Last Update 25 Jun 26

Fair value Increased 2.05%CLAS B: Future Returns Will Depend On Dividend Payouts And Steady Execution

The analyst price target for Clas Ohlson has been adjusted from SEK 406.67 to SEK 415.00, with analysts citing updated assumptions around revenue growth, profit margin, and the future P/E multiple as key drivers of the revised fair value estimate.

What’s in the News for Clas Ohlson

- Clas Ohlson announced that the Board of Directors proposed an ordinary dividend of SEK 9.25 per share (source: Key Developments).

- Clas Ohlson also announced that the Board proposed an extraordinary dividend of SEK 4.75 per share (source: Key Developments).

- Together, the proposed ordinary and extraordinary dividends would bring the total proposed dividend to SEK 14.00 per share (source: Key Developments).

Valuation Changes for Clas Ohlson

- Fair Value: Adjusted from SEK 406.67 to SEK 415.00, representing a modest upward revision in the analyst fair value estimate.

- Discount Rate: Reduced from 6.41% to 6.38%, indicating a small change in the rate used to discount future cash flows.

- Revenue Growth: Increased from 6.25% to 6.69%, reflecting a slight rise in the assumed long term revenue growth rate for Clas Ohlson.

- Net Profit Margin: Raised from 9.87% to 10.00%, indicating a marginally higher margin assumption in the updated model.

- Future P/E: Lowered from 21.18x to 20.72x, indicating a slightly reduced valuation multiple applied to future earnings.

Key Takeaways

- Transitioning to a multi-niche retailer differentiates Clas Ohlson in various market segments, driving sales growth and improving margins.

- Emphasis on profitable online sales and store expansions supports sustained growth, with strategic partnerships enhancing revenue through a diversified product range.

- Currency fluctuations, rising sea freight costs, and higher operating expenses pose risks to gross margins and revenue growth for Clas Ohlson.

Catalysts

About Clas Ohlson- A retail company, sells hardware, electrical, multimedia, home, and leisure products in Sweden, Norway, Finland, and internationally.

- Clas Ohlson's shift from a generalist retailer to a multi-niche player allows them to differentiate within multiple market segments, which should drive continued sales growth and improve operating margins.

- The focus on a profitable online business, with online sales growth at 22%, aims to continually increase the share of online sales, positively impacting revenue and potentially improving net margins.

- The store expansion strategy, with a goal of adding approximately 10 new stores annually, combined with improvements in existing stores, is expected to sustain organic growth and enhance revenue.

- Efforts to establish a cost-competitive operating model, notably through optimized sourcing and inventory management, are likely to contribute to higher net margins and overall earnings.

- Strategic partnerships and product range expansions, such as the introduction of well-known brands like Husqvarna, should attract more customers and increase revenue through a diversified assortment.

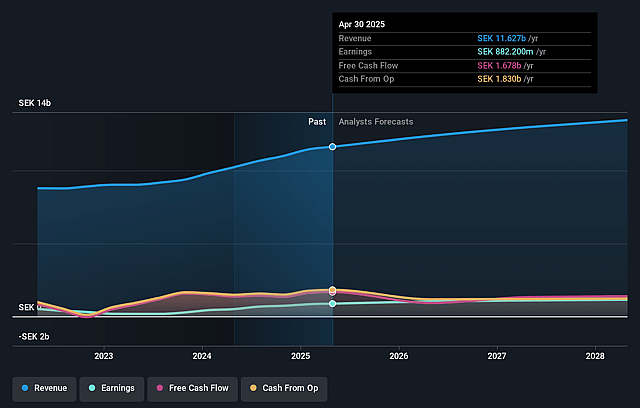

Clas Ohlson Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Clas Ohlson's revenue will grow by 6.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.3% today to 10.0% in 3 years time.

- Analysts expect earnings to reach SEK 1.5 billion (and earnings per share of SEK 23.81) by about June 2029, up from SEK 1.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 21.0x on those 2029 earnings, down from 22.4x today. This future PE is lower than the current PE for the GB Specialty Retail industry at 21.2x.

- Analysts expect the number of shares outstanding to grow by 0.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.38%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The effects of currency fluctuations, specifically a weak Norwegian kroner and a volatile U.S. dollar, present significant risks that can negatively impact gross margins and net profit due to unforeseen fluctuations in costs related to purchasing and logistics.

- The rising sea freight costs, despite recent improvements, have created headwinds that may impact future gross margins by increasing the cost of goods sold.

- The potential slowdown in sales growth, as indicated by a slight decline in February sales growth, may suggest softer consumer demand or external macroeconomic pressures that could affect revenue growth targets.

- Higher salary agreements in Finland could increase operating expenses, which may pressure operational margins if they are not offset by corresponding increases in revenue or operational efficiencies.

- A heavy dependence on maintaining a high store opening pace for growth could increase capital expenditures and operating expenses, which may dilute earnings if the new stores do not meet revenue expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK415.0 for Clas Ohlson based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK460.0, and the most bearish reporting a price target of just SEK360.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK15.2 billion, earnings will come to SEK1.5 billion, and it would be trading on a PE ratio of 21.0x, assuming you use a discount rate of 6.4%.

- Given the current share price of SEK411.2, the analyst price target of SEK415.0 is 0.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Clas Ohlson?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.