Key Takeaways

- Focus on ASEAN diversification, digitalization, and green investment aims to boost growth, potentially increasing future revenue and intra-ASEAN economic activity.

- Integration and cost-cutting strategies, including Citi acquisition and capital return programs, aim to improve margins, stabilize earnings, and enhance shareholder value.

- Geopolitical tensions, interest rate cuts, and competitive pressures challenge UOB's revenue growth, margins, and asset quality, while cross-border strategies carry execution risks amid economic volatility.

Catalysts

About United Overseas Bank- Provides banking products and services worldwide.

- UOB's focus on supply chain diversifications, digitalization, and green economy investments in ASEAN are expected to boost intra-ASEAN connectivity and growth, potentially increasing future revenue from the region's growing economic activities.

- Integration benefits from the Citi acquisition and scaling in ASEAN markets are anticipated to drive higher growth in retail banking, supporting an increase in net margins due to economies of scale and cross-selling opportunities.

- The planned roll-off of Citi-related integration costs in 2025, along with efforts to enhance productivity, are expected to reduce the cost-to-income ratio, improving net margins and overall earnings.

- UOB's strategy to reshape its income drivers toward more recurring revenue streams like wealth management and transaction banking aims to reduce sensitivity to rate cycles, stabilizing earnings growth and potentially expanding net margins.

- Execution of a SGD 3 billion capital return program, including a special dividend and a share buyback initiative, is expected to enhance shareholder value and EPS, indicating confidence in strong future earnings performance.

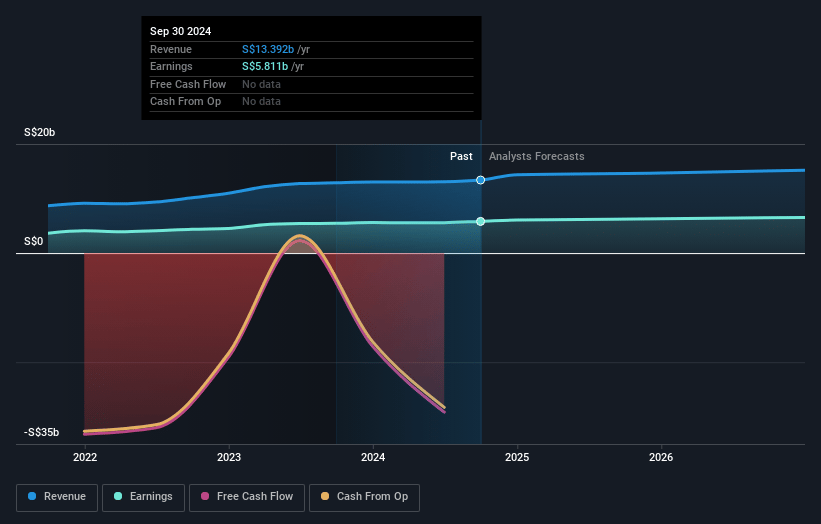

United Overseas Bank Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming United Overseas Bank's revenue will grow by 7.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 45.2% today to 44.0% in 3 years time.

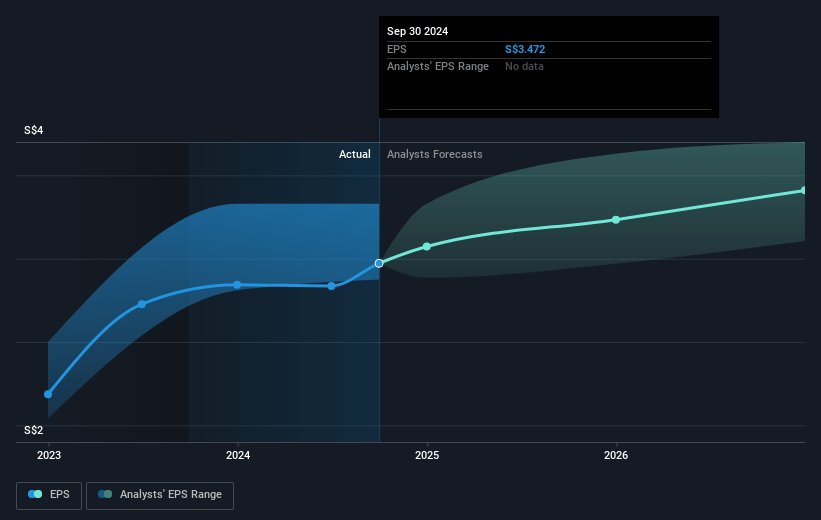

- Analysts expect earnings to reach SGD 7.3 billion (and earnings per share of SGD 4.35) by about March 2028, up from SGD 6.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.7x on those 2028 earnings, up from 10.4x today. This future PE is greater than the current PE for the SG Banks industry at 10.3x.

- Analysts expect the number of shares outstanding to decline by 0.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.98%, as per the Simply Wall St company report.

United Overseas Bank Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ongoing geopolitical tensions and tariffs create an uncertain economic outlook, potentially impacting UOB's revenue growth and net margins if trade relations remain strained.

- The declining net interest margin moderated to 2% due to interest rate cuts, which could affect overall earnings if rates remain low or decrease further.

- Specific allowances rose to 52 basis points due to problematic accounts in U.S. and Greater China, signifying possible challenges in asset quality that may affect net margins.

- UOB is experiencing competitive pressure and margin compression in the banking industry, particularly in Singapore, which could impact revenue and cost-to-income ratios if they are unable to sustain their competitive edge.

- The strategy of cross-border and transaction banking income growth, while beneficial for diversification, may require continued investment and carries execution risks that could impact earnings if global economic conditions are volatile.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SGD42.022 for United Overseas Bank based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SGD47.7, and the most bearish reporting a price target of just SGD36.9.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SGD16.6 billion, earnings will come to SGD7.3 billion, and it would be trading on a PE ratio of 11.7x, assuming you use a discount rate of 7.0%.

- Given the current share price of SGD37.5, the analyst price target of SGD42.02 is 10.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.