Last Update 25 Mar 26

PSL: Tanker Diversification And Stable Assumptions Will Shape A Balanced Outlook

Analysts have adjusted their price target for Precious Shipping to THB7.23, reflecting updated assumptions for the discount rate, revenue growth, profit margin, and future P/E. These changes keep the fair value estimate broadly unchanged.

What's in the News

- Acquisition of secondhand Medium Range tanker M/T FLORENCE for US$11.10 million, or about THB344.62 million, by wholly owned subsidiary Precious Horizon Pte. Ltd., with delivery scheduled between 20 February and 15 March 2026 (Key Developments).

- The company highlights that the M/T FLORENCE purchase is intended to diversify its fleet into the tanker segment to broaden revenue sources beyond dry bulk shipping (Key Developments).

- On 19 January 2026, a wholly owned Singapore subsidiary took delivery of the vessel M.V. Uthita Naree, bringing the fleet size to 41 vessels (Key Developments).

- On 15 January 2026, a wholly owned Singapore subsidiary took delivery of the vessel M.V. Ubon Naree; at that time, the fleet comprised 40 vessels (Key Developments).

Valuation Changes

- Fair Value: THB7.23 per share remains unchanged, indicating the updated assumptions do not alter the overall valuation outcome.

- Discount Rate: risen slightly from 9.59% to 9.88%, implying a marginally higher required return being factored into the model.

- Revenue Growth: kept effectively flat at 3.63%, suggesting no change to the underlying growth outlook used in the valuation.

- Net Profit Margin: held steady at about 13.41%, with only a very small adjustment in the fourth decimal place.

- Future P/E: increased slightly from 15.55x to 15.68x, reflecting a modest tweak to the assumed earnings multiple applied to future profits.

Key Takeaways

- Strategic fleet upgrades and long-term charters enhance efficiency, reduce costs, and ensure steady revenue growth for Precious Shipping.

- Favorable supply-demand dynamics and geopolitical developments could further boost Precious Shipping's revenue and earnings potential.

- Rapid fleet growth could lead to oversupply, impacting freight rates and revenue amidst geopolitical tensions and uncertain demand forecasts.

Catalysts

About Precious Shipping- Owns and operates dry bulk ships on a tramp shipping basis worldwide.

- China's increased steel exports and infrastructure development, particularly in shipbuilding and electric cars, are driving demand for dry bulk shipping, benefiting Precious Shipping's fleet utilization and potentially boosting revenue.

- The projected global trade growth in dry bulk, driven by low commodity prices and high demand, exceeding fleet growth, suggests a favorable supply-demand dynamic for Precious Shipping, improving net margins.

- The company's strategic acquisition of eco-engine ships to replace older, less efficient vessels is likely to reduce operating costs and enhance earnings by improving fleet fuel efficiency.

- With a significant portion of the fleet on long-term and index-linked charters, Precious Shipping benefits from steady cash flow and mitigates risks from fluctuating spot rates, supporting stable revenue growth.

- Potential geopolitical developments, including a resolution to the Russia-Ukraine conflict, could lower oil prices and boost dry bulk trade flows, positively impacting Precious Shipping's future earnings potential.

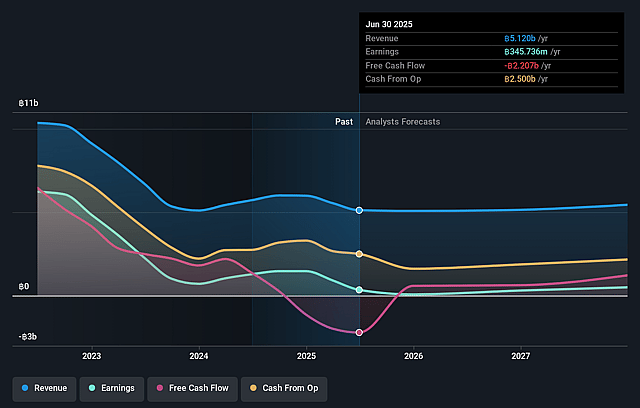

Precious Shipping Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Precious Shipping's revenue will grow by 3.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.9% today to 13.4% in 3 years time.

- Analysts expect earnings to reach THB 784.0 million (and earnings per share of THB 0.5) by about March 2029, up from THB 413.8 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.7x on those 2029 earnings, down from 24.9x today. This future PE is lower than the current PE for the TH Shipping industry at 16.7x.

- Analysts expect the number of shares outstanding to decline by 4.78% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.88%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The rapid fleet growth potential, with the dry bulk fleet expected to grow by 3.2% in 2024 and 2.9% in 2025, could lead to an oversupply situation, potentially impacting freight rates and reducing overall revenue.

- The inability of industry forecasters like Clarksons to accurately predict tonne-mile demand and fleet growth introduces significant uncertainty, which could affect market conditions and ultimately impact earnings.

- The continued geopolitical tensions, such as U.S.-China tariffs and potential increased tariffs under a Trump presidency, pose risks to global trade flow and could negatively impact cargo volumes, affecting revenue.

- The reduction in net profit from USD 14.4 million in Q2 to USD 8.2 million in Q3 2024 despite a moderate increase in demand suggests vulnerability in maintaining profitability, which could impact net margins.

- The slower than anticipated economic growth rates forecasted by the IMF and unreliable growth indicators in global dry bulk trade pose risks to future earnings, hindering sustainable revenue increases.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of THB7.23 for Precious Shipping based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of THB7.7, and the most bearish reporting a price target of just THB6.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be THB5.8 billion, earnings will come to THB784.0 million, and it would be trading on a PE ratio of 15.7x, assuming you use a discount rate of 9.9%.

- Given the current share price of THB6.95, the analyst price target of THB7.23 is 3.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Precious Shipping?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.