Last Update 25 Apr 26

Fair value Decreased 3.07%EMIRATESNBD: Dividend Vote And Upcoming Meetings Will Support Future Upside Potential

Analysts have slightly reduced their price target for Emirates NBD Bank PJSC from AED 35.57 to AED 34.48, reflecting updated assumptions around revenue growth, profit margins, and a lower future P/E estimate.

What's in the News

- A board meeting is scheduled for Apr 22, 2026 at 11:00 UTC to review and approve the previous board meeting minutes, the Emirates NBD Group consolidated financial statements for the quarter ended Mar 31, 2026 in English and Arabic, and other normal activities (Key Developments).

- A special or extraordinary shareholders meeting is set for Feb 17, 2026 at 11:00 UTC at the Meydan Hotel in Dubai to vote on the board report and audited financial statements for the year ended Dec 31, 2025, as well as related governance items (Key Developments).

- Shareholders are scheduled to vote on a proposed cash dividend of AED 1.00 per ordinary share, totaling AED 6,316,598,253 for the year ended Dec 31, 2025, with an intended record date at the close of trading on Feb 27, 2026, subject to approval at the extraordinary meeting (Key Developments).

Valuation Changes

- Fair Value: Trimmed from AED 35.57 to AED 34.48, a modest reduction in the central value estimate.

- Discount Rate: Kept broadly stable, moving slightly from 20.07% to 20.07% on a rounded basis.

- Revenue Growth: Assumed annual growth rate eased from about 9.78% to 9.12%, indicating slightly more cautious expectations for revenue.

- Net Profit Margin: Margin assumption edged up from roughly 45.34% to 46.90%, indicating a stronger profitability profile in the model.

- Future P/E: Forward P/E multiple in the model moved from about 13.53x to 12.60x, indicating a lower valuation multiple applied to future earnings.

Key Takeaways

- Rising demand for banking services and geographic diversification are driving sustained revenue growth and reducing dependence on the UAE market.

- Digital innovation, product expansion, and a dominant retail position are strengthening efficiency, fee income, and long-term profitability.

- Profitability faces pressure from narrowing margins, elevated costs, asset quality concerns, and dependence on favorable market conditions, challenging future earnings growth and capital strength.

Catalysts

About Emirates NBD Bank PJSC- Provides corporate, institutional, retail, treasury, and Islamic banking services.

- Ongoing economic diversification in the UAE and broader GCC region, combined with strong GDP growth forecasts, is driving robust demand for both corporate and consumer banking services; this has enabled Emirates NBD to revise its loan growth guidance upwards to low double digits, pointing to sustained revenue and earnings expansion.

- Accelerated adoption of digital banking and investments in tech innovation are materially improving operating efficiency, contributing to a declining cost-to-income ratio (now below 31%), which supports long-term margin expansion and profitability.

- Significant loan growth momentum in key international markets (notably Saudi Arabia, Egypt, India, Turkey, and Singapore, with double-digit increases), alongside plans for further organic and inorganic expansion, is diversifying earnings streams and reducing reliance on the UAE market, strengthening top-line growth and risk-adjusted returns.

- Expansion and innovation in higher-margin businesses such as wealth management, private banking, and structured products (with strong gains in fee and commission income-up 18% YoY) are increasing non-interest income, which helps offset NIM pressure and boosts net profit growth.

- Continued reputation as a dominant retail bank (e.g., 35% UAE credit card spend market share, rapid card product growth) and a strong, low-cost CASA deposit base (60% CASA ratio) position Emirates NBD to benefit from further international trade flows and capital inflows into Dubai, supporting funding cost advantages and facilitating higher net interest margins.

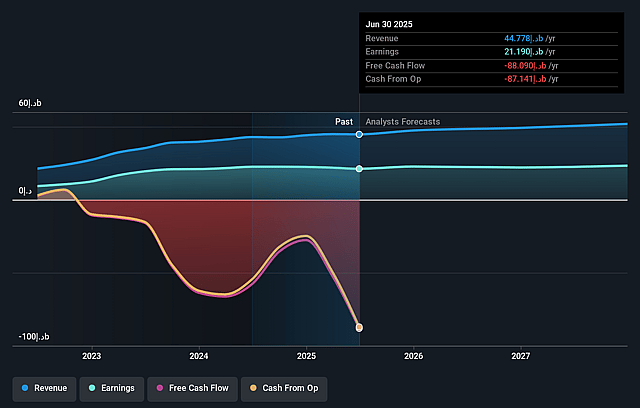

Emirates NBD Bank PJSC Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Emirates NBD Bank PJSC's revenue will grow by 9.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 48.2% today to 46.9% in 3 years time.

- Analysts expect earnings to reach AED 29.9 billion (and earnings per share of AED 4.61) by about April 2029, up from AED 23.7 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as AED33.7 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 12.6x on those 2029 earnings, up from 8.1x today. This future PE is greater than the current PE for the AE Banks industry at 8.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 20.07%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Sustained pressure on net interest margins due to ongoing and anticipated policy rate cuts in both the UAE and Turkey, combined with increasing competition and high market liquidity, could compress profitability and earnings over time.

- Asset quality risks in Turkey remain elevated, as DenizBank continues to face high cost of risk (guidance of 250 basis points for 2025) and macroeconomic uncertainty; normalization may still result in persistently higher provisioning costs that could weigh on group net profits.

- High operating expenses due to significant, ongoing investments in international expansion, digital transformation (including GenAI), and workforce growth could erode net margins if revenue growth slows or efficiency improvements lag.

- Continued reduction in sovereign loan exposure and corresponding increase in risk-weighted assets (RWA density) may strain capital adequacy and require enhanced capital generation to maintain current CET1 ratios, with potential downstream impact on lending growth and return on equity.

- Dependence on strong economic and property market conditions in the UAE and key international markets makes growth assumptions vulnerable to cyclical downturns, while lack of material new government borrowing and a shift to pre-funded real estate development reduce opportunities for high-volume, low-risk loan growth-potentially impacting future revenue trajectory.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of AED34.48 for Emirates NBD Bank PJSC based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of AED37.0, and the most bearish reporting a price target of just AED27.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be AED63.8 billion, earnings will come to AED29.9 billion, and it would be trading on a PE ratio of 12.6x, assuming you use a discount rate of 20.1%.

- Given the current share price of AED30.2, the analyst price target of AED34.48 is 12.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Emirates NBD Bank PJSC?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.