Last Update 23 Jul 26

Fair value Decreased 11%TAALEEM: Upcoming Board Reviews Will Support Future Upside Potential

Analysts have trimmed their fair value estimate for Taaleem Holdings PJSC from AED 5.30 to about AED 4.72, reflecting updated views on growth, margins, and future P/E assumptions for the stock.

What’s in the News for Taaleem Holdings PJSC

- Taaleem Holdings PJSC has scheduled a board meeting on May 21, 2026, at 11:00 Coordinated Universal Time to discuss routine business issues, review the company’s activities, and consider any other matters with the permission of the Chairman. (Source: Company key developments)

- A subsequent board meeting is planned for June 18, 2026, at 11:00 Coordinated Universal Time. The agenda will focus on Taaleem Holdings PJSC’s activities and any additional items raised with the Chairman’s permission. (Source: Company key developments)

- The board of Taaleem Holdings PJSC is set to meet again on July 9, 2026, at 11:00 Coordinated Universal Time to consider and approve the interim consolidated financial statements for the nine month period ended May 31, 2026. The meeting will also include a review of company activities and other matters approved by the Chairman. (Source: Company key developments)

Valuation Changes for Taaleem Holdings PJSC

- Fair Value: Updated estimate reduced from AED 5.30 to about AED 4.72, indicating a lower implied valuation per share based on the latest assumptions.

- Discount Rate: Adjusted slightly from 20.34% to 20.27%, reflecting a small change in the required rate of return used in the valuation model.

- Revenue Growth: Revised from 11.04% to 10.06%, indicating a more moderate expected pace of revenue expansion for Taaleem Holdings PJSC in the model.

- Net Profit Margin: Reduced from 14.65% to 13.16%, pointing to a more conservative view on future profitability levels.

- Future P/E: Model assumption moved from 36.61x to 35.28x, reflecting a slightly lower multiple applied to projected earnings.

Key Takeaways

- Expanding student capacity and premium market focus are expected to drive revenue growth and enhance profitability.

- Strategic funding through debt and IPO proceeds supports growth while maintaining a strong balance sheet and stable net debt levels.

- Expansion efforts and financial strategies, such as increased debt for acquisitions, expose the company to risks of lower revenue, net margins, and liquidity challenges.

Catalysts

About Taaleem Holdings PJSC- Provides and invests in education services in the United Arab Emirates.

- The acquisition of Lycée Libanais Francophone Privé and the expansion of Dubai British School Emirates Hills are expected to significantly increase enrollment and revenue growth over the coming years.

- The expansion in student capacity by around 10,000 seats between 2024 and 2026, through both mergers & acquisitions and greenfield projects, is likely to drive up future revenue.

- The ramp-up of newly opened schools, such as Dubai British School Jumeira and the Lycée Libanais, is expected to improve utilization rates and margins over time, enhancing future profitability.

- Taaleem’s focus on premium and super premium segments, characterized by resilient fee structures and high growth potential, is anticipated to support sustained revenue growth and margin expansion.

- The strategic use of debt and IPO proceeds to fund expansions and acquisitions while maintaining a strong balance sheet is expected to support growth in earnings without significantly impacting net debt levels.

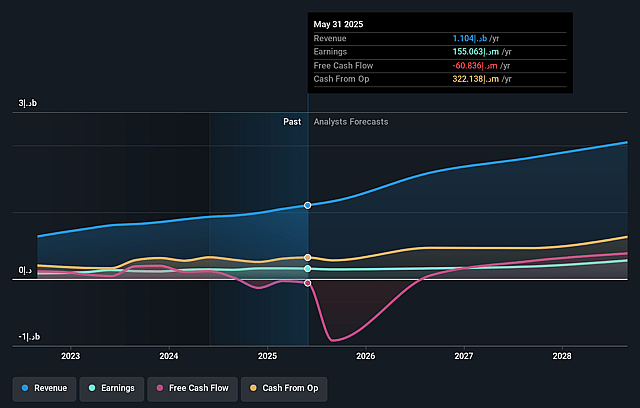

Taaleem Holdings PJSC Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Taaleem Holdings PJSC's revenue will grow by 10.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 14.2% today to 13.2% in 3 years time.

- Analysts expect earnings to reach AED 231.9 million (and earnings per share of AED 0.27) by about July 2029, up from AED 187.8 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as AED188.5 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 35.3x on those 2029 earnings, up from 16.7x today. This future PE is greater than the current PE for the AE Consumer Services industry at 14.3x.

- Analysts expect the number of shares outstanding to decline by 0.06% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 20.27%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- There is a noted decline in premium utilization due to the addition of significant new capacity without a corresponding immediate increase in enrollment, which could lead to lower revenue and net margins.

- The company is experiencing increased operating costs, particularly in staffing and utilities, attributed to its expansion, which can affect net margins and overall profitability.

- There is a negative free cash flow in Q1, suggestive of the company's cash flow seasonality and potential liquidity issues impacting the balance sheet, especially with the simultaneous execution of multiple capital-intensive projects.

- The increased debt burden used to finance acquisitions and growth might strain the company’s financial health, potentially affecting earnings if interest rates fluctuate unfavorably or if anticipated returns don't materialize.

- Dependence on external factors like regulatory changes in the academic year start and its impact on revenue recognition underscores risks in achieving earnings predictability and consistency.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of AED4.72 for Taaleem Holdings PJSC based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be AED1.8 billion, earnings will come to AED231.9 million, and it would be trading on a PE ratio of 35.3x, assuming you use a discount rate of 20.3%.

- Given the current share price of AED3.14, the analyst price target of AED4.72 is 33.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Taaleem Holdings PJSC?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.