Key Takeaways

- Increased Gulfstream aircraft deliveries and G700 introduction signal positive revenue and margin growth in the Aerospace segment.

- Strong order backlog and investments in Navy programs indicate sustained future growth across Aerospace, Combat Systems, and Marine segments.

- Challenges in aerospace delivery schedules, supply chain issues, a potential slowdown in defense segment orders, increased capital expenditures, and a higher effective tax rate pose significant risks.

Catalysts

What are the underlying business or industry changes driving this perspective?

- Strong demand for Gulfstream aircraft with expectations of increased deliveries in 2024, which should positively impact revenue growth and operating margin in the Aerospace segment.

- Robust order activity and backlog across the company, particularly in the Aerospace and Combat Systems segments, indicating potential for sustained future revenue growth.

- Investments in shipyards to support Navy submarine and shipbuilding programs, indicating potential future revenue growth in the Marine segment from government contracts.

- The introduction and expected delivery of approximately 50 G700 aircraft in 2024, anticipated to be accretive to margins and significantly contribute to revenue growth in the Aerospace segment.

- Continual year-over-year improvement in operating earnings and net earnings, suggesting effective cost management and operational efficiency that could further enhance net margins going forward.

Assumptions

How have these above catalysts been quantified?

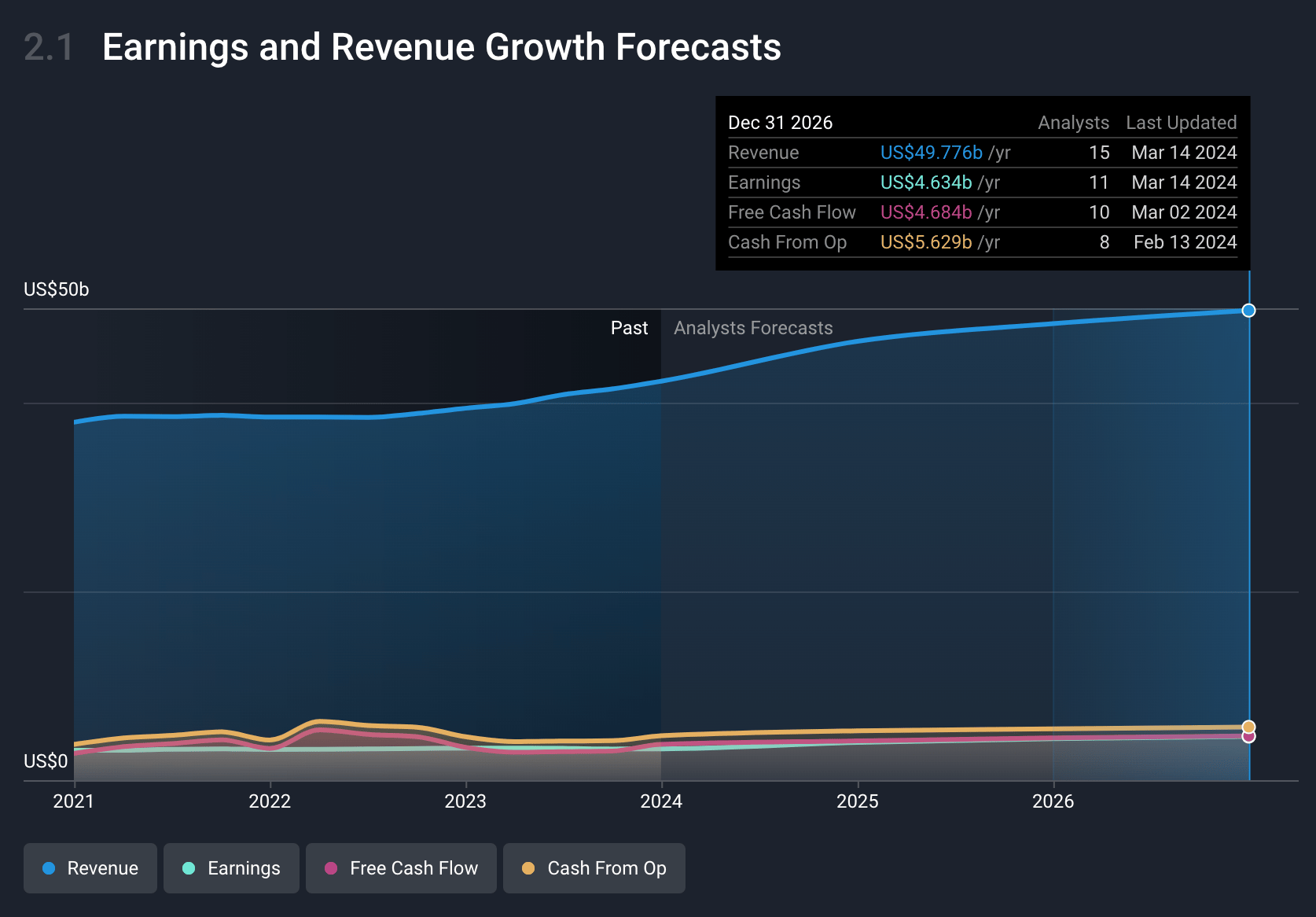

- Analysts are assuming General Dynamics's revenue will grow by 5.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.8% today to 9.3% in 3 years time.

