Key Takeaways

- Mandated EMG technology in Europe and the U.S. and new product launches set a strong growth trajectory, boosting sales and revenue.

- Expansion in the U.S. market and growth in Asia, coupled with strategic partnerships, enhance market penetration and diversify revenue streams.

- Key challenges include disruptions from the new system, dependency on U.S. market stability, competition in Europe, and looming funding needs impacting profitability.

Catalysts

About Senzime- A medical device company, develops, manufactures, and markets algorithm-powered patient monitoring systems to increase patient safety during and after surgery in Europe and the United States.

- The introduction of clinical guidelines in both Europe and the U.S. mandating EMG technology for patients receiving paralytic drugs can drive sales of Senzime's TetraGraph system significantly, boosting future revenue.

- The launch of the next-generation TetraGraph in October 2024, with enhanced features and adaptive intelligence, sets a strong foundation for future growth as it drives interest and adoption among hospitals, positively impacting revenue and earnings.

- Senzime's focus on expanding its U.S. commercial sales force and increasing headcount by 30% could lead to enhanced market penetration and accelerated revenue growth in one of its key markets.

- The shift in hospitals towards formalizing EMG monitoring as part of standard care, along with strong industrial partnerships for data integration with platforms like Philips and GE Healthcare, could increase recurring sales of disposable sensors, enhancing revenue and net margins.

- Significant growth in Asian markets, particularly Japan and South Korea, due to local collaborations and reimbursement opportunities, positions Senzime for diversified international revenue growth, strengthening overall financial performance.

Senzime Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Senzime's revenue will grow by 80.9% annually over the next 3 years.

- Analysts are not forecasting that Senzime will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Senzime's profit margin will increase from -179.6% to the average SE Medical Equipment industry of 11.0% in 3 years.

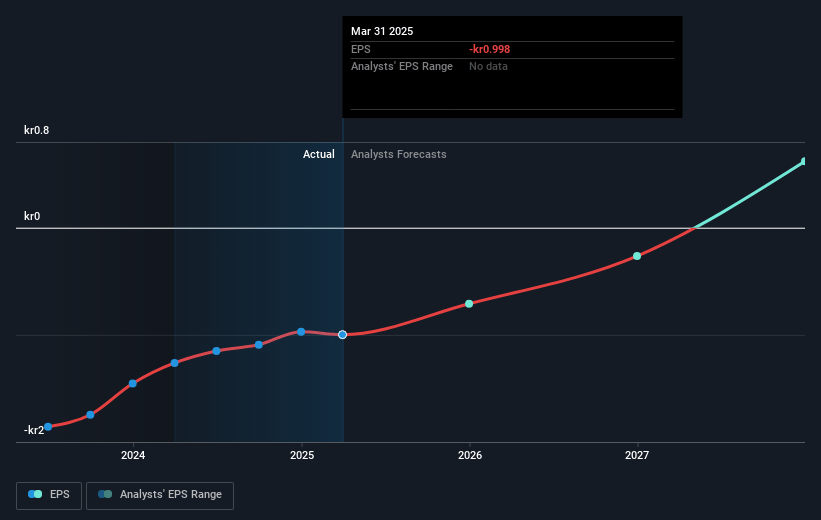

- If Senzime's profit margin were to converge on the industry average, you could expect earnings to reach SEK 45.7 million (and earnings per share of SEK 0.28) by about May 2028, up from SEK -125.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 50.3x on those 2028 earnings, up from -5.1x today. This future PE is greater than the current PE for the SE Medical Equipment industry at 30.9x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.51%, as per the Simply Wall St company report.

Senzime Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The introduction of the next-generation TetraGraph system led to short-term disruptions in the purchasing process, affecting Q4 growth and potentially impacting short-term revenue.

- Operating expenses remain a concern despite reductions, and the company has signaled the likelihood of needing additional funding to reach profitability, which could affect net margins.

- Challenges in the European market due to competition from established AMG technology and budget constraints for new capital goods could hinder revenue growth in this region.

- Dependence on the U.S. market, which constitutes a significant portion of their business, poses a risk if there are changes in healthcare regulations or economic conditions, impacting overall earnings.

- The company's need to secure long-term funding through means that may not be equity-based indicates a potential strain on financial resources, which could affect net margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK12.0 for Senzime based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK413.4 million, earnings will come to SEK45.7 million, and it would be trading on a PE ratio of 50.3x, assuming you use a discount rate of 5.5%.

- Given the current share price of SEK4.83, the analyst price target of SEK12.0 is 59.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.