Last Update 26 Jun 26

Fair value Decreased 3.30%DIM: Bioprocessing Recovery Signals Will Support Constructive Outlook Despite Higher Sector Risk

The analyst price target for Sartorius Stedim Biotech has been trimmed by €7.93 to €232.21, as analysts factor in slightly higher risk, a modestly lower profit margin outlook, and updated sector views that still identify early signs of recovery in bioprocessing.

Analyst Commentary

Recent commentary on Sartorius Stedim Biotech reflects a mix of optimism about early recovery signals in bioprocessing and caution about sector risk, which feeds directly into how analysts are thinking about valuation, execution, and growth over the medium term.

Bullish Takeaways

- Bullish analysts point to what they describe as "green shoots of recovery" in bioprocessing and quality assurance, which they see as supportive for Sartorius Stedim Biotech's growth profile as end market demand stabilises.

- Some research highlights that life science tools stocks, including Sartorius Stedim Biotech, are priced cautiously. Those analysts view this as leaving room for upside if execution on orders, margins, and capacity utilisation tracks expectations.

- Where target prices have been adjusted, bullish analysts frame this as aligning with risk adjusted return expectations rather than a fundamental shift in the long term role of Sartorius Stedim Biotech in the bioprocessing supply chain.

- The company is cited alongside other preferred healthcare tools stocks, which signals that certain analysts still see it as a core holding within the sector despite the more conservative targets.

Bearish Takeaways

- Bearish analysts focus on the sector backdrop, noting that broader market expectations for life science tools remain cautious, with capital still flowing more readily to managed care and therapeutics stocks.

- The recent reduction in the price target for Sartorius Stedim Biotech is tied to higher perceived risk and margin pressure. This could weigh on how investors value the stock if profitability trends do not improve.

- There is concern that the tools sector is currently priced for disappointment, which means any execution slip on orders, inventory normalisation, or cost control at Sartorius Stedim Biotech could have an outsized impact on the share price.

- Adjustments to targets to reflect risk adjusted returns also signal that some analysts see a less favourable balance between potential upside and execution or sector headwinds than before.

What’s in the News for Sartorius Stedim Biotech

- Sartorius Stedim Biotech confirmed earnings guidance for the full year 2026, expecting sales revenue growth in constant currencies of around 5% to 9%.

- The 2026 guidance provides investors with a reference range for potential top line development in constant currency terms, which some may use when assessing how current analyst price targets compare with company expectations. Source: Key Developments

Valuation Changes for Sartorius Stedim Biotech

- Fair Value: trimmed from €240.14 to €232.21, a reduction of about 3.3% that reflects slightly higher risk and margin assumptions.

- Discount Rate: revised from 7.51% to 7.68%, a modest increase that raises the required return used to value Sartorius Stedim Biotech.

- Revenue Growth: adjusted from 9.93% to 10.18%, a small uplift in the long term revenue growth assumption in € terms.

- Net Profit Margin: moved from 16.05% to 15.02%, indicating a slightly lower expected earnings margin in € terms.

- Future P/E: brought down from 46.06x to 43.05x, implying a lower valuation multiple applied to Sartorius Stedim Biotech’s projected earnings.

Key Takeaways

- Strong demand for single-use consumables and compliance expertise drive high-margin growth, supporting both revenue expansion and pricing power for sustained profitability.

- Leadership in innovative bioprocess technologies and rising customer equipment utilization position the company for future sales acceleration and reduced business risk.

- Ongoing weak equipment demand, geopolitical risks, inventory challenges, and slow China recovery threaten revenue growth and margins, especially in the underperforming lab products segment.

Catalysts

About Sartorius Stedim Biotech- Engages in the production and sale of instruments and consumables for the biopharmaceutical industry worldwide.

- Strong, sustained double-digit growth in recurring single-use consumables is being driven by higher bioprocess utilization and robust end-market demand, reflecting increasing adoption of biologics, cell/gene therapies, and the need for flexible production platforms-which supports both revenue growth and margin expansion due to the high-margin nature of these products.

