Key Takeaways

- Dell Technologies is targeting AI technology growth, emphasizing AI-optimized servers for potential future revenue and earnings increase.

- Focusing on operational excellence and expense management suggests improved operating and net margins, alongside growth in server and storage demand.

- Competitive pressures and increasing costs in AI and traditional server markets may hurt profits, margins, and delay revenue growth.

Catalysts

What are the underlying business or industry changes driving this perspective?

- Dell Technologies Inc. designs, develops, manufactures, markets, sells, and supports various comprehensive and integrated solutions, products, and services in the Americas, Europe, the Middle East, Asia, and internationally.

- Dell Technologies is capitalizing on the high-growth AI opportunity with its AI-optimized server portfolio, indicating future revenue growth from the increasing demand for AI solutions. This is expected to positively impact earnings as the company continues to see strong demand and expand its AI capabilities.

- There is an emphasis on operational excellence and disciplined expense management, improving operating margin rate and delivering higher gross margins. This suggests a future positive impact on net margins as Dell focuses on maintaining profitability even in challenging market conditions.

- Dell is experiencing growth in both traditional server demand and storage demand, especially with the AI build-out, suggesting future revenue growth in these areas. This growth is partly due to the company's positioning and offerings that cater to the needs of GenAI solutions, impacting both revenue and net income positively.

- The enhancement of Dell's capital allocation, including increased dividends, reflects confidence in future cash flow generation. This is a positive signal for earnings per share growth as the company continues to return value to shareholders.

- Dell's focus on AI and the expected PC refresh cycle due to aging PC installed base and Windows 10 reaching end-of-life indicate potential revenue growth from new product and solution launches that meet future demands, especially in AI-enabled PCs and solutions. This forward-looking strategy is likely to have a positive impact on revenue and earnings.

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Dell Technologies's revenue will grow by 5.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.6% today to 4.7% in 3 years time.

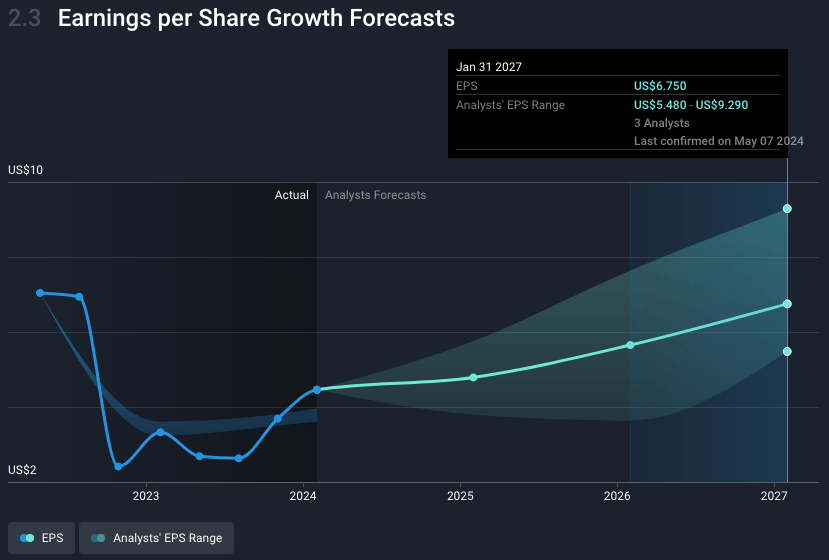

- Analysts expect earnings to reach $4.9 billion (and earnings per share of $6.75) by about May 2027, up from $3.2 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish analysts expecting $6.7 billion in earnings, and the most bearish anlaysts expecting $3.7 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.3x on those 2027 earnings, down from 29.3x today. This future PE is lower than the current PE for the None Tech industry at 24.5x.

- Analysts expect the number of shares outstanding to grow by 0.85% per year for the next 3 years.

- To value all of this in today's dollars, we will use a discount rate of 8.59%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Competitive pricing pressure on AI servers could lower profit margins in that high-growth segment, impacting overall profitability.

- Increasing inflationary input costs, especially in components such as memory, could reduce gross margins further, negatively affecting net income.

- A cautious spending environment, particularly in the PC market and among large enterprise customers, may delay expected revenue growth, especially in the first half of FY '25.

- Dependence on GPU supply for AI-optimized servers could hinder the ability to meet demand, affecting revenue and growth projections in the AI segment.

- Intensifying competition in both the AI and traditional server markets could force more aggressive pricing and spending on marketing and R&D, potentially impacting operating margins and net income.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $127.67 for Dell Technologies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $152.0, and the most bearish reporting a price target of just $55.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $104.3 billion, earnings will come to $4.9 billion, and it would be trading on a PE ratio of 22.3x, assuming you use a discount rate of 8.6%.

- Given the current share price of $131.61, the analyst's price target of $127.67 is 3.1% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company’s future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.’s analysis may not factor in the latest price-sensitive company announcements or qualitative material.