Catalysts

About Kalmar Oyj

Kalmar Oyj provides equipment and services for ports, terminals, heavy logistics and industrial customers, including an expanding range of low emission and electric solutions.

What are the underlying business or industry changes driving this perspective?

- Reliance on a high share of eco and electric equipment, with fully electric machines at 11% of equipment orders over the last 12 months, could expose Kalmar to slower than expected customer adoption if payback periods lengthen or funding tightens, which would pressure equipment revenue growth.

- Tariff exposure on Chinese origin components and batteries, along with shifting documentation requirements, raises the risk that price increases of around 5% to 15% fail to fully offset cost pressure, which would erode equipment margins and comparable operating profit.

- Americas demand, already described as subdued in distribution and affected by tariffs and cautious customer decision making, may remain structurally weaker than other regions, limiting order intake growth and constraining the order book that currently stands at around €1b.

- The long term push toward electrification, including the new lithium ion battery platform, requires continuing investment and supply chain reconfiguration. This could outpace the earnings benefits from the Driving Excellence program and compress net margins if savings do not fully cover higher R&D and sourcing costs.

- Growing dependence on services, which currently carry an 18.5% margin and 34% of sales, could be challenged if fleet activity or container throughput slow from current healthier levels. This could lead to softer service volumes and flattening earnings despite the current order book support.

Assumptions

This narrative explores a more pessimistic perspective on Kalmar Oyj compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming Kalmar Oyj's revenue will grow by 3.8% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 8.6% today to 11.0% in 3 years time.

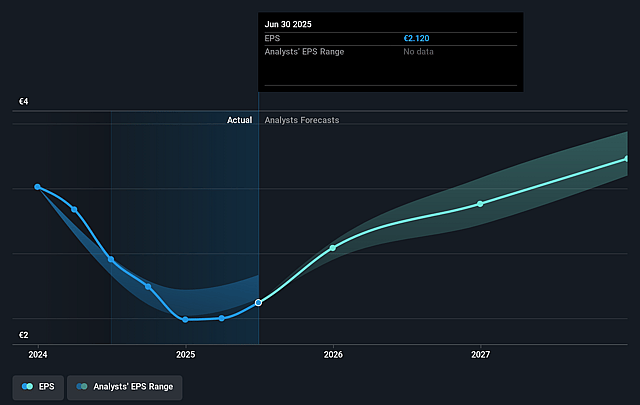

- The bearish analysts expect earnings to reach €207.4 million (and earnings per share of €3.24) by about January 2029, up from €145.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 14.2x on those 2029 earnings, down from 18.8x today. This future PE is lower than the current PE for the FI Machinery industry at 21.2x.

- The bearish analysts expect the number of shares outstanding to grow by 0.11% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.36%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Kalmar reports a record comparable operating profit margin of 13.8% in Q3, with a 12.7% margin over the last 12 months and guidance for a margin above 12% in 2025. This suggests the business currently converts revenue into profit at a healthy rate and, if sustained, could support earnings and justify a higher share price.

- Services now account for 34% of sales, service orders are up 12% in the quarter and 7% year to date, and the service margin stands at 18.5%. A larger, higher margin installed base can provide recurring revenue and earnings that may be more resilient in softer equipment cycles.

- The order book is around €1b and year to date orders are €1.3b compared to €1.2b last year. This indicates ongoing customer demand and future revenue visibility that could support both top line and operating profit, even if quarterly order intake fluctuates.

- Kalmar’s Eco portfolio accounts for 46% of sales and 43% of order intake, with fully electric machines at 11% of equipment orders and customer surveys suggesting 2/3 of customers plan to invest in low emission equipment. Long term electrification and sustainability trends could underpin revenue and margin development rather than a prolonged decline.

- The company reports positive fleet activity trends on 14,500 connected units and references external data showing upgraded forecasts for global GDP, container throughput and manufacturing for 2025 and 2026. Together with Kalmar’s global footprint, this could support volumes, pricing and, in turn, earnings if these trends persist.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Kalmar Oyj is €37.0, which represents up to two standard deviations below the consensus price target of €42.8. This valuation is based on what can be assumed as the expectations of Kalmar Oyj's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €52.0, and the most bearish reporting a price target of just €37.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be €1.9 billion, earnings will come to €207.4 million, and it would be trading on a PE ratio of 14.2x, assuming you use a discount rate of 7.4%.

- Given the current share price of €42.52, the analyst price target of €37.0 is 14.9% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Kalmar Oyj?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.