Last Update01 May 25Fair value Increased 0.043%

Key Takeaways

- Emphasis on own brand products and cost optimization strategies aims to enhance net margins and profit growth.

- Expansion in digital presence and strategic market focus could significantly boost revenue and earnings stability.

- Intense competition, financial impairments, and market risks challenge DFI Retail Group's revenue growth and financial stability, indicating potential underlying business weaknesses and reliance on innovations.

Catalysts

About DFI Retail Group Holdings- Operates as a retailer in Asia.

- The company's focus on own brand products at a higher margin could improve net margins as consumers are attracted to lower-price alternatives compared to national brands.

- Cost optimization strategies, such as reducing overhead and using a franchise model, are expected to enhance net margins and profit growth in the coming years.

- The expansion of digital and omnichannel presence, including data monetization through platforms like Yuu, has the potential to significantly boost revenue and earnings as e-commerce becomes profitable.

- Strategic divestments, such as the sale of Yonghui, and a disciplined CapEx approach focused on high-growth markets are expected to enhance shareholder returns and might positively impact earnings.

- Market share growth, particularly in convenience stores in South China and the focus on ready-to-eat segments, could drive increased revenue and earnings stability.

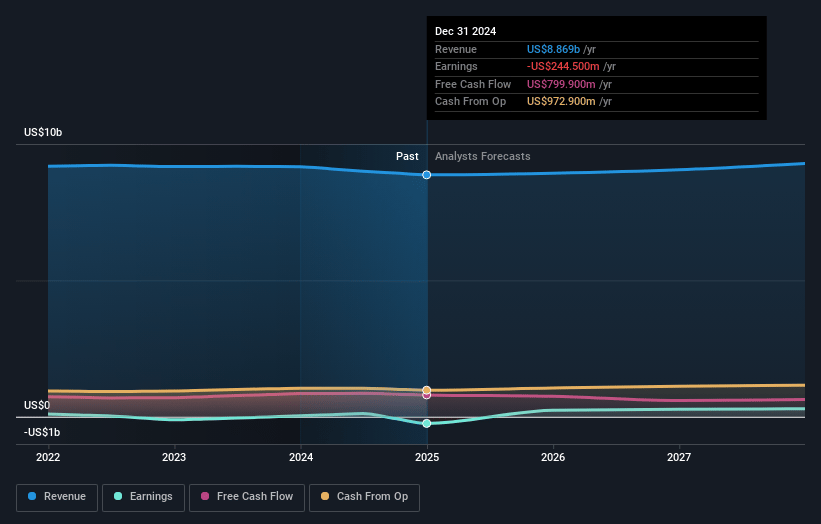

DFI Retail Group Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming DFI Retail Group Holdings's revenue will grow by 1.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -2.8% today to 3.2% in 3 years time.

- Analysts expect earnings to reach $290.2 million (and earnings per share of $0.22) by about May 2028, up from $-244.5 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $259 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.5x on those 2028 earnings, up from -14.0x today. This future PE is lower than the current PE for the GB Consumer Retailing industry at 26.8x.

- Analysts expect the number of shares outstanding to grow by 0.63% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.25%, as per the Simply Wall St company report.

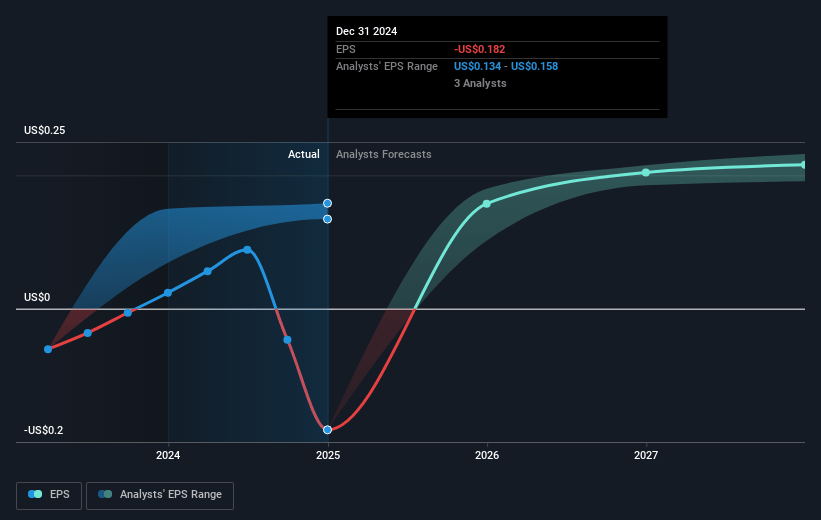

DFI Retail Group Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intense competition from Chinese digital players could impact market share and revenue, as it pressures DFI Retail Group to innovate and compete on pricing and convenience in a highly contested market.

- The impairment of $231 million on Robinsons Retail and other non-cash one-off losses such as goodwill impairments and a fair value loss related to Yonghui indicate potential underlying financial weaknesses, impacting net margins and reported earnings.

- The reported decline in revenue growth year-on-year and the focus on cost control rather than aggressive expansion could signify potential market stagnation or saturation, impacting long-term revenue prospects.

- The ongoing divestments and potential reliance on non-core revenue sources like media and data monetization might indicate a need to offset underlying business weaknesses or growth challenges within primary retail operations, impacting core operational earnings.

- Risks related to North Asia and Southeast Asia market dynamics, particularly given geopolitical tensions and economic uncertainties, could affect cross-border consumer behavior and demand, impacting revenue and overall financial stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $2.901 for DFI Retail Group Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $3.3, and the most bearish reporting a price target of just $2.32.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $9.1 billion, earnings will come to $290.2 million, and it would be trading on a PE ratio of 17.5x, assuming you use a discount rate of 8.2%.

- Given the current share price of $2.53, the analyst price target of $2.9 is 12.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.