Last Update 07 Apr 26

Fair value Decreased 2.04%SAN: Future Upside Will Rely On Pipeline Delivery And Margin Expansion

Analysts trimmed Sanofi's fair value estimate by €2.00 to €96.10, citing updated assumptions that include slightly different revenue growth, a higher profit margin profile, and a lower future P/E multiple.

Analyst Commentary

Recent Street research on European financials and cross border bank deals offers some reference points that investors can use when thinking about Sanofi's updated fair value and how sentiment can swing as assumptions change.

Bullish Takeaways

- Bullish analysts often point to efficiency gains and operating leverage as key supports for higher valuation multiples, suggesting that companies which execute on cost control and productivity can justify richer P/E assumptions.

- Where analysts see a company as an "execution led compounding story," they tend to reflect that view in higher price targets, linking consistent delivery on plans to a willingness to pay up for future earnings.

- Upgrades and target moves that reference scale in core markets highlight how expanding in areas with previously sub optimal returns can, in the eyes of bullish analysts, help support a premium valuation over time.

- In merger situations, some bullish analysts focus on improved terms or clarified exchange ratios as supportive for the target's equity story, particularly when they see the combined entity as more efficient.

Bearish Takeaways

- Bearish analysts often focus on deal risk and regulatory uncertainty, flagging that transactions which appear straightforward on paper can face approval challenges that weigh on valuation.

- Downgrades tied to macro or political comments, such as potential trade restrictions between countries, show how quickly sentiment can shift when analysts see higher execution or closure risk around a transaction.

- Target reductions, even small ones, usually reflect more cautious assumptions around key drivers like growth, margins, or acceptable future P/E multiples, which can limit upside in their models.

- When analysts move ratings lower while peers remain optimistic, it underlines that even within broadly positive coverage, there can be concern about whether current prices already discount much of the execution story.

For Sanofi, the recent trim in fair value and changes to revenue growth, margin profile, and the assumed P/E multiple fit into this broader pattern, with analysts fine tuning their models as they weigh execution quality, regulatory and deal risks, and how much investors may be willing to pay for future earnings.

What's in the News

- Sanofi reported consolidated impairment of intangible assets of €2.01b for Q4 2025 compared with €439m a year earlier, and also proposed a dividend of €4.12 per share for 2025. The company issued 2026 guidance that points to high single digit sales growth at constant exchange rates, with business EPS growth expected to be slightly faster. (company announcement)

- The Board decided not to renew CEO Paul Hudson’s director mandate, with his last day as CEO set for 17 February 2026. It appointed Olivier Charmeil as interim CEO and named former Merck KGaA CEO Belén Garijo to take over as CEO after the 29 April 2026 AGM, alongside proposed bylaw changes including a higher age limit for the CEO role. (company announcement)

- Sanofi and Regeneron secured multiple Dupixent milestones, including Japan approval for bullous pemphigoid, EU committee backing for use in chronic spontaneous urticaria in children aged 2 to 11 years, and US FDA approval for allergic fungal rhinosinusitis in patients aged 6 years and older with prior sino nasal surgery. (company and regulatory announcements)

- Across the pipeline, Sanofi reported positive late stage data in several programs, including phase 3 results for amlitelimab in atopic dermatitis, FDA Breakthrough Therapy designation for venglustat in type 3 Gaucher disease, breakthrough therapy and orphan designations for rilzabrutinib in warm autoimmune hemolytic anemia, and phase 2 success for lunsekimig in asthma and chronic rhinosinusitis with nasal polyps. (company announcements)

- Regulatory and partnership news extended beyond immunology, with conditional EU approval for Rezurock in chronic graft versus host disease, EU approval of Teizeild to delay onset of stage 3 type 1 diabetes, China approvals for Sanofi licensed Myqorzo and Redemplo, and an expanded collaboration with Mirecule on Antibody RNA Conjugate therapies for facioscapulohumeral muscular dystrophy. (company and regulatory announcements)

Valuation Changes

- Fair Value was trimmed from €98.10 to €96.10, a reduction of about €2.00 per share.

- The Discount Rate is unchanged at 6.288%, so the required return assumption stays the same.

- Revenue Growth was adjusted slightly higher from 3.67% to 3.69%.

- The Net Profit Margin was lifted from 20.05% to 21.05%, implying a higher share of € sales flowing through to earnings in the model.

- The assumed future P/E moved lower from 12.76x to 11.90x, pointing to a more cautious earnings multiple.

Key Takeaways

- Continued investment in innovative products, strategic acquisitions, and portfolio streamlining is positioning Sanofi for long-term growth in high-value therapeutic areas.

- Leadership in biologics and vaccines, alongside regulatory opportunities, supports revenue stability and operating efficiency amid evolving market dynamics.

- Prolonged pricing pressures, R&D setbacks, and rising costs from acquisitions and regulations threaten Sanofi's margins and future growth amid increasing post-patent competition.

Catalysts

About Sanofi- A healthcare company, engages in the research, development, manufacture, and marketing of therapeutic solutions in the United States, Europe, and internationally.

