growth.

- The continued shift toward digital content distribution, highlighted by robust catalog sales and increasing digital penetration globally, is expected to support both revenue growth and higher operating margins by lowering distribution costs and expanding the addressable market.

- Multi-pronged brand and IP strategies-including sequels, remakes, collaborations, transmedia content (e.g., Netflix anime, Amazon Prime animation), and eSports-are set to broaden Capcom's user base and diversify recurring revenue streams, boosting both topline growth and earnings stability.

- Investment in expanding in-house development capacity and updating proprietary technology (new development buildings, improved RE Engine) is poised to improve production efficiency and foster higher operating leverage, supporting margin improvement and sustainable earnings growth.

- Sustained focus on workforce expansion, talent development, and diversity is set to alleviate creative/talent bottlenecks and enhance operational resilience, underpinning Capcom's ability to deliver consistent pipeline expansion and future revenue growth.

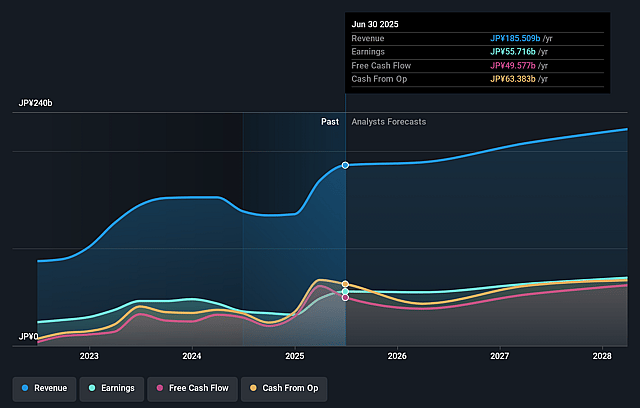

Capcom Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Capcom's revenue will grow by 9.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 27.9% today to 30.7% in 3 years time.

- Analysts expect earnings to reach ¥78.2 billion (and earnings per share of ¥187.3) by about June 2029, up from ¥54.6 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ¥87.4 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 27.5x on those 2029 earnings, up from 21.9x today. This future PE is greater than the current PE for the JP Entertainment industry at 14.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.65%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Overdependence on established franchises like Resident Evil, Monster Hunter, and Street Fighter increases the risk of franchise fatigue and could lead to stagnating or declining sales if new titles or remakes fail to meet consumer expectations, thereby impacting revenue growth and earnings stability.

- Significant investment in human capital, including rising average salaries and ongoing hiring, could materially increase labor costs; when combined with potential global talent shortages in technology and creative roles, these factors may pressure net margins and reduce operating leverage.

- With rapid expansion into new physical locations in the Arcade Operations segment and continued capital outlay for new development facilities, Capcom faces heightened exposure to cyclical downturns or operational inefficiencies, which may depress margins and erode profitability if either segment underperforms.

- Escalating development costs and longer production timelines for high-quality AAA titles heighten financial risk, as each major release carries a greater impact on annual results and may drive more volatile quarterly earnings if a single project underperforms or faces delays.

- Intensifying industry consolidation enables larger competitors to achieve greater scale, negotiating power, and exclusive access to technology and distribution networks, increasing the risk that Capcom could lose market share, face pressure on revenues from reduced visibility, or experience erosion of future earnings capacity.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ¥4236.47 for Capcom based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥4950.0, and the most bearish reporting a price target of just ¥3500.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ¥254.7 billion, earnings will come to ¥78.2 billion, and it would be trading on a PE ratio of 27.5x, assuming you use a discount rate of 6.7%.

- Given the current share price of ¥2864.0, the analyst price target of ¥4236.47 is 32.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Capcom?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.