Last Update27 Aug 25Fair value Increased 4.09%

The upward revision in China Communications Services’ analyst price target is primarily driven by improved consensus revenue growth forecasts, now at 4.2% per annum, alongside a higher future P/E, resulting in a new fair value estimate of HK$4.98.

What's in the News

- The board has proposed amendments to the Articles of Association and Rules of Procedure, including abolishing the supervisory committee in favor of an audit committee, to align with updated PRC Company Law and Hong Kong listing regulations, subject to EGM approval.

- An extraordinary general meeting will be convened to seek shareholder approval for the proposed amendments, with details to be dispatched in a circular.

- A board meeting is scheduled for Aug 21, 2025, to approve interim results for the six months ended June 30, 2025.

- The AGM approved a final dividend of RMB 0.2187 per share (HKD 0.23831 per share pre-tax) for 2024, with payment arrangements specified for both local and Southbound Shareholders and an ex-dividend date of June 27, 2025.

Valuation Changes

Summary of Valuation Changes for China Communications Services

- The Consensus Analyst Price Target has risen slightly from HK$4.79 to HK$4.98.

- The Consensus Revenue Growth forecasts for China Communications Services has significantly risen from 3.4% per annum to 4.2% per annum.

- The Future P/E for China Communications Services has risen from 9.50x to 10.32x.

Key Takeaways

- Strategic emerging businesses, like digital infrastructure and smart cities, are driving growth, with strong contract increases boosting future revenue prospects.

- Overseas market successes and a focus on R&D and cost optimization enhance financial stability, promoting sustainable growth and profitability.

- Heavy reliance on emerging businesses amid declining domestic CapEx and geopolitical risks could pressure margins, liquidity, and overall financial stability.

Catalysts

About China Communications Services- Provides telecommunications support services worldwide.

- Strategic emerging businesses such as digital infrastructure, green and low-carbon solutions, and smart cities are becoming new growth drivers, with new contracts in these areas increasing by over 40% year-on-year. This is likely to positively impact future revenue growth.

- The company has shown a strong increase in gross profit margin by 0.2 percentage points and targets further improvements through high-value business expansion, cost control, and technological innovation. This is expected to enhance net margins and earnings.

- Overseas market expansion, particularly in APAC, the Middle East, Africa, and Latin America, achieved a 26% year-on-year revenue increase. Continued focus on these regions and synergistic projects with major Chinese enterprises are anticipated to further boost revenues.

- The increase in strategic emerging business contracts from domestic non-operator markets, with new contracts up by more than 45%, indicates robust growth potential. This growth is likely to have a substantial effect on revenue and profitability.

- The company's commitment to strengthening R&D, optimizing cost structure, and maintaining solid financial health, with improved cash flow and stable liability ratios, positions it well for sustainable long-term growth, impacting overall earnings positively.

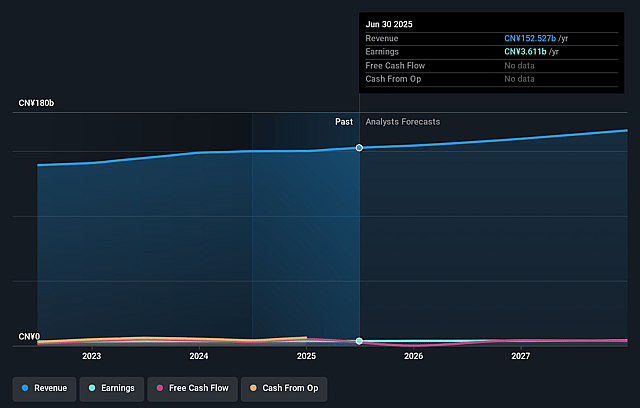

China Communications Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming China Communications Services's revenue will grow by 4.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.4% today to 2.5% in 3 years time.

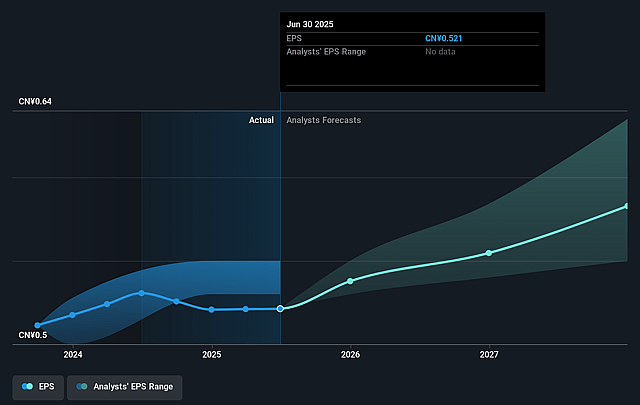

- Analysts expect earnings to reach CN¥4.3 billion (and earnings per share of CN¥0.62) by about August 2028, up from CN¥3.6 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CN¥3.8 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.5x on those 2028 earnings, up from 8.3x today. This future PE is lower than the current PE for the HK Construction industry at 11.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.63%, as per the Simply Wall St company report.

China Communications Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Decline in CapEx from domestic operators could lead to lower revenue growth from the domestic operator market, impacting overall revenue sustainability.

- High reliance on strategic emerging businesses for growth could be risky if expected high growth rates in these sectors do not materialize, affecting future revenue and profitability.

- Increased accounts receivable and lack of improvement in cash flow may lead to liquidity issues, potentially impacting the ability to invest in new projects or pay dividends, thereby affecting net margins and earnings.

- Dependence on overseas markets for robust growth brings exposure to geopolitical risks and regulatory challenges, potentially impacting overseas revenue streams and profit margins.

- Intense market competition and the need for continuous investment in technological advancements and R&D to maintain competitiveness, which could increase costs and pressure profit margins if returns on these investments are not sufficient.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of HK$4.985 for China Communications Services based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of HK$5.51, and the most bearish reporting a price target of just HK$4.4.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥172.7 billion, earnings will come to CN¥4.3 billion, and it would be trading on a PE ratio of 9.5x, assuming you use a discount rate of 8.6%.

- Given the current share price of HK$4.69, the analyst price target of HK$4.98 is 5.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.