Last Update 02 Jun 26

Fair value Decreased 12%OMDA: Q4 Execution And 2026 Guidance Conservatism Will Shape Future Upside Potential

Narrative Update on Omda

The updated analyst price target for Omda shifts from a fair value of NOK57.00 to NOK50.00 as analysts factor in a higher discount rate, more cautious revenue growth assumptions, improved profit margin expectations, and a lower future P/E multiple.

Analyst Commentary

Recent Street research on Omda highlights a mix of optimism about growth and execution, paired with more cautious valuation assumptions and price target resets. Taken together, the commentary points to interest in the company’s exposure to GLP-1 trends, multi-condition programs, and guidance through 2026, while also acknowledging pressure on sector valuations.

Bullish Takeaways

- Bullish analysts point to strong Q4 results, including what they describe as an 8% revenue beat and a US$7m EBITDA beat, as evidence that execution is tracking ahead of prior expectations.

- Several reports highlight momentum across all programs and new product launches, with some analysts framing Omda as demonstrating that its growth is not solely reliant on the GLP-1 category.

- Bullish analysts note that Q4 revenue and member trends are supported by GLP-1 adoption and multi-condition adoption. They view this as a foundation for continued growth into the company’s fiscal 2026 outlook.

- Some commentary suggests that guidance, including 2026 targets, may include pockets of conservatism. These analysts view that conservatism as leaving room for upside if execution continues at a similar pace.

Bearish Takeaways

- Several research notes reduce price targets. While ratings remain positive in many cases, analysts are reassessing what they are willing to pay for that growth in light of updated models.

- Bearish analysts flag ongoing valuation pressure across Healthcare Information Technology stocks, which can cap near term multiples even when company specific fundamentals are viewed positively.

- Some commentary focuses on a key debate around how conservative fiscal 2026 guidance actually is. These notes suggest that if growth or profitability tracks closer to the low end of expectations, upside to current valuation may be more limited.

- Price target cuts immediately following Q4 results and guidance updates indicate that, despite strong backward looking metrics, analysts are treating forward assumptions and sector-wide sentiment with caution.

What's in the News

- Omda plans to present a proposal at its annual general meeting on April 28, 2026, for shareholders to adopt formal articles of association for a nomination and remuneration committee, focusing on board nominations and compensation decisions. Source: Company key developments

- The proposed nomination committee structure would include 3 to 5 members, with a majority independent of the board and management, and explicitly excludes the chief executive officer from membership. Source: Company key developments

- Under the proposal, the nomination committee would recommend board and committee members, set related remuneration, engage with larger shareholders, and publish member information and proposal deadlines on Omda’s website to increase transparency. Source: Company key developments

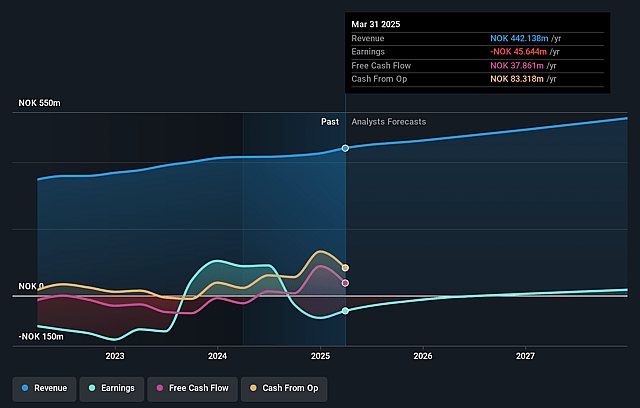

- Omda has reiterated its 2026 guidance and currently expects revenue between NOK 500 million and NOK 525 million for the year. Source: Company key developments

Valuation Changes

- Fair Value: Analyst fair value estimate moves from NOK57.00 to NOK50.00, a reduction of roughly 12%.

- Discount Rate: Discount rate edges higher from 8.82% to 8.99%, implying slightly higher required return assumptions in the model.

- Revenue Growth: Revenue growth assumption shifts from 4.77% to 3.68%, reflecting more cautious expectations for top line expansion in NOK terms.