- Sanofi's ongoing focus on innovative product launches and its strong R&D pipeline-highlighted by accelerating investments, multiple Phase III readouts through 2026, and continued expansion of biologics (e.g., Dupixent, amlitelimab)-position the company to capture higher demand for chronic disease treatments in a world with an aging population, supporting robust long-term sales growth and EPS upside. (Revenue, EPS)

- Strategic expansion into rare disease and immunology through targeted acquisitions (e.g., Blueprint Medicines with Ayvakit, Vigil Neuroscience, Vicebio) will expand Sanofi's presence in high-growth, premium-priced therapeutic areas, broadening its addressable patient base as global healthcare access increases, and driving net margin and revenue improvement over time. (Revenue, Net Margins)

- Dupixent's continued growth across multiple indications-including recent launches in COPD, CSU, and bullous pemphigoid-along with significant potential for geographic and indication expansion (notably in underpenetrated markets such as China), underpins a credible pathway to €22 billion in 2030 sales, supporting sustained top-line growth and improved operating leverage. (Revenue, Net Margins)

- Portfolio streamlining-such as the sale of Opella and Consumer Healthcare separation-combined with redeployment of capital into higher growth pharmaceuticals and vaccines, is driving greater operating efficiency, improved product mix, and tighter SG&A/G&A control, all likely to further support net margin and BOI (business operating income) expansion. (Net Margins, BOI)

- Sanofi's leadership in vaccines, development of combination and next-generation products (e.g., Beyfortus, flu/RSV combinations), and active pursuit of regulatory incentives (orphan/fast-track designations) position the company to capitalize on secular trends of rising non-communicable disease prevalence and industry shifts toward biologics, supporting baseline revenue resilience despite periodic pricing pressures in established markets. (Revenue)

Sanofi Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

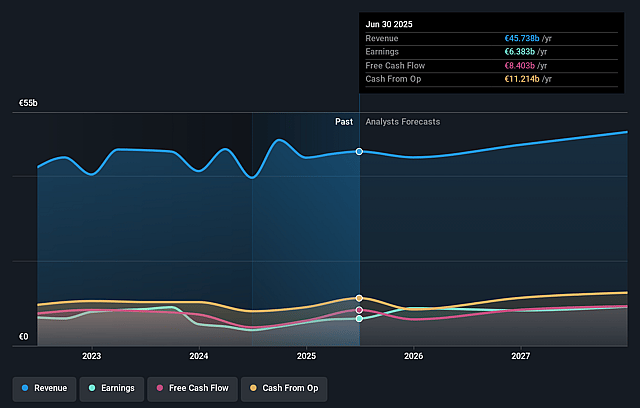

- Analysts are assuming Sanofi's revenue will grow by 3.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.6% today to 21.0% in 3 years time.

- Analysts expect earnings to reach €11.0 billion (and earnings per share of €8.82) by about April 2029, up from €4.9 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €12.5 billion in earnings, and the most bearish expecting €8.9 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 11.9x on those 2029 earnings, down from 20.2x today. This future PE is lower than the current PE for the US Pharmaceuticals industry at 20.2x.

- Analysts expect the number of shares outstanding to decline by 2.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.29%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heightened pressure from competitive pricing, particularly in flu vaccines (expected mid-teens decline in 2025 sales from price competition in the U.S. and Germany), poses a structural risk to Sanofi's long-term vaccine franchise and could compress net margins as pricing headwinds persist beyond this year.

- Pipeline execution remains a key uncertainty: management and investors directly acknowledged that Sanofi's R&D transformation will take several years to play out, and that some high-profile late-stage assets have produced "mixed" results or outright Phase III failures (e.g., itepekimab in COPD), increasing the risk of slower revenue and earnings growth if pipeline assets don't materialize as expected.

- Sanofi's heavy investment in new launches and recent acquisitions (e.g., Blueprint, Vigil Neuroscience, Vicebio), while offering promising long-term growth avenues, has resulted in higher SG&A and R&D expenses; failure to generate expected returns from these investments or delayed integration could limit operating leverage and compress net margins in the coming years.

- The expiration of patent protection for key blockbuster drugs like Dupixent (U.S. 2031, EU 2033) and increasing biosimilar/generic competition industry-wide mean Sanofi faces the risk of accelerating revenue erosion post-exclusivity, particularly as payers, governments, and insurers globally push harder for drug price reductions and transparency.

- Intensified regulatory and geopolitical uncertainty-such as potential U.S. tariffs on EU pharmaceuticals, drug pricing reforms in both the U.S. and Europe, and lengthening approval timelines amid higher regulatory scrutiny-could drive higher operating costs, strain international sales, and directly impair net earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €96.1 for Sanofi based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €112.0, and the most bearish reporting a price target of just €57.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €52.1 billion, earnings will come to €11.0 billion, and it would be trading on a PE ratio of 11.9x, assuming you use a discount rate of 6.3%.

- Given the current share price of €82.58, the analyst price target of €96.1 is 14.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Sanofi?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.