Last Update 17 Jun 26

AD.UN: Higher Distribution And Refined Assumptions Will Support Future Cash Flow Stability

Analysts have lifted their price targets on Alaris Equity Partners Income Trust by CA$3.00 and CA$0.50 in recent research, citing updated assumptions that leave the modelled fair value essentially unchanged, while modestly adjusting the discount rate and forward P/E inputs.

Analyst Commentary

Recent research on Alaris Equity Partners Income Trust points to a measured shift in analyst assumptions, with price targets adjusted while fair value estimates are described as broadly intact. For you as an investor, the key signals center on how analysts are thinking about valuation inputs, execution risk and the growth profile embedded in their models.

Bullish Takeaways

- Bullish analysts lifting price targets signal that, within their frameworks, current assumptions still support upside potential relative to where Alaris Equity Partners units are trading.

- The decision to adjust P/E inputs while keeping modelled fair value essentially unchanged suggests confidence that the company’s cash flow profile can support existing valuation ranges.

- Refined discount rate assumptions indicate that analysts see the risk profile as adequately reflected in their models, rather than requiring a material reset to expected returns.

- Multiple research updates in a short time window keep Alaris Equity Partners on the radar for institutional coverage, which can support more consistent scrutiny of execution and capital allocation.

Bearish Takeaways

- Even with higher price targets, analysts maintaining a steady fair value view implies limited conviction in materially re-rating the Alaris Equity Partners stock on current information.

- Adjustments to the discount rate and P/E inputs highlight that valuation for Alaris Equity Partners is sensitive to modest shifts in assumptions, which can constrain how aggressively some analysts underwrite upside.

- The modest scale of the price target changes suggests that, within these models, there may be less room for error on execution or distribution stability before estimates would need to be reworked.

- By fine tuning rather than overhauling their models, bearish analysts may see Alaris Equity Partners as fairly valued on their base case, which can temper expectations for outsized gains without new catalysts.

What’s in the News for Alaris Equity Partners Income Trust

- Alaris Equity Partners Income Trust announced a 3% increase in its quarterly distribution to $0.38 per unit (annualized $1.52). The change is described as being supported by capital deployment, reset growth and a payout ratio below its target range. Source, Key Developments

- Following the new distribution level, Alaris Equity Partners’ pro forma payout ratio is described at approximately 60%. This provides a reference point for how much cash flow is being returned to unitholders versus retained. Source, Key Developments

- Alaris Equity Partners Income Trust issued revenue guidance for the second quarter of 2026, with total partner revenue expected to be approximately $47.9 million, reflecting seasonal distribution timing. Source, Key Developments

Valuation Changes for Alaris Equity Partners Income Trust

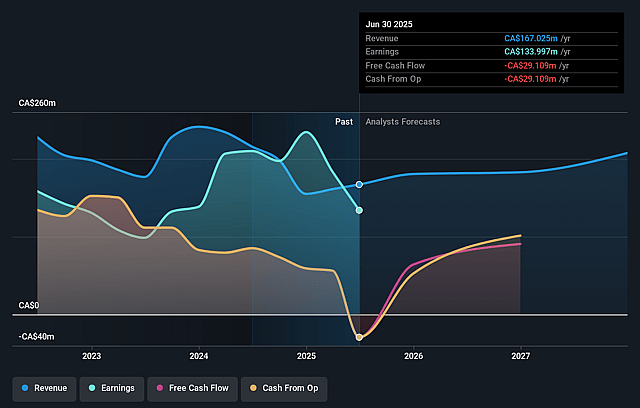

- Fair Value: The modelled fair value is unchanged at CA$27.22, indicating no revision to the core valuation estimate in the latest update.

- Discount Rate: The discount rate has moved slightly lower from 7.44% to 7.42%, a modest refinement rather than a major shift in risk assumptions.

- Revenue Growth: The revenue growth input remains effectively stable at 14.31%, with no meaningful change in the underlying growth assumption for Alaris Equity Partners.

- Net Profit Margin: The profit margin assumption is essentially flat at 54.74%, suggesting no material adjustment to expected profitability levels.

- Future P/E: The forward P/E multiple is marginally lower from 10.46x to 10.45x, implying only a very small change in how future earnings are being valued in the model.

Key Takeaways

- Strong transaction pipeline and strategic partnerships could enhance revenue growth and investment returns, offering greater optionality for future deals.

- Focus on share buybacks and U.S. service-based investments signals potential earnings growth, revenue stability, and an increase in book value per share.

- Changes in accounting standards and reliance on leverage could obscure financial transparency and impact net margins amidst operational challenges and economic uncertainties.

Catalysts

About Alaris Equity Partners Income Trust- A private equity firm specializing in management buyouts, growth capital, lower & middle market, later stage, industry consolidation, growth capital, and mature investments.

- Alaris Equity Partners’ future growth could benefit from a strong pipeline of potential transactions, supported by new partnerships with large asset management companies that enable Alaris to engage in larger deals. This is anticipated to impact revenue growth and optionality for investment returns.

- The anticipated increase in partner resets by approximately $5 million in 2025 and the higher-than-expected common distributions are likely to enhance future revenue, indicating a positive growth trajectory.

- Alaris’ strategic focus on share buybacks using free cash flows, with a plan to maintain a payout ratio of roughly 65%, suggests that earnings per share (EPS) could increase due to a reduced share count, contributing to a higher book value per share.

- The company's investment in service-based U.S. businesses, insulated from tariffs and economic turbulence, indicates sustainable cash flow and revenue stability that could bolster net margins, especially with 90% of revenue being in U.S. dollars.

- Increases in fair value of portfolio investments such as Fleet and Ohana, and anticipated recovery in EBITDA for some partners (e.g., Fleet’s recovery in 2025), highlight potential earnings growth and improvement in the overall valuation of Alaris’ investment portfolio.

Alaris Equity Partners Income Trust Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Alaris Equity Partners Income Trust's revenue will grow by 14.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 60.9% today to 54.7% in 3 years time.

- Analysts expect earnings to reach CA$145.3 million (and earnings per share of CA$1.94) by about June 2029, up from CA$108.3 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 10.7x on those 2029 earnings, up from 10.0x today. This future PE is greater than the current PE for the CA Capital Markets industry at 9.7x.

- Analysts expect the number of shares outstanding to grow by 0.31% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.42%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The change in accounting standards under IFRS 10 means Alaris no longer consolidates its investment entity subsidiaries. This could lead to misleading financial comparisons across periods, impacting clarity in reported revenues and earnings.

- The higher cost of advertising in the U.S. and declining conversion rates for Sono Bello could impact its EBITDA in the short term, affecting Alaris' revenue from this partner.

- Heritage's delayed return to profitability means it won't be able to support preferred distributions until 2026, affecting forecasted cash flow and net margins from this part of Alaris' portfolio.

- The potential impact of U.S. government spending cuts or tariffs could disrupt operations at partner firms like FMP, affecting the revenue and earnings from these companies within Alaris' investment portfolio.

- Despite a significant deployment pipeline, Alaris relies heavily on its revolver for funding and is planning an expansion of its debt facility. This reliance on leverage could impact net margins if interest rates rise.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$27.22 for Alaris Equity Partners Income Trust based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$29.0, and the most bearish reporting a price target of just CA$24.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CA$265.4 million, earnings will come to CA$145.3 million, and it would be trading on a PE ratio of 10.7x, assuming you use a discount rate of 7.4%.

- Given the current share price of CA$23.72, the analyst price target of CA$27.22 is 12.9% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Alaris Equity Partners Income Trust?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.