Catalysts

About Bridgestone

Bridgestone is a global manufacturer of tires and related solutions for passenger vehicles, trucks, buses, specialty applications and retail customers.

What are the underlying business or industry changes driving this perspective?

- Expansion of U.S. tariffs on imported products is now expected to have a JPY 25b direct impact on adjusted operating profit for fiscal 2025. If trade frictions or sourcing shifts continue to build, future revenue growth and margins in North America could face sustained pressure.

- A clear slowdown in the U.S. economy is already linked to weaker truck and bus original equipment demand and softer consumer retail traffic. If freight volumes and consumer confidence remain soft, this could cap volume growth and weigh on group revenue and earnings from 2026 onward.

- Truck and bus tire demand in North America is currently described as down about 23% year-on-year at the industry level. If this lower baseline persists while Bridgestone defends share with higher fixed costs after prior rebuilding, unit economics in this core segment could compress net margins.

- Latin American and diversified product operations are still referred to as challenging with business rebuilding ongoing. If these portfolios struggle to reach management’s profitability ambitions, they may continue to drag on consolidated adjusted operating margin and ROE despite stronger regions.

- The recent cyber incident in North America caused production stoppages, backlogs and lost sales. If similar operational or IT risks recur as the company digitises more of its B2B solutions and retail network, this could introduce recurring disruption risk to revenue and short term earnings.

Assumptions

This narrative explores a more pessimistic perspective on Bridgestone compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

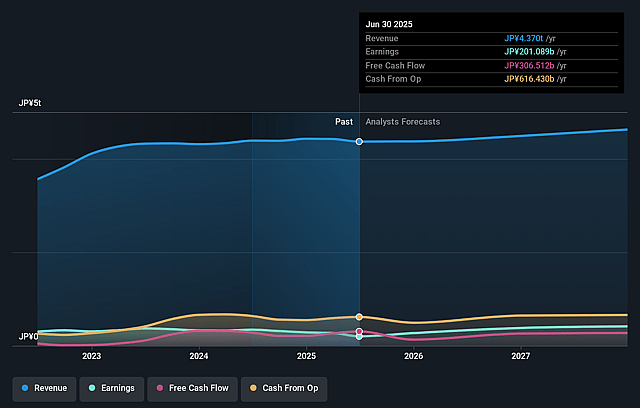

- The bearish analysts are assuming Bridgestone's revenue will grow by 3.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 5.4% today to 9.2% in 3 years time.

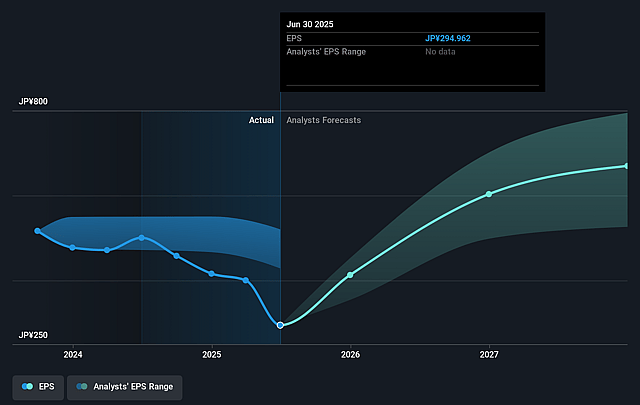

- The bearish analysts expect earnings to reach ¥444.6 billion (and earnings per share of ¥226.16) by about February 2029, up from ¥235.7 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ¥561.7 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 8.4x on those 2029 earnings, down from 18.9x today. This future PE is lower than the current PE for the JP Auto Components industry at 10.6x.

- The bearish analysts expect the number of shares outstanding to decline by 4.68% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.45%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Management repeatedly talks about "growth with quality" built on premium tires such as high rim diameter products in Europe, Japan and other key regions, and these premium mixes are already linked to higher adjusted operating margins in the premium tire business and in Europe. This could support revenue and net margin resilience even if some markets stay soft.

- Commercial B2B solutions and the broader Solutions business are described as growth markets, with adjusted operating profit in commercial B2B solutions up 144% year on year and the Solutions segment profit up 155% year on year with margin expansion of 2.7 percentage points. If this higher margin, service driven revenue continues to scale it could support earnings even if some tire volumes come under pressure.

- Several regions that were previously under rebuilding, such as North America, Europe, Latin America and Asia Pacific, India and China, are already reporting year on year profit growth or solid profit levels. If these long running restructuring and cost reduction efforts keep improving business quality, the group adjusted operating margin around 11% and ROIC around 9% could be sustained or improved, which would be supportive for earnings and return on equity.

- Global cost reduction and lean management programs have already produced approximately ¥52b of cumulative savings and free cash flow of ¥243.7b alongside ongoing growth investments and share buybacks that are about 86% complete. If Bridgestone keeps converting profits into cash at this pace, balance sheet strength, buybacks and dividends such as the ¥230 per share payout could support shareholder returns even if revenue growth moderates.

- Despite tariff headwinds, U.S. macro slowdown and a cyber incident, adjusted operating profit guidance for fiscal 2025 of ¥490b still represents year on year growth with an adjusted operating margin above 11%, while premium tire margins in North America are about 15% and specialty tires maintain margins above 20%. If these high margin franchises continue to perform, group earnings and cash generation could remain sturdier than a bearish share price view implies for revenue, net margins and overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Bridgestone is ¥2733.04, which represents up to two standard deviations below the consensus price target of ¥3745.77. This valuation is based on what can be assumed as the expectations of Bridgestone's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥4200.0, and the most bearish reporting a price target of just ¥2150.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be ¥4840.6 billion, earnings will come to ¥444.6 billion, and it would be trading on a PE ratio of 8.4x, assuming you use a discount rate of 6.4%.

- Given the current share price of ¥3740.0, the analyst price target of ¥2733.04 is 36.8% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Bridgestone?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.