Last Update 09 Jun 26

3711: Future Returns Will Rely On Panel Packaging While P/E Stays Rich

Analysts have maintained their NT$536.53 price target for ASE Technology Holding, indicating consistent views on fair value, discount rate, revenue growth assumptions, and profit margin expectations.

What's in the News

- Advanced Semiconductor Engineering Inc. announced an automated 310 mm × 310 mm panel-level packaging production line, designed to support FOCoS and FOCoS-Bridge platforms with line and space capabilities of 2/2 µm and 8/8 µm.

- The new panel format is described as allowing up to 96,100 mm² usable area per panel, targeting applications such as AI data centers, high performance computing, networking, high-end gaming, and edge AI, and is expected to enter production in the first half of 2027.

- ASE Technology Holding Co., Ltd. reported unaudited consolidated net revenues of TWD 61,577 million for March 2026, compared with TWD 53,748 million for March 2025. Source: company announcement of operating results.

- Advanced Semiconductor Engineering Inc. plans to participate in the 76th IEEE Electronic Components and Technology Conference in Orlando, Florida, from May 26 to May 29, 2026, highlighting its panel-level packaging platform and advanced packaging solutions.

Valuation Changes

- Fair Value: NT$536.53 remains unchanged, indicating no adjustment to the assessed fair value of the stock.

- Discount Rate: 11.27% is unchanged, so the risk and return assumptions used in the valuation stay the same.

- Revenue Growth: 19.65% is effectively unchanged, with only an immaterial rounding difference in the updated figure.

- Net Profit Margin: 12.25% is also effectively unchanged, with only a minor numerical refinement in the updated estimate.

- Future P/E: 23.67x is unchanged, indicating that valuation expectations relative to projected earnings remain consistent with the prior view.

Key Takeaways

- Diversified growth in advanced packaging, automation, and new technologies is driving higher-margin potential and positioning ASE as a key industry player for next-generation demands.

- Margin pressures from costs and foreign exchange are expected to ease as automation ramps and value-added services enable more stable, resilient, and diversified earnings.

- Persistent currency volatility, capacity constraints, rising leverage, market cyclicality, and geopolitical risks collectively threaten ASE's margins, scaling ability, earnings stability, and global competitiveness.

Catalysts

About ASE Technology Holding- Provides semiconductor manufacturing services in assembly and testing in the United States, Taiwan, Europe, Asia, and internationally.

- ASE is experiencing strong, multi-year demand driven by the expansion of global data centers, proliferation of AI applications, and increasing semiconductor content per device across end-markets. This should support sustained revenue growth into 2026 and beyond as advanced packaging and testing needs accelerate.

- Investments in leading-edge technologies (3D IC, chiplet, system-in-package, silicon photonics) and aggressive capacity expansion-especially in advanced packaging/test and fully automated lines-position ASE as a key player to meet next-generation requirements, enabling higher-margin mix and long-term operating margin expansion.

- The increasing pace of digital transformation in automotive, industrial, and networking segments is boosting high-margin demand for ASE's services outside traditional consumer electronics, supporting more stable and resilient earnings and diversifying revenue streams.

- Margins are temporarily pressured by foreign exchange headwinds and early ramp-up costs, but management anticipates a return to structural margin levels by 2026 as utilization improves, cost efficiencies from automation ramp, and pricing recalibrates to reflect value-added capabilities, benefiting future net margins and earnings.

- Tight capacity environment and high CapEx investments today are largely customer-driven, with long-term orders and ecosystem partnerships in place. As these capacity additions come online and resource optimization initiatives take effect, ASE can better leverage scale, capture incremental volume, and realize improved returns on capital, positively impacting future operating and net margins.

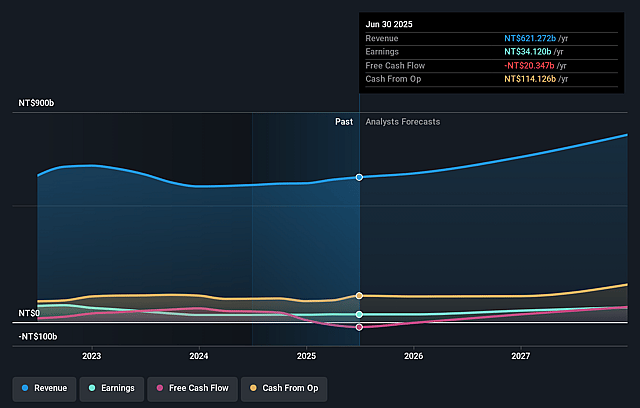

ASE Technology Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming ASE Technology Holding's revenue will grow by 19.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.0% today to 12.2% in 3 years time.

- Analysts expect earnings to reach NT$140.8 billion (and earnings per share of NT$28.39) by about June 2029, up from NT$47.3 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting NT$170.0 billion in earnings, and the most bearish expecting NT$108.9 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 23.7x on those 2029 earnings, down from 50.2x today. This future PE is lower than the current PE for the US Semiconductor industry at 44.4x.

- Analysts expect the number of shares outstanding to grow by 0.9% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.27%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent foreign exchange volatility, particularly NT dollar appreciation against the US dollar, is having a significant and direct negative impact on ASE's gross and operating margins; this currency risk remains a structural threat that could continue to erode profitability and reported earnings if left unmitigated.

- The company is facing substantial resource constraints-including execution risk, human talent shortages, land, facility, and machine delivery issues-that are limiting its ability to rapidly scale capacity to meet surging demand, potentially resulting in missed revenue opportunities and higher operational pressure.

- Ongoing, heavy capital expenditures funded through rising debt are increasing financial leverage and net debt-to-equity ratios; if anticipated returns or market growth do not materialize as planned, this creates long-term pressure on net margins and could limit financial flexibility.

- There are signs of market disparity and potential cyclicality, with non-AI segments (such as PC, smartphone, and general EMS) described as slow or inconsistent; over-reliance on the AI and advanced packaging/testing wave exposes ASE to earnings volatility if there is a pause or slowdown in that domain.

- Geopolitical risks and regulatory controls-including evolving tariffs, BIS restrictions, and worldwide deglobalization trends-may require costly overseas investments, resource diversion, or loss of market access, all of which threaten revenue growth and global competitiveness in the longer term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of NT$536.53 for ASE Technology Holding based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NT$660.0, and the most bearish reporting a price target of just NT$161.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be NT$1149.3 billion, earnings will come to NT$140.8 billion, and it would be trading on a PE ratio of 23.7x, assuming you use a discount rate of 11.3%.

- Given the current share price of NT$540.0, the analyst price target of NT$536.53 is 0.6% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on ASE Technology Holding?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.