- Net Profit Margin: Net profit margin assumption increases from 7.72% to 10.51%, indicating a higher expected share of revenue converting into earnings in NOK.

- Future P/E: Future P/E multiple moves from 33.38x to 22.38x, a sizeable compression that lowers the valuation applied to projected earnings.

Key Takeaways

- High reliance on public sector and Nordic-European contracts exposes Omda to risks from budget constraints, regulatory changes, and potential cuts in IT spending.

- Sustained competitiveness demands heavy investment in R&D and cyber compliance, which could hinder margin growth amid intensifying international competition.

- Strong recurring revenue, robust customer retention, digital health expansion, and strategic cost and M&A initiatives are driving Omda's sustainable growth and margin improvement.

Catalysts

About Omda- Provides software solutions for the healthcare and emergency response sector in Norway, Sweden, Denmark, Finland, and internationally.

- Investors may be overestimating Omda's ability to maintain strong revenue growth rates, as much of its expansion relies on ongoing digitization in healthcare and public investment, which can be challenged by potential macroeconomic pressures or austerity measures-raising the risk of future revenue disappointments if public sector IT spending slows.

- The company's heavy dependence on publicly funded, Nordic and European contracts creates long-term exposure to regulatory tightening and cyclically constrained government budgets, suggesting margins and recurring revenues could be impacted by compliance cost increases or contract cutbacks.

- Although the company highlights strong, resilient recurring revenues and successful margin expansion, the required pace of R&D and platform upgrades to remain competitive (including integration of AI and data analytics) may keep operating expenses higher for longer, compressing net margins over time.

- Market valuations may not fully account for Omda's vulnerability to increasing data privacy regulation complexity and the continually evolving cyber-threat landscape, both of which carry the potential for higher costs, reputational risks, and lower profitability in the future.

- Despite positive outlooks regarding geographic and product expansion, Omda faces intensifying competition from large established international health tech firms and startups; this could erode its pricing power and market share, placing future revenue and earnings growth at risk if growth expectations are priced for near-perfection.

Omda Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Omda's revenue will grow by 3.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from -7.3% today to 10.5% in 3 years time.

- Analysts expect earnings to reach NOK 57.8 million (and earnings per share of NOK 1.6) by about June 2029, up from -NOK 35.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 23.0x on those 2029 earnings, up from -20.0x today. This future PE is lower than the current PE for the NO Healthcare Services industry at 54.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.99%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The aging global population and increasing demand for efficient, digitalized healthcare solutions are likely to drive sustained volume growth for Omda, as evidenced by their expanding footprint in specialized sectors (e.g., Emergency and fertility areas), supporting long-term revenue stability and growth.

- The company's highly diversified revenue base-over 750 active contracts across 26 countries, with >79% recurring revenues and ultra-low churn (<2%)-demonstrates strong customer retention, resilience, and predictability, countering risks of revenue decline.

- Ongoing digital transformation in healthcare, including adoption of patient-centric IT platforms and integration of AI-driven modules, positions Omda well to capture both organic growth (guided at 5–10% per year) and higher-margin value-added sales, enhancing future gross margins and earnings.

- Strategic cost efficiencies (such as COGS reduction toward 5%, selective FTE reductions, and productivity gains via AI-assisted development) have led to significant EBITDA margin improvement (from 12% to 20% YoY, aiming for 28%–32% in 2026), supporting robust future net margin and earnings expansion.

- Prudent, disciplined M&A activity-focused on acquiring complementary software and domain expertise within existing verticals-and the ability to leverage favorable market conditions for acquisitions (lower upfront cash, earnouts) suggest further scalable inorganic growth, diversification, and upside for both revenue and margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of NOK50.0 for Omda based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be NOK550.0 million, earnings will come to NOK57.8 million, and it would be trading on a PE ratio of 23.0x, assuming you use a discount rate of 9.0%.

- Given the current share price of NOK35.0, the analyst price target of NOK50.0 is 30.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Omda?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.