- Continued global momentum in regulation-driven requirements for manufacturing quality and safety benefits Sartorius Stedim Biotech as a trusted partner with strong compliance track records, increasing its competitive moat and supporting premium pricing-leading to sustained improvements in net margins over time.

- Recent product launches-such as automated/intensified bioprocess modules and next-gen lab instruments-position the company ahead of the ongoing industry shift toward more innovative manufacturing technologies and personalized medicine, setting up for future revenue acceleration as new drug modalities scale.

- The growing installed base and high utilization of Sartorius' equipment platform signal a likely inflection point in new equipment investment cycles as customers' capacity becomes fully utilized, which is expected to translate into a recovery in equipment sales and incremental top line growth.

- Consistent improvement in order intake and a book-to-bill ratio above 1 on a rolling 12-month basis indicate strengthening forward demand visibility across regions, reducing revenue and earnings uncertainty, and supporting management's confidence in meeting or exceeding current financial guidance.

Sartorius Stedim Biotech Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Sartorius Stedim Biotech's revenue will grow by 10.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.0% today to 15.0% in 3 years time.

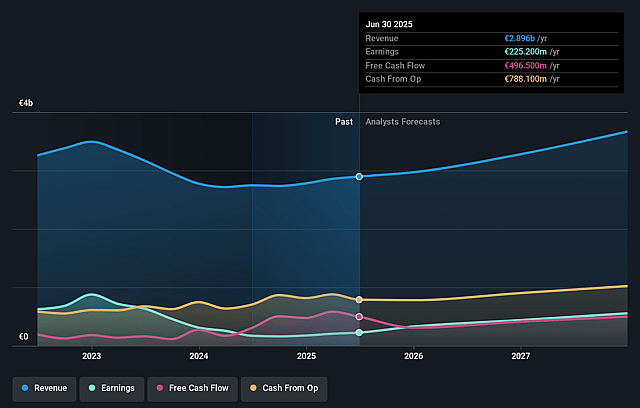

- Analysts expect earnings to reach €599.3 million (and earnings per share of €6.41) by about June 2029, up from €268.1 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as €665.3 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 43.4x on those 2029 earnings, down from 64.2x today. This future PE is greater than the current PE for the GB Life Sciences industry at 28.7x.

- Analysts expect the number of shares outstanding to decline by 2.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.68%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Lingering weakness and uncertainty in equipment sales, with capital spending by customers remaining soft and continued reluctance to invest in large CapEx projects, could cap topline revenue growth and increase dependence on consumables for margin expansion.

- Tariff increases and ongoing geopolitical risks (notably for US business) are anticipated to intensify in the second half of the year; these could inflate the top line but potentially dilute margins (by 30–40 bps), and in a prolonged scenario, raise costs and disrupt operations, negatively impacting net margins and earnings.

- Persistent inventory write-downs-still above pre-pandemic levels-are continuing to dampen profitability, with only a gradual normalization projected into 2026, presenting an ongoing drag on net margin and earnings quality.

- Slow recovery and heightened local competition in key markets such as China, where government procurement policies increasingly favor locally produced lab instruments, may limit regional revenue growth and profitability, particularly in the LPS division.

- The LPS (Lab Products & Services) segment remains underperforming with CapEx-driven business in structural decline and ambitious guidance for a second–half acceleration reliant on new product launches and market stabilization, raising the risk of missed revenue targets and ongoing margin pressure if the recovery does not materialize as expected.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €232.21 for Sartorius Stedim Biotech based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €262.0, and the most bearish reporting a price target of just €210.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €4.0 billion, earnings will come to €599.3 million, and it would be trading on a PE ratio of 43.4x, assuming you use a discount rate of 7.7%.

- Given the current share price of €177.0, the analyst price target of €232.21 is 23.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Sartorius Stedim Biotech?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.