Key Takeaways

- Regulatory approvals in the U.S. for liver and heart technologies and Canadian market expansions may significantly boost revenue and market share in North America.

- Strategic improvements in the Abdominal segment are set to increase gross margins and profitability, while strong adoption in Australia indicates promising growth.

- Production constraints and regulatory uncertainties could hinder market expansion and revenue growth, while currency fluctuations may affect profitability and earnings.

Catalysts

About Xvivo Perfusion- A medical technology company, develops and markets machines and perfusion solutions for assessing usable organs and maintains in optimal condition pending transplantation in Sweden.

- The approval of the DELIVER IDE and the ability to start related trials in the United States for liver and heart technologies could serve as a catalyst for future growth by opening new revenue streams as the company gains U.S. market share. This is expected to impact revenue positively.

- The strategic initiative to improve the Abdominal segment's gross margin to 70% by 2027 through achieving economies of scale in production is expected to enhance the net margins over time, positively impacting profitability.

- Growth opportunities in Canada, supported by recent regulatory approvals for liver and kidney products, align with strategic market expansion plans. This could result in increased revenues and market share in the North American region.

- The expected heart technology expansion in Australia, with an observed growth of 60% in Q1, reflects strong regional adoption, suggesting increased revenue streams. Continued penetration could strengthen earnings.

- The initiative for a robust U.S. service offering, modeled after successful international approaches, is anticipated to be critical for the U.S. heart launch and could contribute to future sales revenue as it enhances the customer onboarding process.

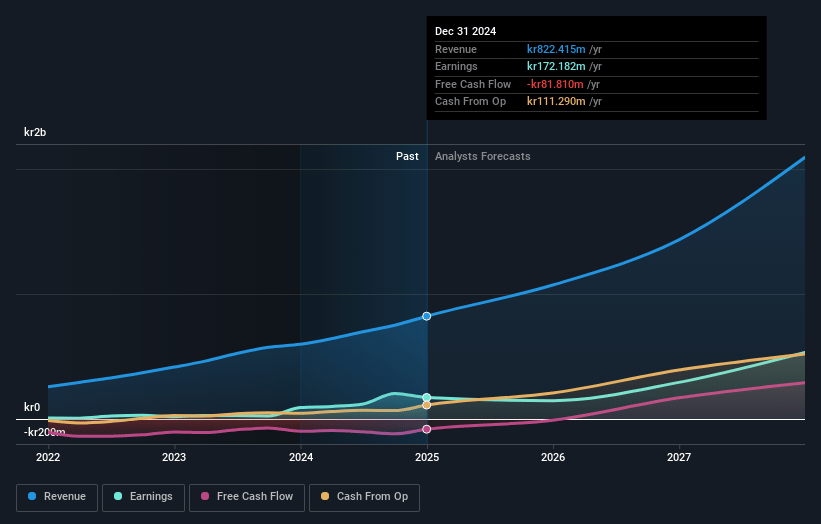

Xvivo Perfusion Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Xvivo Perfusion's revenue will grow by 31.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 16.0% today to 23.9% in 3 years time.

- Analysts expect earnings to reach SEK 460.6 million (and earnings per share of SEK 10.96) by about May 2028, up from SEK 137.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting SEK661 million in earnings, and the most bearish expecting SEK271 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 35.4x on those 2028 earnings, down from 73.4x today. This future PE is greater than the current PE for the GB Medical Equipment industry at 30.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.45%, as per the Simply Wall St company report.

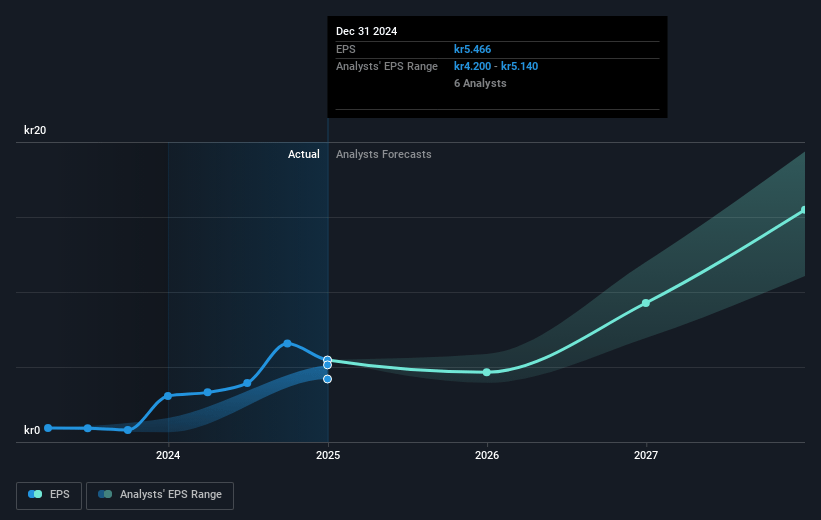

Xvivo Perfusion Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Challenges in the U.S. Service business and ongoing strategic review to improve organ recovery services could hamper support for growth, potentially affecting revenue from this segment.

- Availability of XPS machines is constrained due to production capacity limitations, which might impede the ability to meet growing demand and affect future revenues.

- The delayed availability of the kidney product enhancements in the U.S. could slow market penetration, impacting the revenue from this product line.

- Currency fluctuations, particularly a weakened U.S. dollar, could significantly impact sales and EBITDA margins, reducing expected earnings.

- Uncertainty in the regulatory timelines for the heart technology in Europe and dependency on CE-marking for expansion in Canada add risk to market access, potentially affecting future revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK448.5 for Xvivo Perfusion based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK520.0, and the most bearish reporting a price target of just SEK335.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK1.9 billion, earnings will come to SEK460.6 million, and it would be trading on a PE ratio of 35.4x, assuming you use a discount rate of 5.4%.

- Given the current share price of SEK319.2, the analyst price target of SEK448.5 is 28.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.