Last Update 25 Jun 26

BRD: Dividend Will Sustain An Overvalued P/E Despite Flat Earnings Outlook

Analysts kept their price target for BRD - Groupe Société Générale at RON 25.08, reflecting essentially stable assumptions around fair value, discount rate, revenue growth, profit margin and future P/E in their latest update.

What's in the News for BRD - Groupe Société Générale

- No recent news items or key developments are currently available from the specified sources for BRD - Groupe Société Générale.

- Analysts and investors may need to rely more heavily on existing financial reports, company filings and historical disclosures when assessing BRD and Groupe Société Générale at this time.

- The absence of recent source-cited headlines can make it useful to monitor upcoming earnings releases, regulatory announcements and corporate communications for fresh information.

Valuation Changes for BRD - Groupe Société Générale

- Fair Value: RON 25.08 has been maintained, indicating no change in the central valuation level used for BRD - Groupe Société Générale.

- Discount Rate: Adjusted slightly to 13.93% from 13.92%, reflecting a very small technical update to the rate applied in the valuation model.

- Revenue Growth: Held essentially steady at 8.01%, suggesting the same growth assumption for BRD's RON denominated revenue as in the prior model.

- Net Profit Margin: Remains at 38.53%, with only a marginal rounding difference, so profitability assumptions for BRD are effectively unchanged.

- Future P/E: Updated very slightly to 12.84x from 12.84x, implying no meaningful shift in the valuation multiple applied to BRD's expected earnings.

Key Takeaways

- Rapid digital banking adoption and branch optimization are projected to increase efficiency, lower costs, and support stronger profit margins and returns.

- Strategic lending growth and investments in green financing position the company to benefit from macroeconomic trends and drive sustained topline and earnings expansion.

- Rising regulatory costs, reliance on the domestic market, and increasing fintech competition threaten profitability and shareholder returns amidst uncertain dividend outlook and required digital investments.

Catalysts

About BRD - Groupe Société Générale- Provides a range of banking and financial services to corporates and individuals in Romania.

- Rapid expansion in digital banking usage, with a 20% annual increase in mobile app users and nearly all corporate and retail transactions processed through digital channels, is expected to boost operational efficiency, lower the cost-to-income ratio, and drive net margin improvement over the long term.

- Sustained growth in lending activity, evidenced by 19% year-on-year growth in the loan portfolio and significant market share gains in both SME and retail loans, positions the company to benefit from rising urbanization and increasing middle-class income in Romania, supporting future revenue and earnings growth.

- Strategic investments in green financing and sustainable products, having already surpassed 2025 targets and entered new partnerships (e.g., with IFC and EIF), are likely to expand the corporate loan portfolio and increase fee and commission income, supporting topline growth and future profitability.

- Ongoing optimization of the physical branch network, with a reduction of 35 branches year-on-year and expansion of cashless/self-service points, is expected to lower operational expenses, improve overall efficiency, and support higher returns on equity.

- A resilient balance sheet, strong liquidity coverage ratio (>220%), low NPL ratio (2.1%), and high coverage levels provide a solid foundation to weather macroeconomic fluctuations and leverage further lending and business expansion for future net income growth.

BRD - Groupe Société Générale Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming BRD - Groupe Société Générale's revenue will grow by 8.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 37.8% today to 38.5% in 3 years time.

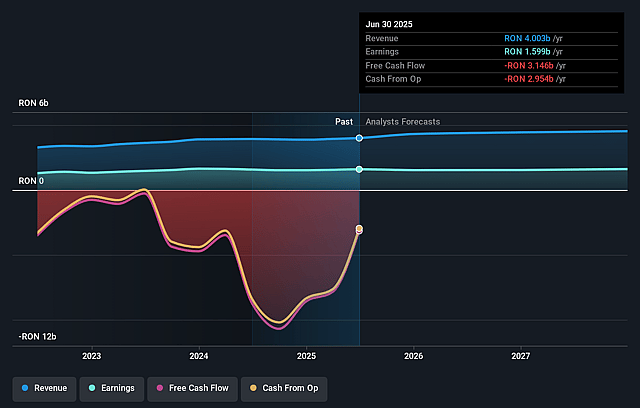

- Analysts expect earnings to reach RON 2.0 billion (and earnings per share of RON 2.9) by about June 2029, up from RON 1.6 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as RON2.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 12.9x on those 2029 earnings, down from 14.4x today. This future PE is greater than the current PE for the RO Banks industry at 8.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.93%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The new 2% tax on gross turnover, which significantly increased operating expenses in 2024, directly pressures net margins and future profitability-especially if further regulatory or fiscal burdens emerge in the Romanian market.

- The company's high reliance on the Romanian market exposes it to local economic slowing, as highlighted by decreasing GDP growth (from over 2% in 2023 to approximately 1% in 2024), increasing earnings volatility and sensitivity to domestic economic shocks.

- While digital adoption is growing, increasing competition from fintechs and digital-first banks may compress BRD's fee and commission revenues over time, particularly if the pace of innovation or customer engagement slows compared to more agile competitors.

- Extensive investments in digital transformation and IT are required to maintain competitiveness, and if BRD's execution slows or fails to keep up with industry standards, cost-to-income ratios may rise and net margins could suffer.

- The absence of a confirmed dividend announcement and ongoing negotiation with the National Bank of Romania on payout approvals introduce uncertainty around shareholder returns, which could impact investor sentiment and affect the share price.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of RON25.08 for BRD - Groupe Société Générale based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of RON30.0, and the most bearish reporting a price target of just RON20.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be RON5.2 billion, earnings will come to RON2.0 billion, and it would be trading on a PE ratio of 12.9x, assuming you use a discount rate of 13.9%.

- Given the current share price of RON32.3, the analyst price target of RON25.08 is 28.8% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on BRD - Groupe Société Générale?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.