Last Update 23 Jun 26

EPR: Dividend Visibility And Nationwide Store Expansion Will Support A Stronger Future

Analysts have maintained their Europris price target at NOK 102, with only minor adjustments to the discount rate, revenue growth, profit margin, and future P/E assumptions supporting this stable outlook.

What’s in the News for Europris

- Europris has opened a new store in Alstad, Bodø in Nordland, the group’s first store opening in 2026, bringing its Norwegian network to 290 stores, including 269 directly operated and 21 franchised locations. (Key Developments)

- Europris now reports a physical presence in all Norwegian counties through its 290 store network. (Key Developments)

- At the AGM on 29 April 2026, Europris ASA approved a dividend of NOK 3.75 per share, with entitlement based on shareholders registered in the ESO on 4 May 2026 and the shares trading ex dividend from 30 April 2026. (Key Developments)

- The dividend to Europris shareholders is expected to be paid on or about 11 May 2026. (Key Developments)

Valuation Changes

- Fair Value: NOK 102.0, unchanged from the previous NOK 102 estimate for Europris.

- Discount Rate: risen slightly from 9.14% to 9.21%.

- Revenue Growth: edged slightly lower from 4.91% to 4.89%.

- Net Profit Margin: broadly stable at 9.07%.

- Future P/E: increased slightly from 13.54x to 13.57x.

Key Takeaways

- Modernization and integration efforts at ÖoB are projected to enhance profitability and sales through clearance sales, category upgrades, and increased margin efficiency.

- Expansion in Norway and IT platform upgrades in Norway and Sweden are expected to boost revenue and net margins by improving market reach and operational efficiency.

- Volatile currency markets, integration challenges, and increased competition are limiting Europris' profitability and market share growth despite strategic efforts.

Catalysts

About Europris- Operates as a discount variety retailer in Norway.

- The integration and modernization efforts at ÖoB, including clearance sales and category upgrades, are expected to enhance sales and profitability as the turnaround process gains traction. This is projected to impact future revenue and EBIT positively by increasing sales volume and improving margin efficiency.

- The expansion strategy in Norway, exemplified by three new store openings and the upcoming store in Larvik, aims to increase Europris' market reach and footfall, potentially driving revenue growth as more consumers access the brand through new locations.

- The successful implementation of new IT platforms, including ERP systems both in Norway and Sweden, is expected to improve operational efficiency and customer experience, potentially boosting net margins by reducing costs and enhancing sales processes across the group.

- Investment in the home & interior category, which is a high-margin area and drives seasonal sales, along with leveraging social media trends like TikTok, is anticipated to increase sales and improve gross margins through enhanced product offerings and marketing strategies.

- Harmonizing systems and supply chains through IT improvements and joint sourcing strategies, especially between Europris and ÖoB, is expected to optimize operational efficiency and reduce costs, enhancing net margins and improving earnings long-term as the integration continues.

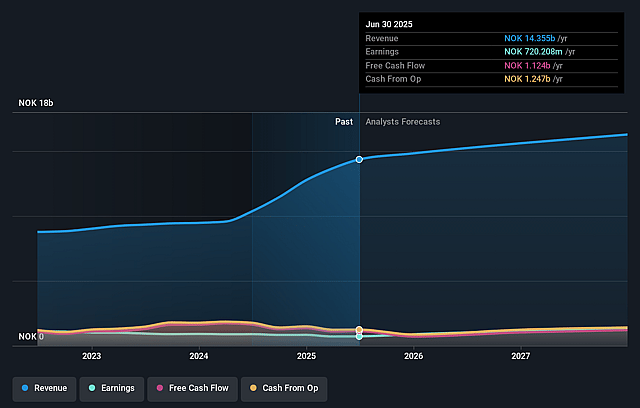

Europris Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Europris's revenue will grow by 4.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.9% today to 9.1% in 3 years time.

- Analysts expect earnings to reach NOK 1.6 billion (and earnings per share of NOK 8.86) by about June 2029, up from NOK 891.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting NOK2.0 billion in earnings, and the most bearish expecting NOK1.4 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.6x on those 2029 earnings, down from 16.2x today. This future PE is lower than the current PE for the GB Multiline Retail industry at 16.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.21%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Volatile currency markets have significantly impacted Europris' financial performance, leading to unrealized losses on currency hedging contracts, which negatively affect net margins and reported EBIT.

- The ÖoB acquisition in Sweden has yet to show improved sales and customer traffic, with current efforts primarily directed at inventory clearance and store remodeling, which could delay potential revenue recovery and profit growth.

- High net working capital and negative cash flow from operations, exacerbated by planned inventory buildup and integration costs, may pressure liquidity and raise financial risk if sales do not meet expectations.

- Continued integration and upgrade expenses in Sweden, such as costs associated with ERP system implementation, weigh on operating expenses and reduce earnings in the short term until benefits are realized.

- Increased competition, particularly on seasonal and nonfood products, and a cautious approach to changing consumer behavior could limit Europris' ability to capture market share and achieve desired revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of NOK102.0 for Europris based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be NOK17.6 billion, earnings will come to NOK1.6 billion, and it would be trading on a PE ratio of 13.6x, assuming you use a discount rate of 9.2%.

- Given the current share price of NOK88.4, the analyst price target of NOK102.0 is 13.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Europris?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.