Last Update 25 Jun 26

SCATC: Tunisian Solar Expansion And Long-Term PPAs Will Support Future Cash Flows

Analysts have raised their Scatec price target to NOK 129.89, with the updated view reflecting a slightly higher discount rate and continued reliance on robust revenue growth and profit margin assumptions, as recent research turns more positive on the stock.

What’s in the News for Scatec

- Scatec and partner Aeolus SAS reached financial close and started construction of the 120 MW Sidi Bouzid II solar power plant in Tunisia, a government tender project that supports Tunisia’s target of 35% renewable energy generation by 2030 and aims to improve national energy security. (Source: company announcement)

- Scatec and Aeolus achieved commercial operations for the 60 MW Tozeur and 60 MW Sidi Bouzid solar plants in Tunisia, awarded through government tenders and together expected to produce about 288 GWh of electricity per year, with an estimated abatement of more than 115,000 tonnes of CO2 annually. Scatec owns 51% of these projects and will provide Operations & Maintenance and Asset Management services. (Source: company key developments)

- Scatec’s joint venture with Aboitiz Power in the Philippines started commercial operation of the 16 MW Magat battery energy storage system, connected to the Magat hydro power plant and earning revenues from the ancillary services reserves market, adding to the existing 24 MW battery system at the site. (Source: company key developments)

- Scatec reported total power production of 1,046 GWh for the first quarter ended March 31, 2026, compared with 947 GWh in the same period a year earlier. (Source: company operating results)

- Scatec issued power production guidance for the second quarter and full year 2026, indicating an expected range of 1,150 GWh to 1,250 GWh for the quarter and 5,050 GWh to 5,450 GWh for the year. (Source: company guidance)

Valuation Changes

- Fair Value: NOK 129.89 is unchanged compared with the previous estimate.

- Discount Rate: has risen slightly from 9.90% to 10.35%, implying a modestly higher required return for Scatec.

- Revenue Growth: assumption remains broadly stable at about 48.0%.

- Net Profit Margin: assumption is effectively unchanged at about 21.7%.

- Future P/E: has inched up from 10.85x to 10.99x, pointing to a slightly higher earnings multiple being applied to Scatec.

Key Takeaways

- Expansion into emerging markets offers growth but brings significant geopolitical, currency, and regulatory risks that could impact cash flow stability and earnings.

- Market optimism on rapid margin and revenue growth may be misplaced due to potential technology price stabilization, supply disruptions, and financing cost challenges.

- Strong financial discipline, diverse growth portfolio, and early adoption of batteries position Scatec for resilient earnings, reduced risk, and sustained margin expansion across global markets.

Catalysts

About Scatec- Provides renewable energy solutions worldwide.

- Investor optimism appears high regarding Scatec's expansion into emerging markets like Egypt and South Africa, where the company has secured record project backlogs and near-term growth, but this strategy exposes the company to heightened geopolitical and currency risks, potentially increasing future cash flow volatility and impacting earnings and net margins.

- The market may be overvaluing Scatec due to the expectation that falling renewable technology and battery costs will continually translate into higher margins and rapid capacity additions; however, if technology prices stabilize or supply chain disruptions return, future margin improvement and revenue growth could fall short of expectations.

- Overreliance on government contracts, PPAs, and regulatory approvals-especially in developing countries-means that any shifts in policy support, fiscal tightening, or payment delays could risk lower-than-anticipated revenue visibility and introduce downward pressure on future earnings.

- High expectations are likely being placed on Scatec's ability to efficiently execute its large pipeline and ramp up its operating portfolio, but persistent industry issues like grid constraints, project delays, and curtailments (as already hinted in Brazil and Ukraine) may disrupt revenue timing and compress overall returns.

- Assumptions of easy capital access and continuous deleveraging may be optimistic given the potential for persistently high global interest rates, which could increase project financing costs and reduce net margins if debt servicing becomes more expensive than currently projected.

Scatec Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Scatec's revenue will grow by 48.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.5% today to 21.7% in 3 years time.

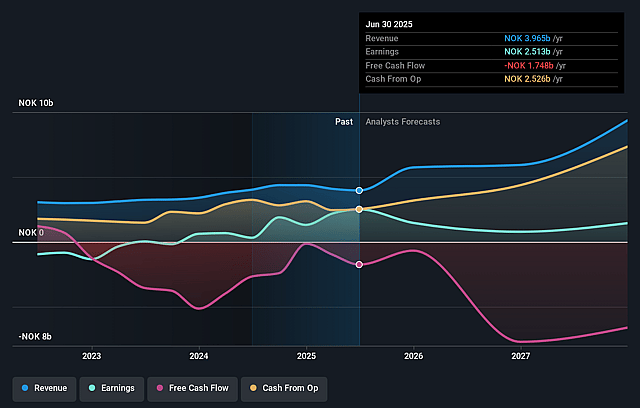

- Analysts expect earnings to reach NOK 2.5 billion (and earnings per share of NOK 11.15) by about June 2029, up from NOK 56.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting NOK3.8 billion in earnings, and the most bearish expecting NOK1.0 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 11.0x on those 2029 earnings, down from 278.6x today. This future PE is lower than the current PE for the GB Renewable Energy industry at 21.5x.

- Analysts expect the number of shares outstanding to grow by 0.31% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.35%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Scatec's strong financial performance, exemplified by significant year-on-year growth in revenue and EBITDA, robust OpEx control, and high gross margins from both power production and development/construction activities, indicates healthy and resilient earnings potential that could support share price appreciation.

- The company's rapidly expanding growth portfolio-including a record-high backlog of 3.2 GW, an additional 2 GW under construction, and a pipeline of 7.7 GW of mature projects across multiple technologies and geographies-signals the potential for continued top-line growth and a doubling of installed capacity over the next two years, which would positively impact future revenues.

- Continued reduction in corporate debt and strengthening of the balance sheet, with a clear deleveraging strategy, enhanced capital efficiency, and improved financial flexibility, lowers financial risk and creates capacity for self-funded growth, supporting strong net margins and earnings stability.

- Accelerating adoption of battery storage and hybrid solutions, particularly the unexpected earnings upside from batteries in the Philippines, positions Scatec to capitalize on long-term trends in grid flexibility and reserves markets, potentially increasing recurring revenues and improving profit margins as these technologies scale.

- Scatec's diversified global footprint (notably in South Africa, Egypt, the Philippines, and new markets) and active asset rotation strategy provide resilience against regional risks and generate recurring proceeds from divestments, which together underpin consistent cash flows, margin expansion, and share price support through business cycles.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of NOK129.89 for Scatec based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK150.0, and the most bearish reporting a price target of just NOK120.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be NOK11.7 billion, earnings will come to NOK2.5 billion, and it would be trading on a PE ratio of 11.0x, assuming you use a discount rate of 10.4%.

- Given the current share price of NOK97.6, the analyst price target of NOK129.89 is 24.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Scatec?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.