Last Update 14 Jun 26

LEADD: Hospital Contract And Refined Assumptions Will Support Future Upside

Analysts kept their €4.70 fair value estimate for LeadDesk Oyj steady while adjusting underlying assumptions such as discount rate, profit margin and future P/E, signalling a refined view of the stock’s risk and earnings profile rather than a change in headline valuation.

What's in the News

- LeadDesk Plc has been selected as the supplier of the customer service and contact center system for the Hospital District of Helsinki and Uusimaa (HUS) following a public procurement process. [Source: Key Developments]

- The agreement with HUS has an estimated value of approximately €1.3 million over three years, with the possibility to continue until further notice based on the terms of the arrangement. [Source: Key Developments]

- LeadDesk will provide HUS with a customer service solution that entered its product portfolio through the acquisition of Norwegian company Zisson AS, completed in 2025. [Source: Key Developments]

- The solution is intended to support HUS's customer service and contact center system needs, as well as the operations of its various units. [Source: Key Developments]

Valuation Changes

- Fair Value: The €4.70 fair value estimate is unchanged, indicating no adjustment to the overall valuation level.

- Discount Rate: The discount rate has risen slightly from 9.05% to 9.34%, pointing to a modestly higher assumed risk level.

- Revenue Growth: The long term revenue growth assumption is effectively unchanged at about 44.4%.

- Net Profit Margin: The assumed net profit margin has eased from 15.23% to 14.53%, reflecting a slightly more conservative earnings outlook.

- Future P/E: The future P/E multiple has risen from 5.02x to 5.30x, implying a somewhat higher valuation multiple applied to projected earnings.

Key Takeaways

- Integration progress, operational improvements, and enhanced efficiency are set to boost recurring earnings and margins through scalability and cost control.

- AI-driven solutions and a strategic enterprise focus position LeadDesk to capture automation growth, increase customer retention, and expand in underpenetrated European markets.

- Heavy reliance on acquisitions and complex integrations, rising customer concentration, and intense competition threaten sustainable growth, margin stability, and successful market repositioning.

Catalysts

About LeadDesk Oyj- Provides cloud-based contact center solutions for sales outreach and customer service in Finland.

- The ongoing integration of Zisson is on track, with key cost and revenue synergies (including cross-selling, partner network expansion, and operational improvements) expected to become fully visible by Q4 2025 and especially during 2026, likely driving stronger EBITDA margins and earnings growth.

- Significant investment in AI-powered solutions (such as AI Insights and Voicebot) and early adoption by over one third of LeadDesk's customer base position the company to capitalize on accelerating automation and demand for omnichannel customer experience, supporting future revenue growth and higher upsell per customer.

- The strategic shift upmarket toward larger enterprise clients in the Nordics is improving customer stickiness (retention), broadening recurring revenue streams, and setting a stronger foundation for organic growth and net revenue retention rates.

- Accelerated expansion in Continental Europe, particularly Spain, targets a large, underpenetrated market, leveraging both organic growth through new logos and inorganic growth through targeted M&A-directly increasing topline revenues.

- Enhanced operational efficiency initiatives (including ERP implementation and process streamlining) are expected to increase scalability and cost control, enabling LeadDesk to improve operating leverage and EBITDA margins as it pivots from integration to growth.

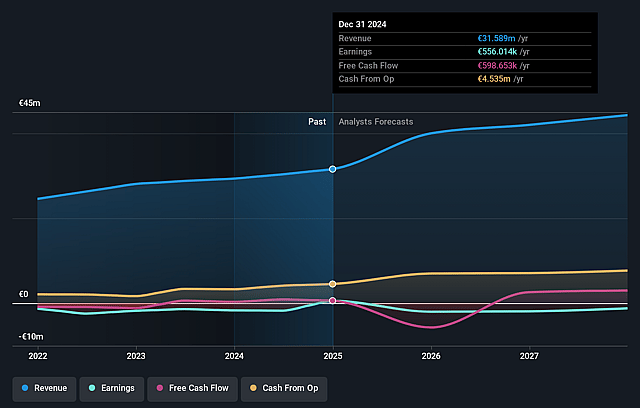

LeadDesk Oyj Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming LeadDesk Oyj's revenue will remain fairly flat over the next 3 years.

- Analysts are not forecasting that LeadDesk Oyj will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate LeadDesk Oyj's profit margin will increase from -6.0% to the average FI Software industry of 14.5% in 3 years.

- If LeadDesk Oyj's profit margin were to converge on the industry average, you could expect earnings to reach €5.8 million (and earnings per share of €1.0) by about June 2029, up from -€2.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 6.2x on those 2029 earnings, up from -8.3x today. This future PE is lower than the current PE for the FI Software industry at 20.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.34%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Organic growth appears to be lagging behind overall revenue growth, with acquisitions (particularly Zisson) driving much of the recent expansion; this creates a risk of over-reliance on M&A for topline increases and may mask slowdowns in underlying demand, impacting the sustainability of revenue growth.

- The company is undergoing a complex integration of Zisson and new partner-led sales models (particularly in Sweden), with full cost and revenue synergies yet to be realized; failure to properly harmonize cultures, systems, and sales channels could lead to delays, unexpected costs, or missed synergies, which may negatively affect net margins and earnings.

- The shift in Nordic markets from SME to larger, more complex enterprise clients increases customer concentration risk and lengthens sales cycles; losing major clients or failing to secure new large contracts could introduce significant volatility in recurring revenues and earnings.

- Escalating R&D and operational investment-driven by the need to keep pace with rapid AI developments and regulatory requirements (e.g., GDPR, forthcoming EU AI Act)-may put persistent pressure on margins, especially if revenue growth slows or investments do not yield expected upsell/cross-sell opportunities.

- The highly fragmented European CCaaS market could consolidate further or attract global players with more resources, intensifying competition and potentially eroding pricing power for LeadDesk Oyj; this environment may strain net margins and make it harder to achieve and sustain their ambitious growth and profitability targets.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €4.7 for LeadDesk Oyj based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €39.9 million, earnings will come to €5.8 million, and it would be trading on a PE ratio of 6.2x, assuming you use a discount rate of 9.3%.

- Given the current share price of €3.36, the analyst price target of €4.7 is 28.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on LeadDesk Oyj?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.