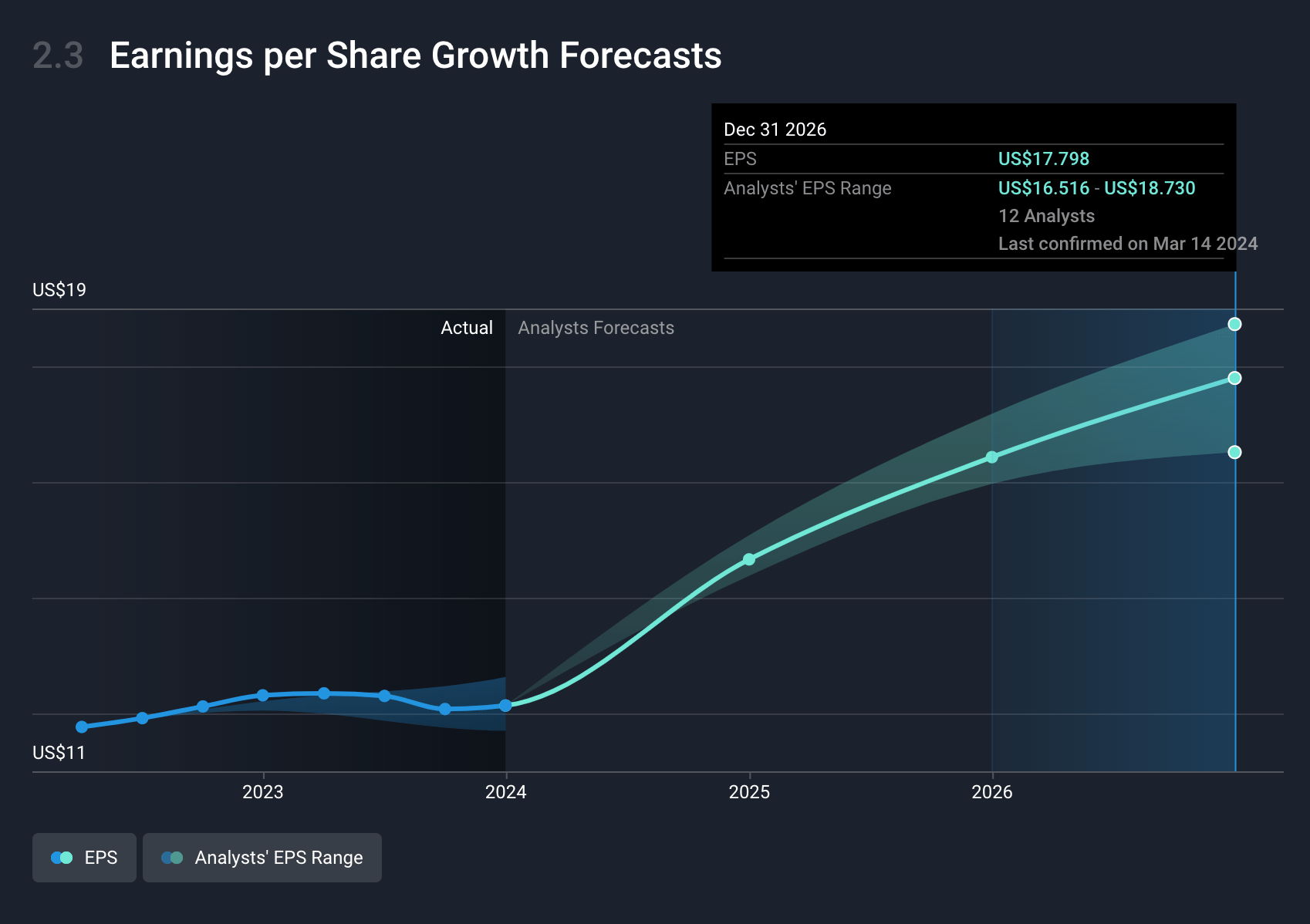

- Analysts expect earnings to reach $4.6 billion (and earnings per share of $17.8) by about March 2027, up from $3.3 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.3x on those 2027 earnings, down from 22.9x today.

- To value all of this in today’s dollars, we will use a discount rate of 5.97%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Delays in G700 certification have directly impacted revenue and earnings, with the failure to deliver 15 aircraft resulting in a significant loss of revenue and near $250 million in earnings, indicating a challenge in meeting aerospace delivery schedules.

- Supply chain issues across segments, notably in Aerospace, affected production ramp-up plans, demonstrating operational risk factors that could further disrupt future revenue and margin performance.

- The Defense segment's lower book-to-bill ratio in the fourth quarter (0.7x) compared to the year overall (1:1) might reflect a potential slowdown in order activity, posing a risk to sustained revenue growth within this segment.

- Higher expected capital expenditures for the upcoming year in support of Navy submarine and shipbuilding could strain cash flows if unanticipated expenditures arise, highlighting a financial risk in maintaining or improving net margins.

- An anticipated increase in effective tax rate to around 17.5% due to higher taxes on foreign earnings represents a risk to net earnings growth, potentially offsetting operational gains made in other areas of the business.

valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $290.01 for General Dynamics based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with this, you'd need to believe that by 2027, revenues will be $49.8 billion, earnings will come to $4.6 billion, and it would be trading on a PE ratio of 18.3x, assuming you use a discount rate of 6.0%.

- Given the current share price of $277.6, the analyst's price target of $290.01 is 4.3% higher. The relatively low difference between the current share price and the analyst target indicates that they believe the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company’s future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.’s analysis may not factor in the latest price-sensitive company announcements or qualitative material.